The lacklustre mixed efficiency of the sector’s majors got here regardless of the revival within the bellwether metals, however the broader market has been a blended bag in 2024.

Aluminium is buying and selling not far off 52-week highs, however zinc appears unlikely to breach $3,000 a tonne any time quickly and cobalt is bobbing alongside historic lows under $30,000 a tonne.

Nickel has been bumped up after lows within the mid-$15,000s final 12 months, however stays firmly caught in bear territory and lithium’s 2024 luck additionally appears at risk of really fizzling out.

Sentiment in direction of PGMs has hardly improved with each platinum and palladium drifting decrease in 2024. Even iron ore costs again above $100 a tonne – the bread and butter of the diversified majors – was not sufficient for traders to leap again into the sector.

Gold, copper increase

First Quantum Minerals with market valuation up 58% in US greenback phrases, made a welcome return at place 44 after dropping out on the finish of final 12 months following the closure of its Cobre Panama mine.

Amman Mineral continued its astounding run – the Indonesian copper and gold miner has added 380% in worth since its July itemizing and will quickly vie for a spot within the prime 10.

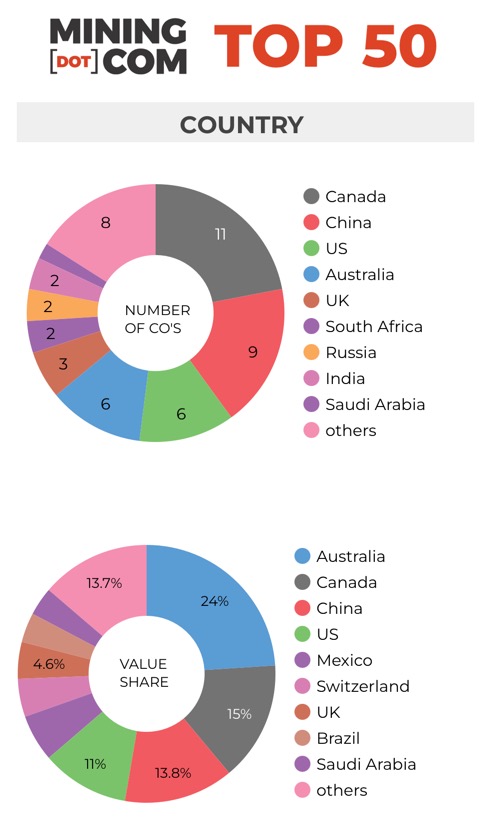

Lundin Mining joins the highest 50 for the primary time, leaping 5 locations to 48 and is already climbing due to the pink steel approaching 14-month highs. Lundin’s 25% rise in 2024 additionally restores Vancouver because the primary location amongst prime 50 headquarters after Pilbara Minerals’ exit this quarter.

Anglogold Ashanti’s re-entry boosts the variety of treasured metals miners within the prime tier to 10 and their collective worth to $183 billion.

China’s Yintai Gold, which in February picked up Canada’s Osino Sources, may additionally problem for a place within the higher echelon from its present 54th place ought to gold proceed to rally, however long run prime 50 participant KGHM has a hill to climb to make it again regardless of shares within the Polish mining firm rising 15% 12 months so far.

Pan American Silver, like its major steel, may trip gold’s coattails to grow to be the one silver-focused miner within the prime 50 following Fresnillo’s exit greater than a 12 months in the past. Silver is now the very best performing steel 12 months so far, up greater than 18%.

Diversified drubbing

Whereas the highest 50 mining firms as a complete drifted sideways throughout the quarter, the most important diversified firms confronted headwinds going into 2024, and uncharacteristically a number of the greatest names in mining function on the worst performers checklist for the quarter.

The one $100bn firms within the rating – BHP and Rio Tinto – had been each down by double digits on the finish of Q1 and Glencore’s rerating over the previous couple of years went into reverse with declines of 9% in 2024.

Vale’s pullback from its valuation on the finish of 2023 locations the inventory firmly in bear territory with losses of almost 24% in US greenback phrases. The Brazilian large bought 13% of its base metals unit for $3.4bn to amongst others, the Saudi Arabia’s sovereign wealth fund, however given the efficiency of nickel a separate itemizing appears off the desk for now.

Anglo American inventory had a reasonably uneventful Q1 2024 after the sharp H2 2023 sell-off sparked by copper steering, PGM and South African energy woes, and regardless of the dangerous information from its Woodsmith fertiliser venture in England.

Nonetheless, the counter has dropped under a $30 billion market cap for the primary time because the outset of the pandemic and losses for the previous 12 months prime 30%. Rumours that Glencore could also be after the Swiss behemoth’s bid for all of Teck Sources fell by have died down, most likely for the best causes.

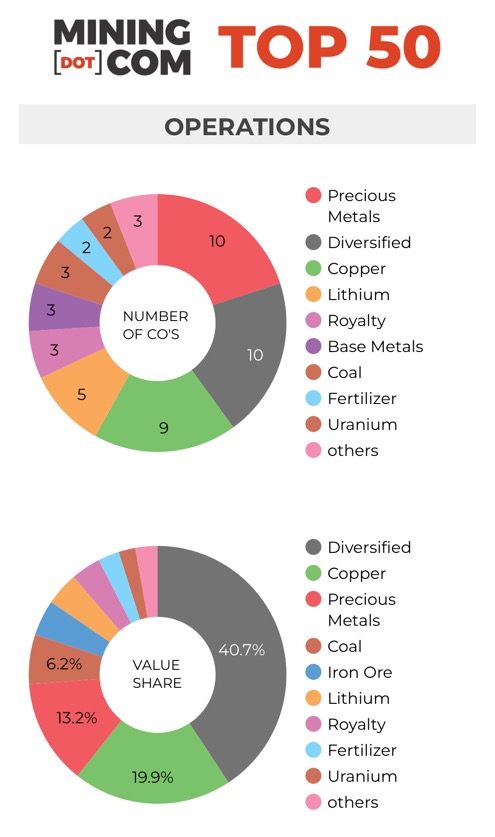

The rating stays prime heavy, however as a gaggle the historic prime 5 diversified mining firms’ share of the MINING.COM High 50’s general valuation fell to a brand new low of 29%, down from 36% on the finish of 2022.

China cheer

The historic prime 5 diversifieds ought to in equity be expanded to seven and embody Saudi Arabia’s Ma’aden and Zijin Mining, the extremely acquisitive Chinese language agency is up over 30% to this point this 12 months and seems to be effectively ensconced within the prime 10.

Xiamen-based Zijing on the finish of Q1 fell simply wanting a $60bn market value (certainly gold and copper’s run within the first week of Q2 has now lifted the inventory above that milestone).

On the very best performer checklist for the quarter, Zijin sits simply behind CMOC Group, previously China Molybdenum and for years earlier than being overtaken by Zijin probably the most worthwhile center kingdom mining inventory, and forward of Jiangxi Copper, which jumps 9 locations to 41 in Q1.

The ten Chinese language firms within the rating collectively are value $192bn or 14% of the general worth, up from 8 firms valued at $115bn and 9% of three years in the past.

Lithium loss

Three counters dropped out of the highest 50 throughout the first quarter. Brazil’s CSN Mineração, an iron ore miner, China’s Huayou Cobalt and Australian lithium producer Pilbara Minerals.

Pilbara Minerals solely simply misplaced out to Kinross Gold for the final spot as at end-March and lithium costs have recovered considerably this 12 months, however most likely not sufficient for the lithium sector to outperform gold shares in Q2.

The merger of Livent and Allkem to type Arcadium Lithium additionally didn’t end in a rise in lithium mining’s illustration within the rating. Arcadium Lithium has been hammered all the way down to under a $5bn valuation this 12 months.

From its top of a collective $119bn valuation on the finish of the second quarter of 2022, the mixed worth of the lithium shares within the prime 50 has now fallen to $59 billion.

Click on on the desk under for a full-size picture.

*NOTES:

Supply: MINING.COM, GoogleFinance, inventory alternate information, firm stories. Share information from primary-listed alternate at March 28, 2024 – March 29, 2024 shut of buying and selling transformed to US$ at cross-rates March 29, 2024.

Proportion change primarily based on US$ market cap distinction, not share value change on alternate in native forex.

As with every rating, standards for inclusion are contentious. We determined to exclude unlisted and state-owned enterprises on the outset attributable to a ignorance. That, in fact, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining, which owns the world’s largest gold mine, Eurochem, a significant potash agency, and plenty of entities in China and growing international locations world wide.

One other central criterion was the depth of involvement within the business earlier than an enterprise can rightfully be known as a mining firm.

As an illustration, ought to smelter firms or commodity merchants that personal minority stakes in mining property be included, particularly if these investments don’t have any operational part or warrant a seat on the board?

This can be a widespread construction in Asia and excluding most of these firms eliminated well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Ranges of operational or strategic involvement and measurement of shareholding had been different central concerns. Do streaming and royalty firms that obtain metals from mining operations with out shareholding qualify or are they only specialised financing automobiles? We included Franco Nevada, Royal Gold and Wheaton Treasured Metals on the premise of their deep involvement within the business.

Vertically built-in issues like Alcoa and power firms reminiscent of Shenhua Power or Bayan Sources the place energy, ports and railways make up a big portion of revenues pose an issue. The income combine additionally tends to vary alongside unstable coal costs. Identical goes for battery makers like CATL which is more and more shifting upstream, however the place mining nonetheless makes up a small portion of its valuation.

One other consideration is diversified firms reminiscent of Anglo American with individually listed majority-owned subsidiaries. We’ve included Angloplat within the rating however excluded Kumba Iron Ore during which Anglo has a 70% stake to keep away from double counting. Equally we excluded Hindustan Zinc which is listed individually however majority owned by Vedanta.

Many steelmakers personal and sometimes function iron ore and different steel mines, however within the curiosity of steadiness and variety we excluded the metal business, and with that many firms which have substantial mining property together with giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and lots of others.

Head workplace refers to operational headquarters wherever relevant, for instance BHP and Rio Tinto are proven as Melbourne, Australia, however Antofagasta is the exception that proves the rule. We take into account the corporate’s HQ to be in London, the place it has been listed because the late 1800s.

Please tell us of any errors, omissions, deletions or additions to the rating or counsel a unique methodology.