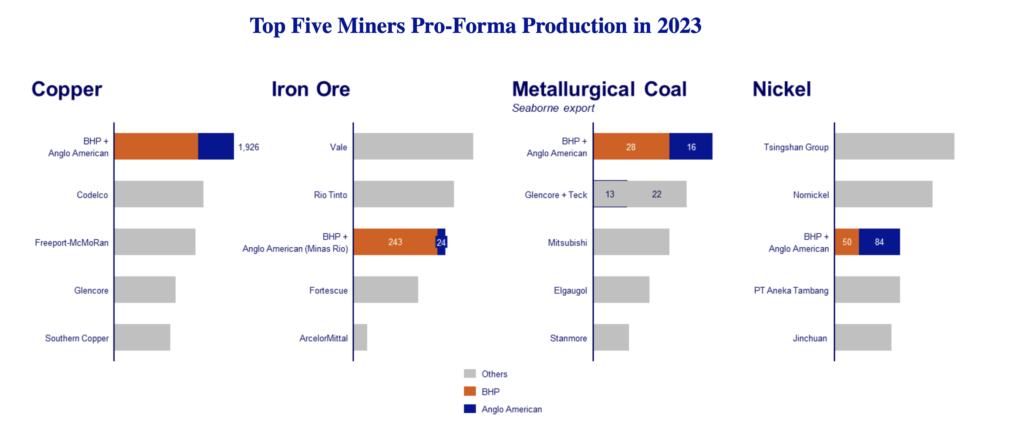

An electrified world has change into more and more depending on battery metals, notably on copper, and BHP is, not surprisingly, desperate to safe a number one place on this market. A tie-up would give the mining large about 10% of worldwide copper manufacturing.

It could additionally enhance its presence on the earth’s high copper producing international locations, Chile and Peru, as with the acquisition of Anglo American, BHP would achieve entry to 4 of the world’s largest copper mines — Collahuasi (with possession of 44%), Los Bronces (50.1%), El Soldado (50.1%) and Quellaveco (60%). This could enhance the corporate’s publicity to copper by about 40%.

BHP’s proposal is valued at £25.08 per Anglo share, a 14% premium to the goal firm’s closing value on Wednesday. In keeping with analysts, the provide will not be as candy because it appears they usually consider Anglo American is well-positioned to push for a greater deal.

Given its conglomerate nature, discovering a knockout value isn’t a easy process.

“Anglo American is a longtime conglomerate with a fancy construction, that includes quite a few partial possession stakes and numerous defensive mechanisms, most of that are concentrated in its South African property,” Jefferies’ Christopher LaFemina wrote in a be aware to shoppers.

The analyst believes that “a value of not less than £28 per share can be vital for severe discussions to happen, and a takeout value of nicely above £30 per share can be the end result if different bidders had been to become involved”.

“If we embrace our estimate of synergies on an after-tax current worth foundation, we estimate Anglo honest worth to be 2824p per share, which equates to a $42.6 billion fairness worth. That’s 28% above the newest Anglo share value, and we consider it’s a cheap place to begin,” LaFemina wrote.

Anglo American turned a takeover goal lately after output fell and prices mounted.

“It turned a possible goal for BHP as Anglo continued to publish a weak top-line, whilst its whole debt saved growing since 2021 because of the poor efficiency of platinum group metals (PGMs) and diamonds on account of value fluctuations, geopolitical and financial conditions, and different operational constraints,” Sathiya Narayanan Jalapathy, Enterprise Fundamentals Analyst at GlobalData, wrote in an emailed assertion.

“Amidst this, the corporate has reported progress of 31.5% in copper gross sales from $5,599 million in 2022 to $7,360 million in 2023 (…) Operationally, the mixed entity may have a high line of over $84 billion, EBITDA of over $34 billion, and a workforce of near 100,000, reinforcing its place as one the biggest world gamers within the mining sector,” he famous.

“The deal would signify the largest shakeup of the worldwide mining business in additional than a decade,” says James Whiteside, metals and mining analysis director at Wooden Mackenzie. “However Anglo American shareholders might contemplate honest worth nearer to the share value in 2023 earlier than operational points emerged and different suitors could also be compelled to behave at this value.”

Berenberg analyst Richard Hatch will not be satisfied that Anglo presents important turnaround alternatives.

“BHP is doubtlessly shopping for a bunch of property that want some care and a focus,” Hatch wrote, referring to Anglo’s operations in South Africa. “This, in our view, provides restricted upside at this level with present valuation multiples that will additionally indicate a barely dilutive deal for BHP.”

In keeping with Fitch Group, BHP is “possible drawn by the corporate’s low valuation (inventory down 12% over the LTM), with the corporate going by a multi-year operational restructuring. From a strategic standpoint, larger is all the time higher within the metals and mining sector.”

“Extremely opportunistic“

Earlier on Thursday considered one of Anglo’s 20 largest shareholders, Authorized & Common Funding Administration, mentioned BHP’s strategy was “extremely opportunistic” and “unattractive”.

“As with many different UK-listed corporations, we consider the valuation of Anglo American to be depressed and regard the proposed alternate ratio as an unattractive proposition for long-term traders,” Nick Stansbury, head of local weather options at Authorized & Common Funding Administration (LGIM), mentioned in an emailed assertion.

“The business is extraordinarily concentrated immediately, and additional consolidating it is not going to contribute to accelerating funding in the best way we consider is required,” Stansbury mentioned.

Anglo American didn’t reply to a request for feedback however in a press release it mentioned it was reviewing the proposal, which might require it to separate its majority holdings in South Africa of Anglo American Platinum (JSE: AMS) and Kumba Iron Ore (JSE: KIO) beforehand.

With a deal with the steel key to the power transition, BHP itself purchased copper producer OZ Minerals final 12 months for about $6.4 billion whereas Rio Tinto (NYSE: RIO; LSE: RIO; ASX: RIO), the world’s second largest miner, has been investing in copper mines in Utah and Arizona.

Deal underneath the microscope

BMO Capital analyst Alexander Pearce highlighted that the deal to mix each miners can be topic to important anti-trust/competitors scrutiny, notably in the case of the copper property.

The Anglo-owned Quellaveco and BHP-owned Antamina mines are key to Peru’s economic system. If the merger is profitable, each operations can be underneath the identical possession, elevating questions of a possible market focus subject or perhaps a main political concern.

The deal may face authorities and native opposition because of the scale and affect of the mixed firm. Relying on the character of the perceived downside, the antitrust resolution might contain selectively promoting off elements of the enterprise which are deemed non-essential, with a view to deal with focus points, whereas preserving the core copper property that each corporations view as strategically vital. These are the problems in South America.

The problems the merged firm may face in South Africa are equally or harder. The nation’s minerals sources minister Gwede Mantashe will not be an enormous fan of BHP and has already voiced his opposition to BHP’s bid for Anglo.

Mantashe advised the Monetary Instances that he was not in favour of BHP’s bid given the nation’s earlier “not constructive” expertise with the corporate, referencing the 2001 merger between BHP and Billiton that created the world’s largest mining firm.

Whereas he clarified this was his private opinion and never the federal government official place on the matter, Mantashe mentioned that BHP Billiton “by no means did a lot for South Africa” and led to “capital leaving the nation.”

BHP in 2015 created and spinned off South32 (ASX, LON, JSE:S32), an organization that inherited the South African property and operations.By way of this demerger, BHP successfully diminished its publicity to the nation in a transfer interpreted as many as its try and restrict its involvement within the nation.

Anglo American, in distinction, embodies the mining custom of South Africa. Began within the nation in 1917, it holds the fourth-largest place within the FTSE/JSE Africa All Share Index, accounting for 4.3% of the index.

Anglo has controlling pursuits in two different mining corporations listed on the South African inventory alternate — Anglo American Platinum Ltd., also called Amplats, and Kumba Iron Ore.

The corporate additionally owns one other South African emblematic firm: Diamond large De Beers, which Anglo acquired greater than a decade in the past.