The Canadian miner had tried to achieve an settlement with one in all three unions representing roughly 30% of Caserones staff, or 5% of the overall workforce on the Caserones, previous to the strike…

The corporate just lately upped its stake in Caserones to 70% after exercising an choice with Japan’s JX Nippon Mining & Metals. The mine represents one in all Lundin’s trio of key property in or round northern Chile, the opposite two being the 80%-owned Candelaria mine within the Atacama area and the Josemaría undertaking in Argentina. (through Mining.com)

No phrase but on how the strike might influence manufacturing.

Chile is the biggest producer of mined copper on the planet, adopted by the Democratic Republic of Congo and Peru.

Labor strife can also be evident at BHP’s large Escondida mine, with a strike beginning on Tuesday. Reuters reported “a strong employees union… is trying to snarl manufacturing on the web site because it pushes for an even bigger share of earnings.”

Readers might recall a 44-day strike at Escondida in 2017 which brought about copper costs to spike when the mega-miner declared “pressure majeure”.

The identical factor occurred in 2016 after a 26-day strike, and in 2011 the union halted operations for 2 weeks.

In Africa, the export of copper has been interrupted for a special motive. On Aug. 11, Zambia quickly sealed its border with Congo after the DRC authorities banned sure beverage imports, together with beer, from Zambia, native media mentioned.

Landlocked Congo solely has one approach to entry ports, and that’s via Zambia. The latter resumed commerce with the DRC on Tuesday.

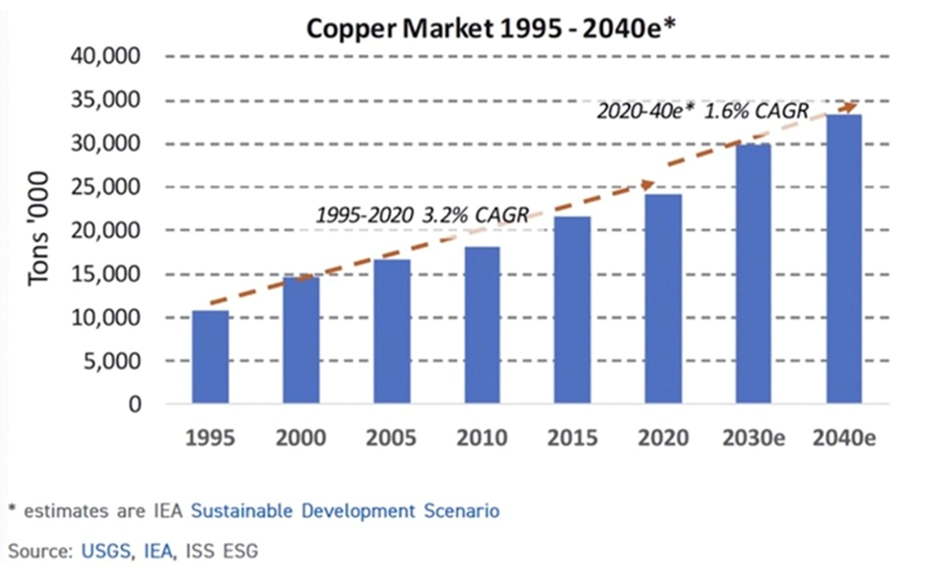

Copper market

Benchmark Mineral Intelligence (BMI) forecasts international copper consumption to develop 3.5% to twenty-eight million tonnes in 2024, and for demand to extend from 27 million tonnes in 2023 to 38 million tonnes in 2032, averaging 3.9% yearly development.

But the US Geological Survey reviews provide from copper mines in 2023 amounted to solely 22 million tonnes. If the copper provide doesn’t develop this 12 months, we’re presumably a 6Mt deficit.

Mining corporations are seeing their reserves dwindle as they run out of ore. Commodities funding agency Goehring & Rozencwajg says the business is “approaching the decrease limits of cut-off grades and brownfield expansions are not a viable resolution. If that is appropriate, then we’re quickly approaching the purpose the place reserves can’t be grown in any respect.”

Successfully, decrease grades imply tens of millions of tonnes extra rock must be moved and processed to get the identical quantity of copper.

In July, the vice chairman of US funding financial institution Stifel Monetary Cole McGill introduced knowledge that corroborates Goehring & Rozencwajg, stating “In the event you have a look at grades on the prime 20 copper mines since 2000, they’ve trended down about 15-20%, and when you take out a number of the higher-grade African tasks, that’s even decrease.”

Sprott agrees that, Chile and Peru, the highest copper-producing nations, are grappling with labor strikes and protests, compounded by declining ore grades. Russia, ranked seventh in copper manufacturing, faces an anticipated decline because of the ongoing battle in Ukraine. Regardless of efforts by miners to ramp up manufacturing, many analysts anticipate a widening provide imbalance.

Main copper miners aren’t doing a lot to alleviate the issue. Excessive-quality tasks are more and more uncommon and main new discoveries are missing. The worldwide time from discovery to manufacturing averages 16.5 years.

To satisfy the rise in copper demand, copper majors are targeted on extending the life spans and productiveness of present mines slightly than finishing up dearer, and dangerous, exploration and growth of latest (greenfield) tasks.

E&MJ Engineering said in its outlook for copper manufacturing to 2050, “The development towards declining orebody grades and continued growth of the pursuit of present operations to use decrease grade deposits is more likely to proceed, within the absence of high-grade undertaking discovery.

“A decline in ore grade leads to greater working prices due primarily to the quantity and depth of fabric required to be mined and processed to supply the identical quantity of copper product. It’s no shock that each GHG emission depth and power depth improve as ore grade decreases. There’s a level of inflection, the place under an ore grade of round 0.5% copper, the depth of each metrics rises sharply.”

Provided that many mines are quick approaching, if not already tackling, related grades, it is a urgent drawback. In its fiscal 12 months 2020 commodity outlook, BHP, the world’s third largest copper producer, estimated that grade decline might take away about 2 million metric tons per 12 months (mt/y) of refined copper provide by 2030, with useful resource depletion doubtlessly eradicating an extra 1.5 million to 2.25 million mt/y by this date.”

Grade decline, deteriorating ore high quality and provide strain from rising useful resource nationalism highlights the significance of funding exploration.

Sadly, in accordance with Sprott, capital for the exploration and growth of copper mines peaked at $26.13 billion in 2013. Since then, it has virtually halved and stays low, with solely $14.42 billion spent in 2022.

McGill advised Bloomberg that between 2009 and 2016, copper provide grew at a CAGR of three.5-4%. Since 2016, when copper priced bottomed at round $2-2.20/lb, the CAGR is round 1%.

With out new capital investments, Commodities Analysis Unit (CRU) predicts international copper mine manufacturing will drop to under 12Mt by 2034, resulting in a provide shortfall of greater than 15Mt. Over 200 copper mines are anticipated to expire of ore earlier than 2035, with not sufficient new mines within the pipeline to take their place.

Final 12 months, the federal government of Panama ordered First Quantum Minerals (TSX:FM) to close down its Cobre Panama operation, eradicating almost 350,000 tonnes from international provide.

A strike at one other massive copper mine, Las Bambas in Peru, quickly halted shipments.

Copper specialist Anglo American (LSE:AAL) says it’s scaling again output by about 200,000 tons, owing to move grade declines and logistical points at its Los Bronces mine. Los Bronces manufacturing is predicted to fall by almost a 3rd from historic ranges subsequent 12 months because the miner pauses a processing plant for upkeep, Reuters mentioned.

Copper mined from Anglo American’s Chile and Peru operations was 6% decrease within the second quarter in contrast Q2 2023, and 1% decrease than Q1 2024. The lower was “pushed by decrease throughput at Los Bronces and El Soldado, and deliberate decrease grades at Quellaveco, partially offset by greater throughput at Collahuasi pushed by the fifth ball mill,” the corporate said in a quarterly manufacturing report.

Chile’s copper output has been dented by a long-running drought within the nation’s arid north. State miner Codelco’s 2023 manufacturing was the bottom in 25 years.

All 4 of Codelco’s megaprojects have been delayed by years, confronted price overruns totaling billions, and suffered accidents and operational issues whereas failing to ship the promised enhance in manufacturing, in accordance with the corporate’s personal projections.

A July 11 Reuters story mentioned Codelco is behind goal for manufacturing in 2024, with H1 manufacturing decrease than final 12 months’s first half. Output has been hit by a deadly accident at it’s Radomiro Tomic mine, and delays to the startup of its Rajo Inca undertaking. Chairman Maximo Pacheco mentioned longer-term points have affected Chuquicamata and El Teniente, with out elaborating.

Glencore’s (LSE:GLEN) first-half manufacturing of 462,600 tonnes was 2% under 2023’s 488,000 tonnes, which the agency attributed to the sale of its Cobar mine in Australia.

Freeport McMoran (NYSE:FCX) noticed decrease second-quarter output of 1.037 billion kilos in comparison with the year-ago quarter of 1.067Blbs, however greater first-half manufacturing of two.122Blbs in comparison with H1 2023’s 2.031Blbs. Quarterly copper manufacturing from Freeport’s North American mines was down for each time intervals.

In Zambia, Africa’s second largest copper producer drought situations have lowered dam ranges, creating an influence disaster that threatens the nation’s deliberate copper growth.

Certainly First Quantum mentions “further energy provide restrictions by Zambian Electrical energy Provide Company Restricted.” Whereas the corporate highlights 2% greater second-quarter manufacturing in comparison with Q1, with 10,034 extra tonnes mined at Kansanshi, its quarterly manufacturing was down y/y, from 187,175 tonnes in Q2 2023 to 102,709t in Q2 2024.

Ivanhoe Mines (TSX:IVN) reported a 6.5% Q1 drop in manufacturing on the world’s latest main copper mine, Kamoa-Kakula within the DRC.

The forecasted copper provide hole — greater than 15Mt by 2034 — was entrance and heart on the Rule Symposium in Florida earlier this 12 months. Mining magnate and Ivanhoe Mines’ founder Robert Friedland mentioned present copper costs “fall woefully brief” of supporting the event of latest tasks.

“We see a disaster coming in bodily markets and a requirement for a lot greater costs to allow a lot of the copper tasks which might be in growth to have a prayer coming in,” Friedland mentioned through The Northern Miner. The motivation worth to construct new mines is $11,000/t.

Increased costs are wanted to counteract hovering price inflation in constructing new mines, even in cheaper jurisdictions like Chile and Peru.

Friedland produced a shocking statistic, that humanity should mine extra copper within the subsequent 20 years than we now have in human historical past to satisfy surging international demand on the again of the power transition.

He estimated the worldwide economic system wants to seek out 5 or 6 new Kamoa-Kakula-sized tasks yearly to keep up a 3% gross home product development fee over the following 20 years.

Over the previous 10 years, greenfield additions to copper reserves have slowed dramatically. S&P International estimates that new discoveries averaged almost 50Mt yearly between 1990 and 2010. Since then, new discoveries have fallen by 80% to solely 8Mt per 12 months.

There are actually solely 3 ways for the business to get this extra metallic. First, they will improve manufacturing from present mines; this typically entails “going underground”, digging beneath the present open pit to entry extra ore. An growth to the present concentrator or constructing a brand new one, is usually wanted.

Second, they will increase their mines laterally, going after assets that weren’t a part of the preliminary mine plan as a result of they have been much less accessible, or un-economic.

Third, they will discover for brand spanking new mineral deposits, both internally, or working with junior mining corporations, which have the exploration experience to convey a deposit ahead to the purpose when it may be bought to a significant.

Clearly choice three, often known as greenfield exploration, is tougher, pricey, and carries greater threat than choices one and two, referred to as brownfield exploration.

Crux Investor famous that majors like BHP are buying copper property via M&A slightly than constructing new mines. Examples embody BHP’s buy of Oz Minerals and Newmont’s acquisition of Newcrest.

Regardless of the market’s recognition of copper’s function sooner or later economic system and growing provide tightness, Crux Investor says evaluation exhibits copper costs nonetheless stay under their long-term inflation-adjusted common, suggesting room for additional appreciation.

Whereas BMO Capital Markets and Citigroup analysts consider present copper costs might rise previous $4.54/lb as a result of a Chinese language smelter provide scarcity, and grid investments in China, they are saying a sustained worth acquire is required by copper miners to make funding choices.

Copper mining is a particularly capital-intensive enterprise for 2 causes.

First, mining has a big up-front format of building capital referred to as capex — the prices related to the event and building of open-pit and underground mines. There may be typically different company-built infrastructure like roads, railways, bridges, power-generating stations and seaports to facilitate extraction and delivery of ore and focus. Second, there’s a repeatedly rising opex, or operational expenditures. These are the day-to-day prices of operation: rubber tires, wages, gas, camp prices for workers, and so forth.

The common capital depth for a brand new copper mine in 2000 was between US$4,000-5,000 to construct the capability, the infrastructure, to supply a tonne of copper. In 2012 capital depth was $10,000/t, on common, for brand spanking new tasks. At this time, constructing a brand new copper mine can price as much as $44,000 per tonne of manufacturing.

Capex prices are escalating as a result of:

- Declining copper ore grades means a a lot bigger relative scale of required mining and milling operations.

- A rising proportion of mining tasks are in distant areas of creating economies the place there’s little to no present infrastructure.

- Many inputs vital for mine-building are getting dearer, as cross-the-board inflation, the very best in 40 years, infiltrates the business. This contains two of the biggest prices, wages and diesel gas, used to run mining tools.

The underside line? It’s changing into more and more pricey to convey new copper mines on-line and run them.

Traders are additionally demanding the next return on funding than beforehand, when there was a higher urge for food for threat.

Citigroup is bullish on copper, with the financial institution’s analysts predicting that costs might surpass $10,000 a tonne ($4.53/lb) this 12 months as a result of coverage help in China.

Mining.com reviews Beijing is predicted to introduce additional stimulus to improve its renewable power infrastructure on the Third Plenum assembly in mid-July:

These further measures, particularly focusing on home property and grid investments, are anticipated to help copper costs within the close to time period, Citi analysts mentioned in a word.

Why Kodiak Copper (TSX.V:KDK, OTCQB:KDKCF, Frankfurt:5DD1)

Kodiak Copper’s MPD undertaking is positioned alongside the southern-most portion of the Quesnel Trough, a particularly potential for discovery mineral belt extending over 1,000 kilometers from Washington State to the Yukon border. It’s the longest mineral belt in Canada and British Columbia’s most important copper-producing belt.

Copper-gold porphyries embody Copper Mountain, New Afton, Mount Milligan, Woodjam, Kwanika and Kemess. Teck’s Highland Valley is the largest open-pit mine in Canada.

The possibilities of efficiently discovering a deposit and constructing a mine are considerably greater when a talented workforce is in cost. Kodiak’s administration workforce, and the Discovery Group, have a profitable, an envious, monitor report of shareholder return.

Copper market fundamentals are at the moment sturdy with analysts predicting growing demand going through the headwinds of structural provide deficits.

KDK has a big, absolutely funded exploration/drilling program underway, and traders can anticipate information properly into 2025.

Kodiak Copper, via a novel mixture of superior fashionable expertise (AI) and quaint ‘boots on the bottom’ exploration and prospecting provides vital publicity to copper and gold.

Exploration has already proven loads of dimension potential as KDK has now drilled a number of kilometer-scale zones of mineralization over virtually your complete size of the property of 20km. Drilling up to now at Kodiak’s MPD deposit has proved in depth and high-grade mineralization at a number of porphyry facilities, with a number of targets but to be examined. The 2024 drill program is ready to check a number of targets, constructing important mass.

And we all know that the undertaking shares geological similarities to Copper Mountain and New Gold. All three are alkalic copper porphyries, that means the mineralization is copper-gold.

“We’re absolutely funded for a considerable drill program as we proceed to systematically show that our district-scale MPD undertaking has the potential to grow to be a world-class mine. For our 2024 program we now have prioritized high-confidence targets close to present zones to increase mineralization, and new targets that current contemporary discovery potential. We’ll proceed to construct important mass and focus significantly on including and increasing near-surface mineralization and higher-grade zones.” Claudia Tornquist, Kodiak President and CEO

Junior Useful resource Firm valuations are low and Kodiak Copper MPD Mission has all of the hallmarks of a significant copper/gold porphyry system with the potential to grow to be a world class mine.

Kodiak’s MPD Mission lies in a low price, low threat space. Infrastructure contains provides, roads, railway, extremely educated expert native workforce and low-cost hydro energy.

Robust capital construction and shareholders with Cdn$7m in treasury.

With a robust capital construction, money in hand, a completely funded exploration/ drilling program underway, and Teck Assets as their largest shareholder (holding 9.1%), it appears Kodiak Copper is well-positioned for development.

Why Max Useful resource Corp (TSXV:MAX; OTC:MXROF; Frankfurt:M1D2)

MAX is taking a contemporary method to exploring its Sierra Azul Copper-Silver Mission in Colombia, following a just lately signed earn-in settlement with Freeport-McMoRan Exploration Company (“Freeport”), an entirely owned-affiliate of Freeport-McMoRan Inc. (NYSE:FCX).

Below the phrases of the EIA , introduced on Might 13, Freeport has been granted a two-stage choice to amass as much as an 80% possession curiosity within the Sierra Azul Mission by funding cumulative expenditures of CAD$50 million and making money funds to Max of CAD$1.55 million.

This week, Max introduced the 2024 exploration program at Sierra Azul, funded by USD$4.2 million (CAD$5.8 million) of accredited expenditures by Freeport-McMoRan Exploration Company, as per the Might 13 earn-in settlement.

“We’re leveraging Freeport’s international exploration workforce and experience to unlock Sierra Azul’s potential, which we consider is host to one of many world’s largest underexplored sedimentary and volcanic copper-silver programs,” Max’s CEO Brett Matich mentioned within the July 29 information launch.

“The USD$4.2 million exploration funds to be applied within the second half of 2024 is the biggest annual exploration funds up to now. We sit up for working with Freeport, one of many world’s largest copper producers, to advance our Sierra Azul Copper-Silver Mission.”

This system has two most important aims:

Conduct systematic regional exploration over your complete Sierra Azul undertaking space of higher than 1,300 km;

Outline precedence targets for drilling.

By way of drill targets, this system will focus exploration on 28 targets that span 90 km over all three districts of the Sierra Azul Mission: AM, Conejo and URU. The 2 precedence districts are AM and Conejo. AM is extra superior and potential with 14 targets and potential deep-seated floor constructions. Conejo is earlier-stage however considered a minimum of as potential as AM.

Conclusion

At AOTH we consider copper presents a compelling alternative for traders. The Sprott report notes that copper costs and miners are more likely to profit from the rising supply-demand hole. It additionally says that copper’s strategic significance drove vital M&A in 2023, with BHP and Rio Tinto buying copper producers at vital premiums. Automakers involved about securing future provides are investing immediately in mining corporations.

However copper miners shopping for different copper miners does nothing to alleviate the provision scarcity. It solely transfers one copper reserve to a different. Majors have underinvested in copper exploration and growth, preferring M&A to the expense and threat of discovering new copper deposits.

Junior copper explorers present traders publicity to potential new discoveries that might assist slim the provision hole. These discoveries supply the prospect for outsized returns, although clearly with greater threat.

Juniors useful resource corporations are delicate to commodity costs, that means their share costs rise, or fall, immediately in step with the commodity with which they’re related. Traditionally junior useful resource corporations have supplied one of the best leverage to rising commodity costs.

Richard owns shares of Max Assets (TSXV:MAX)

Richard doesn’t personal shares of Kodiak Copper (TSX.V:KDK).

KDK and MAX are paid advertisers on his web site aheadoftheherd.com

This text is issued on behalf of MAX and KDK

Authorized Discover / Disclaimer

Forward of the Herd publication, aheadoftheherd.com, hereafter often known as AOTH.

Please learn your complete Disclaimer fastidiously earlier than you utilize this web site or learn the publication. If you don’t conform to all of the AOTH/Richard Mills Disclaimer, don’t entry/learn this web site/publication/article, or any of its pages. By studying/utilizing this AOTH/Richard Mills web site/publication/article, and whether or not you truly learn this Disclaimer, you’re deemed to have accepted it.