Copper is a vital part of electrification; with out it, the world can’t decarbonize. WoodMac estimates that demand for the metallic is ready to rise as a lot as 75% to 56 million tonnes by 2050.

Assembly this demand received’t be straightforward.

Present mines and tasks beneath building are anticipated to fulfill solely 80% of copper wants by 2030, the Worldwide Power Company has mentioned.

Nonetheless, provide progress is extra than simply about constructing new mines. Downstream processing (smelting and refining) and semi-manufacturing/fabricating are additionally main components of the copper provide that WoodMac analysts say are being ignored.

At the moment, China dominates each of those sectors.

China’s dominance

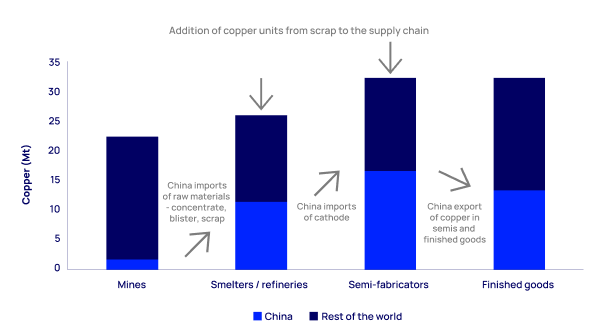

WoodMac estimates that near 80% of copper mining produces copper focus, which should then be processed at smelters and refineries to provide the copper cathode traded in terminal markets.

Since 2000, China has accounted for 75% of worldwide smelter capability progress and presently controls practically all of worldwide smelting and refining capability (97%), contributing over 3 million tonnes of manufacturing and practically $25 billion in funding, it says.

The nation has additionally added practically 11 million tonnes of copper and alloy capability since 2019, representing round 80% of worldwide additions. Roughly two-thirds of those services produce wire rods, giving China half of the world’s fabrication capability, with additional growth underway.

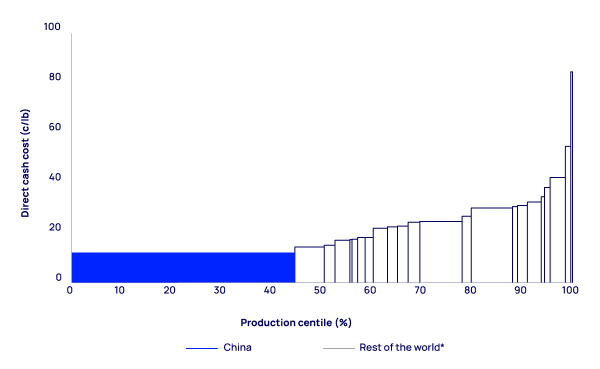

“China’s copper smelting trade has undergone vital evolution,” commented Zhifei Liu, managing guide, copper markets, at WoodMac. “Within the 2000s, a drive for stricter environmental and effectivity requirements led to the modernization of smelting capabilities.

“At this time, Chinese language smelters are low price and meet excessive environmental requirements, notably in sulphur dioxide seize, making them extremely aggressive.”

In the meantime, semi-fabricators exterior of China are dealing with challenges resulting from decrease utilization and better working prices regardless of efforts just like the Inflation Discount Act, and there aren’t any plans for brand new main smelting capacities in North America or Europe, WoodMac’s report says.

Life with out China

With out China, whose first use of copper accounts for 50% of worldwide demand, it’s anticipated that considerably extra processing capability could be required to fulfill vitality transition targets.

WoodMac estimates round 8.6 million tonnes of further copper demand ex-China over the following decade, pushed by progress in transport, energy and electrical networks. This equates to 70% of smelter functionality and 55% of fabricator capability in the remainder of the world.

Assuming international common capital depth, practically $85 billion in new smelting and refining functionality could be wanted to displace Chinese language provide, it provides.

But, because the WoodMac report factors out, capability has barely modified exterior China over the past 20 years, elevating the query of whether or not such a shift is achievable.

A situation with out China for the copper provide chain, says Nick Pickens, WoodMac’s analysis director of worldwide mining, would require “a considerable enhance in processing capability to fulfill vitality transition targets.”

Compromise wanted

Whereas copper provide dangers might be mitigated and a few rebalancing has begun in varied nations, the size of China’s dominance within the provide chain means “full substitute is unfeasible,” Pickens goes on to say.

He additionally notes that the introduction of latest processing and fabrication services might lead to increased prices and delays within the vitality transition. “Financing these investments presents further hurdles, with resistance to new smelter tasks on environmental and social grounds notably sturdy in Europe.”

Until there’s a seismic shift within the price and effectivity at which the remainder of the world deploys capital and operates, decoupling from China fully will imply a dearer and far slower vitality transition, the report says.

To conclude, pragmatism and compromise have to be thought-about to realize internet zero objectives, in response to WoodMac.

Learn the total report right here.