As economies develop, so does the demand for commodities, and finally the demand outstrips provide. That results in rising commodity costs, however the commodity producers don’t initially reply to the upper costs as a result of they’re not sure whether or not they are going to final. In consequence, the hole between demand and provide continues to widen, protecting upward stress on costs.

Ultimately, costs get so enticing that producers reply by making extra investments to spice up provide, narrowing the availability and demand hole. Excessive costs proceed to encourage funding till lastly, provide overtakes demand, pushing costs down. However whilst costs fall, provide continues to rise as investments made throughout the increase years bear fruit. Shortages flip to gluts and commodities enter the bearish a part of the cycle.

There have been a number of commodity supercycles all through the course of historical past. The latest one began in 1996 and peaked in 2011, pushed by uncooked materials demand from speedy industrialization happening in markets like Brazil, India, Russia and particularly, China.

We will speak concerning the cyclical nature of commodities basically, however we will additionally decide sure commodities to see whether or not they’re on the upswing or downswing.

Sprott earlier this yr identified that A new copper supercycle is rising, constructed on a number of rising geopolitical and market developments, together with electrification, nationwide safety considerations, environmental coverage, provide constraints and deglobalization.

Daybreak of a brand new supercycle

Whereas no two supercycles look the identical, all of them have three indicators in widespread: a surge in provide, demand and worth. The brand new commodity supercycle, nevertheless, might look a bit totally different from the earlier ones for one motive — the concentrate on makes an attempt to restrict international warming.

In accordance with S&P International, a extra aggressive dedication to the vitality transition throughout G-20 nations might additionally create the circumstances for a sustained surge in demand, provide and costs.

Like previously, commodity supercycles are often pushed by robust demand for uncooked supplies, manufactured supplies and sources of vitality. The vitality transition serves as a significant catalyst for all the important thing inputs to our renewable vitality infrastructure, taking demand to ranges by no means seen earlier than.

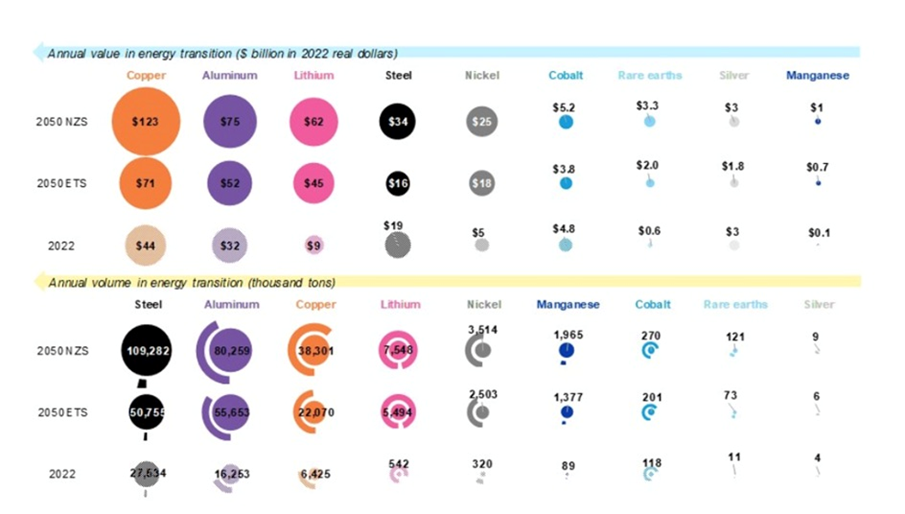

Demand for copper — the cornerstone for all electricity-related applied sciences — is ready to develop by 53% to 39 million metric tons by 2040, in keeping with BloombergNEF. Battery metals like lithium, cobalt and nickel will see even sooner development, reaching greater than 3 times the present demand ranges by 2030, says BNEF, with lithium rising the quickest with a seven-fold improve.

To achieve net-zero, demand for these key metals wanted for the deployment of vitality transition applied sciences similar to photo voltaic, wind, batteries and electrical automobiles will develop fivefold by 2050, BNEF provides.

One other proponent of the “inexperienced” commodities supercycle is Dr. Linda Yueh, adjunct professor of economics on the London Enterprise College.

In a 2023 podcast, Yueh stated the subsequent commodities cycle has begun in earnest and that this time it’s being led by battery metals. She identified that final yr, the Guangzhou Futures Alternate turned the fourth commodities change to launch contracts monitoring the value of lithium carbonate, utilized in electrical automobile batteries.

Final July the COMEX division of the New York Mercantile Alternate launched a lithium carbonate futures contract, whereas the London Metals Alternate launched new futures contracts to supply additional hedging and buying and selling alternatives for battery supplies.

“The solar doesn’t all the time shine and the wind doesn’t all the time blow so batteries are essential for the inexperienced transition,” Yueh observes. “Thus, the mining and processing of metals, such lithium and nickel, are driving a possible supercycle and raises attendant resilience considerations about provide chains in addition to environmental considerations.”

Whereas China, which controls about 80% of the world’s battery manufacturing capability, is at the moment the highest “commodity superpower,” the time period additionally applies to main lithium producers Australia and Chile.

For nickel, a mainstay of nickel-manganese-cobalt batteries, the highest three producers are Indonesia, the Philippines and Russia.

In accordance with a information article titled ‘Inexperienced Tech is Driving the Subsequent Commodities Supercycle’, Yueh believes that the main focus of this current supercycle more and more falls on provide chain resilience, noting that China has had a head begin and that it’s going to proceed to be a significant participant for years to return.

(Western nations are aiming to restrict China’s clean-technology dominance by means of tariffs and laws just like the US Inflation Discount Act — Rick)

A key space of focus will should be within the processing of battery metals, thereby serving to to diversify and add resilience to provide chains whereas contributing to the necessary value-added advantages to these nations that make such investments in processing and ending crops.

In March of this yr, The Financial Occasions of India cited three causes for the start of a brand new supercycle, not all of them inexperienced:

- The worldwide inhabitants is believed to have elevated past 8 billion individuals— a putting milestone for commodity analysts.

- Per-capita consumption of commodities stays low in rising market economies, notably India, which is simply at a comparatively early stage of the emergence of a large center class, like China.

- The next dedication to the vitality transition throughout G-20 nations might create the circumstances for a sustained surge in demand, provide, and costs. Battery metals similar to lithium carbonate are exhibiting the kind of sustained worth will increase that counsel a much bigger cycle is on its means, and hydrogen and carbon markets are in early days of exhibiting robust development in each provide and demand.

Jeff Curry spent 27 years at Goldman Sachs, the place he was head of worldwide commodities analysis. The person is aware of a factor or two about commodity supercycles.

He now works for Carlyle, a personal fairness agency, the place he’s chief technique officer for vitality pathways.

In talking just lately with Barron’s, Curry stated he’s extra satisfied than ever that commodities have entered a brand new supercycle that particularly will carry copper, gold and oil costs.

Curry says when (not if) the Federal Reserve cuts rates of interest in September, as anticipated, probably the most interest-rate delicate sectors will profit together with inexperienced vitality and copper.

However not like earlier supercycles, traders have to concentrate on a bigger ecosystem, not simply the supplies themselves however issues like batteries and so-called inexperienced metal. Biden’s Inflation Discount Act for instance gives gives $500 million to repower a metal plant with cleaner vitality in Ohio, Trump’s operating mate JD Vance’s residence state.

“Copper and inexperienced vitality are linked as a result of a lot copper is utilized in batteries and electrical automobiles,” says Curry. “Copper is concerned in all the important thing funding themes dealing with the world immediately. It embodies the demand round inexperienced spending, information facilities, and deglobalization.”

However what about new sectors like AI, know-how, healthcare and agriculture? Curry calls it “the revenge of the previous economic system” and we see it taking place throughout previous cycles.

The latest interval noticed the shale oil increase put downward stress on costs. Inflation and rates of interest have been low so traders moved into long-term property like synthetic intelligence shares.

To interchange capital that traders moved out of the bodily items market, governments world wide have created a requirement shock by means of spending such because the Inflation Discount Act and REPowerEU in Europe. Curry notes there might be $750 million spent on subsidies for inexperienced capex in 2024 alone.

At this time’s demand drivers for commodities Curry teams underneath the acronym RED: redistribution, environmental insurance policies and deglobalization.

An instance of redistribution is covid-19 stimulus checks mailed out to lower-income Individuals. The additional cash went instantly into consumption, not saving or investing. The lower-income group spends the next proportion of their revenue on commodities.

E stands for environmentalism. It has to do with the quantity of stimulus going to struggle local weather change. Better than $16 trillion has been spent on this decade alone — equal to all of China’s spend throughout the 2000s.

Lastly, deglobalization is the method of disconnection from different nations. China is an effective instance of this. China produces extra electrical automobiles than some other nation, but it additionally accepted 106 gjgawatts of coal-fired energy era capability final yr.

“So, between coal and all of the renewables, it’s disconnecting itself from the remainder of the world. That’s deglobalization,” Curry writes. “It goes to point out you that these three themes that drive every part are all linked. You possibly can join deglobalization again to redistributionist insurance policies. Take into consideration tariffs. Why do you place tariffs on? To guard your manufacturing. All these nations are constructing out their very own manufacturing. When you construct out your personal manufacturing, there’s extra commodity demand, extra capex, extra bodily every part.”

The position of inflation

The ultimate, most definitive indicator of a commodity supercycle is rising costs, and traditionally, supercycles are inclined to create inflation.

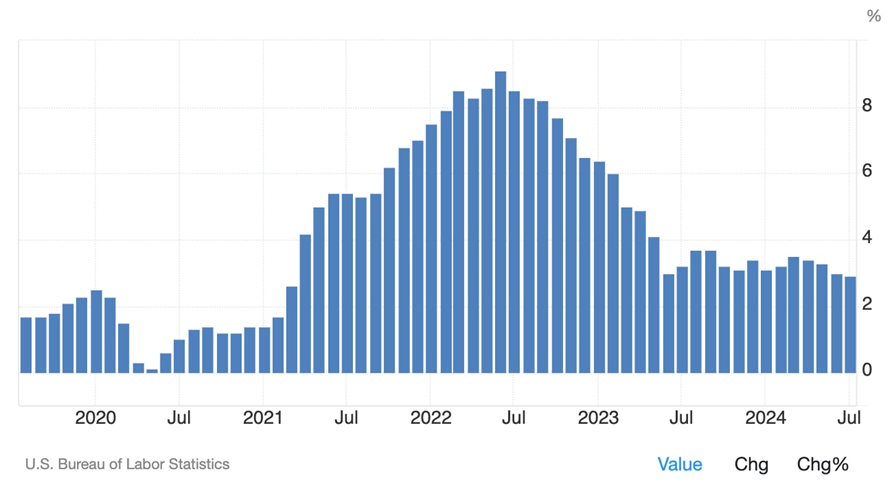

Over the previous two years the Federal Reserve and different central banks have been preventing inflation that at one level reached the very best in 40 years; not because the early Eighties had worth will increase been so excessive.

The Fed raised rates of interest to quell demand and produce costs right down to its goal inflation degree of two%. It labored. A sequence of fee hikes because the spring of 2022 lowered inflation from the 95 peak in June 2022 to the present 2.9%.

A outstanding feat and achieved with a “tender touchdown”, i.e. no recession.

Whereas some have argued that inflation would have come down anyway as soon as covid-related provide chain wrinkles have been ironed out, we’re not amongst them. The Fed needed to do one thing to sluggish runaway costs and financial tightening/ fee hikes have been the reply.

As The Economist writes in a latest article, “excessive rates of interest not the passage of time have restored worth stability”.

One other necessary level from The Economist article is that inflation could have stopped rising, however inflation isn’t gone; it has compounded through the years and the costs of many items, together with commodities, stay excessive.

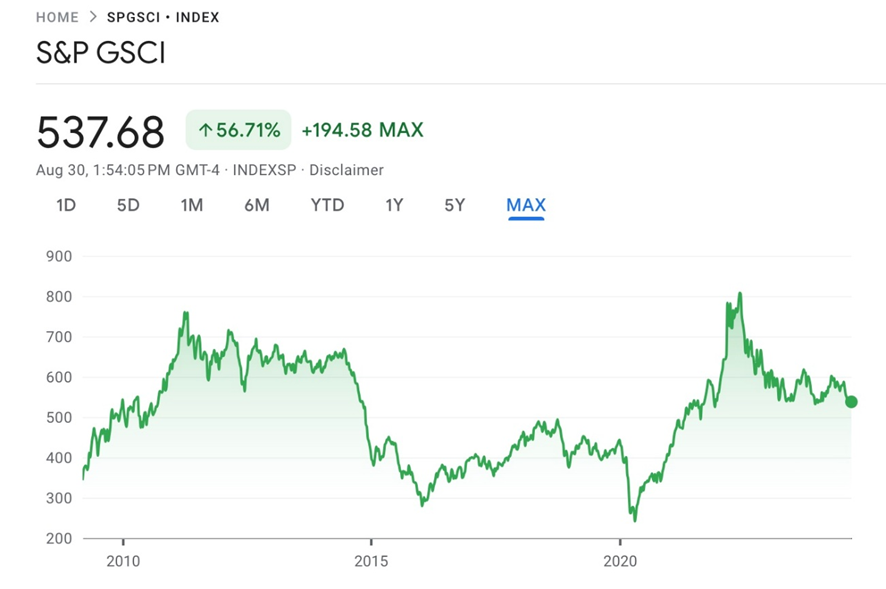

For proof of this, seek the advice of the chart under of the S&P GSCI commodities index. The index peaked in June 2022, lining up with the inflation peak, and has since declined. However commodity costs immediately, tracked by the index, are nonetheless the very best they’ve been since October 2014.

Supply: Google Finance

Supply: Google FinanceCommodity costs have stayed buoyant regardless of comparatively excessive rates of interest, round 5%, excessive bond yields and a excessive greenback — all headwinds for commodities.

Whereas the Fed’s assault on inflation hasn’t performed a lot to cut back demand — shopper spending elevated by 0.5% in July, and second-quarter GDP development rose by 3% — a slowing labor market has the Fed taking a look at a fee lower in September.

If rates of interest are lowered, there might be a direct impact on bond yields, which have already fallen this summer time. The US 10-year Treasury notice, for instance, has gone from a year-to-date excessive of 4.7% in April to the present 3.9%.

Supply: MarketWatch

Supply: MarketWatchBond yields and bond costs have an inverse relationship. May this be the beginning of a bull marketplace for bonds, and a bull marketplace for commodities as soon as the triad of decrease charges, decrease bond yields and a decrease greenback takes impact?

Look what occurred to gold when the Fed final week telegraphed an rate of interest lower. Spot gold set a file $2,531.60 on Powell’s dovish feedback. Silver adopted gold larger, breaking by means of $30/oz. Market individuals ought to see this as a dry run for what truly occurs when charges are lowered. Commodities and valuable metals, imo, appear to be the place to be.

The brand new commodity supercycle is exclusive within the sense that provides for a number of commodities are set to peak or have already peaked, inflicting market deficits and better costs.

Beforehand, surging demand and falling provide are the hallmarks of a market in decline (i.e. coal). However now, it’s not a lot about producers being reluctant to take a position, however extra of demand rising too quick for provide to catch up.

Copper

Take copper, for instance.

On the demand facet, electrical grids should be up to date, and governments are embarking on large-scale infrastructure investments which can be copper-intensive.

Together with the same old purposes in building wiring and plumbing, transportation, energy transmission and communications, there may be now added demand for copper in electrical automobiles, photo voltaic panels, wind generators, and vitality storage.

Extra copper is being demanded by the electrification of public transportation techniques, 5G and AI.

Copper costs could have come off the boil just lately (from a excessive of $5.11/lb in Might) attributable to issues in China however the structural provide deficit is actual and protecting costs elevated.

Benchmark Mineral Intelligence (BMI) forecasts international copper consumption to develop 3.5% to twenty-eight million tonnes in 2024, and for demand to extend from 27 million tonnes in 2023 to 38 million tonnes in 2032, averaging 3.9% yearly development.

But the US Geological Survey studies provide from copper mines in 2023 amounted to solely 22 million tonnes. If the copper provide doesn’t develop this yr, we’re taking a look at a 6Mt deficit.

5 the reason why we’re getting into the subsequent copper supercycle — Richard Mills

Copper: Humanity’s first and most necessary future steel — Richard Mills

Silver

One steel that has already plunged into deficit territory is silver. Whereas typically purchased for funding functions, silver is primarily used for industrial purposes similar to electronics and automotive. It’s additionally a key ingredient in photo voltaic panels, and because the world strikes in direction of renewables, demand from that sector has grown exponentially.

The Silver Institute reported a 184.3 million-ounce deficit in 2023 on the again of sturdy industrial demand.

SI expects demand to develop by 2% this yr, led by an anticipated 20% achieve within the PV market. Industrial fabrication ought to put up one other all-time excessive, rising by 9%. Demand for jewellery and silverware fabrication are predicted to rise by 4% and seven%, respectively.

Whole silver provide ought to lower by 1%, which means 2024 ought to see one other deficit, amounting to 215.3Moz, the second-largest in additional than 20 years.

Silver is within the fourth yr of a scarcity, with mined provide seemingly unable to maintain up with demand, which is strongly influenced by the photo voltaic and electronics markets.

Silver appears to be like prepared to tear — Richard Mills

Iron ore

Admittedly the iron ore worth has taken a beating of late, largely as a result of unfavourable outlook for Chinese language demand, which has been hit by a protracted property disaster.

Regardless of the federal government’s assist for housing and different industries, on June 3 the iron ore worth tumbled to its lowest in six weeks.

Earlier this week, nevertheless, the steelmaking ingredient was again above $100 a ton. Merchants are seeing China’s drop in inventories as a tentative signal that the interval of oversupply is beginning to ease.

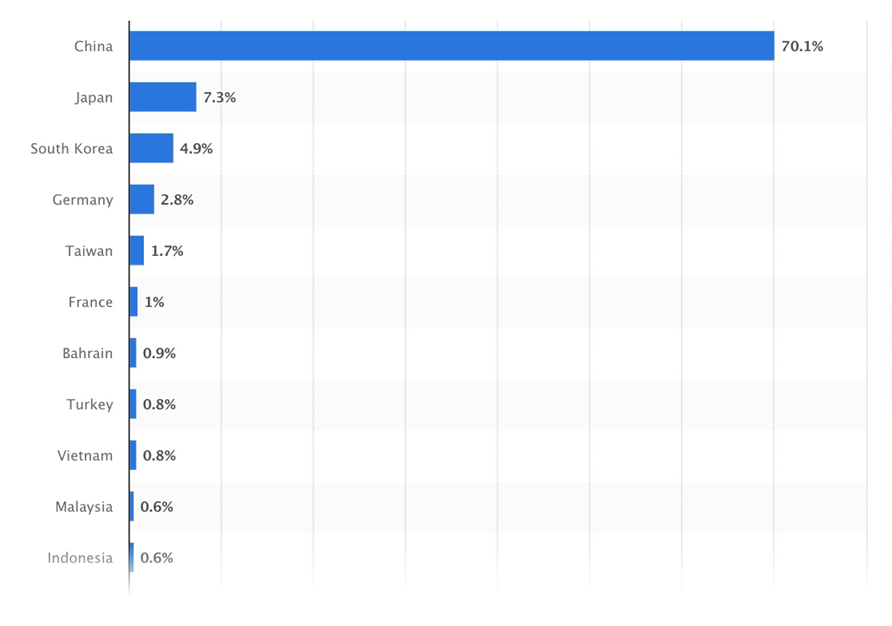

China imports probably the most iron ore of all nations, adopted by Japan and South Korea.

Conclusion

There have been a number of commodity tremendous cycles all through the course of historical past. The latest one began in 1996 and peaked in 2011, pushed by uncooked materials demand from speedy industrialization happening in markets like Brazil, India, Russia and particularly, China.

The primary inexperienced shoots of a brand new commodity supercycle, one primarily based on uncooked supplies for supplying the brand new electrified economic system, are rising.

Silver and gold are up over 20% thus far this yr regardless of the headwinds of excessive bond yields and a robust US greenback.

Copper has come down from its $5 a pound pinnacle, however at $4.22 miners can nonetheless earn cash, though it’s not excessive sufficient to incentivize new mines.

Iron ore has had a troublesome go of it however it seems that the glut in provide is lessening and the value is basing round $100 a ton.

We all know one factor for certain. The case for all commodities rests upon the US greenback. As soon as the Fed begins chopping rates of interest, the greenback will weaken and all the commodities complicated will strengthen.

Authorized Discover / Disclaimer

Forward of the Herd publication, aheadoftheherd.com, hereafter referred to as AOTH.

Please learn all the Disclaimer rigorously earlier than you employ this web site or learn the publication. If you don’t conform to all of the AOTH/Richard Mills Disclaimer, don’t entry/learn this web site/publication/article, or any of its pages. By studying/utilizing this AOTH/Richard Mills web site/publication/article, and whether or not you truly learn this Disclaimer, you might be deemed to have accepted it.