In personal conversations, senior trade executives attending the annual LME Week mentioned it’s probably that the important thing processing charge will fall to a stage the place smelters will wrestle to show a revenue. The 2 sides started holding conferences this week to share their views available on the market, though they’ve but to place any numbers on the desk, they mentioned. There’s a broad expectation that the talks would be the hardest in years.

Whereas the annual negotiations don’t get a lot consideration outdoors of the metals world, this 12 months the result might have far-reaching ramifications for the copper market. Smelter closures might reshape the map of worldwide refined copper provide at a time of rising considerations about Chinese language dominance over vital minerals. And, after a 12 months by which the marketplace for refined copper has been in oversupply whilst miners struggled to elevate output, the squeeze on smelters is prone to crimp refined provide — simply as some count on China’s newly introduced stimulus to kickstart consumption.

Smelters usually derive a big a part of their earnings from processing charges which might be deducted from the price of concentrates, the partly processed ore that they purchase from miners. The trade agrees a benchmark for remedy and refining prices (TC/RCs) within the fourth quarter of every 12 months — the charge is used as a reference for long-term provide contracts, whereas different advert hoc gross sales all year long are priced primarily based on situations on the time.

The mounting squeeze on ore provides has led to a large gulf between final 12 months’s benchmark — which was set a $80 per ton of ore and eight cents per pound of contained steel — and the phrases being agreed in spot offers. The scenario has grown so extreme that the charges have turned damaging; merchants and smelters have been paying extra for copper ore than the copper contained in it will fetch as soon as processed, a extremely uncommon scenario.

In a straw ballot of greater than two dozen miners, merchants and smelters, respondents who offered an estimate mentioned the benchmark would probably be agreed between $20 and $40 a ton and 2c to 4c a pound. A number of respondents recommended that the negotiations might result in a breakdown of the benchmark system, a possible watershed second for the trade.

This 12 months, the benchmark is anticipated to be negotiated with Chilean miner Antofagasta Plc, which prior to now has tended to strike a more durable negotiating line than American rival Freeport-McMoRan Inc. The US firm has typically set the benchmark lately, however it would have far fewer concentrates to promote subsequent 12 months after constructing an enormous new smelter subsequent to its largest mine in Indonesia. Chief government officer Kathleen Quirk mentioned in an interview that Freeport gained’t set the benchmark this 12 months.

A spokesperson for Antofagasta declined to touch upon the negotiations.

Representatives of Chinese language smelters in London this week mentioned they’re emphasizing to Antofagasta that the trade already faces widening losses as a result of there may be not sufficient focus to go round, and warning that an aggressive lower to the benchmark charges might result in manufacturing cuts and trigger everlasting harm to the trade. Officers at Chinese language smelters mentioned the trade would most likely be lossmaking at charges beneath about $35 to $40 a ton.

“There’s been a lot new capability developed for smelters in China through the years, and there’s simply not the focus out there to feed the whole lot,” Freeport’s Quirk mentioned in London this week. “However for focus producers which might be counting on smelters, they must assume: ‘Properly, I don’t wanna push these guys out of enterprise.’”

The massive mismatch between focus provide and demand stems from the commissioning of recent crops in India, Indonesia and the Democratic Republic of Congo, in addition to a number of main plant expansions in China. It’s additionally been a weak 12 months for mine provide, however the fast growth in smelting capability has fueled expectations that smelting margins will stay severely constrained whilst mined output rebounds.

“We’ll preserve our manufacturing as we do have long-term provide contracts, and we’ll must stay with these decrease TC/RCs for the approaching 12 months,” mentioned Toralf Haag, who final month took over as CEO of Aurubis AG, Europe’s largest copper smelting group. “We’re optimistic that the scenario will begin to resolve itself over the approaching 12 months — some refining capability will come off-stream, and a few further mining capability will come onstream.”

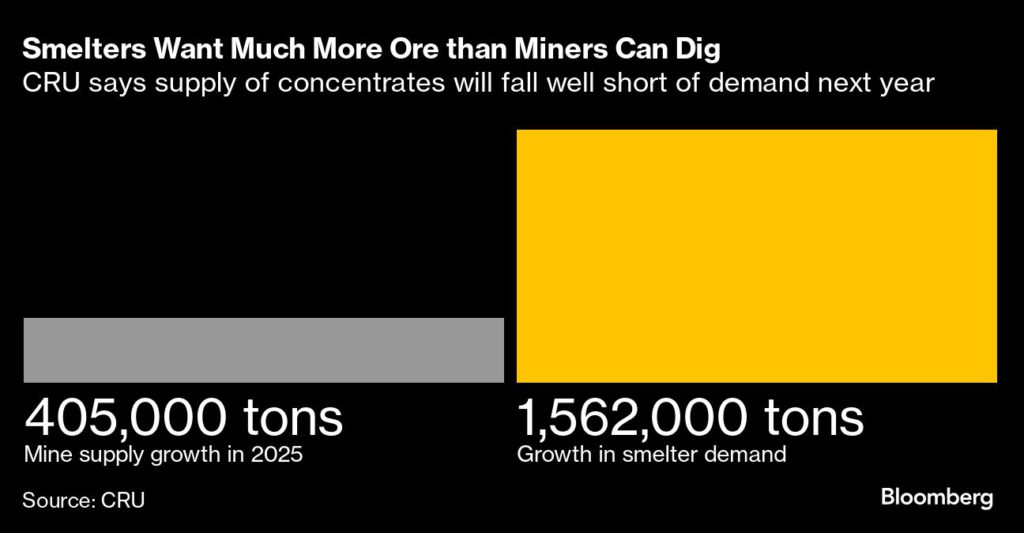

Researcher CRU estimates that the distinction between smelters’ wants and focus provide will balloon to about 1.2 million tons, the most important deficit in a minimum of a decade.

It expects that 70% of the hole can be resolved by smelters decreasing their working charges, however the remaining hole will should be solved by short-term or everlasting plant closures. And the extra aggressive miners are in driving down TC/RCs, the extra in depth the cuts can be, in keeping with Erik Heimlich, the consultancy’s head of copper and zinc.

“Miners are in an excellent place and so they might pressure a really low TC/RC, however there are causes that they gained’t wish to go as little as attainable,” he mentioned in an interview. “These are long-term relationships, and for those who go very low, you’ll find yourself with an trade that loses a variety of gamers on the demand aspect.”

Learn Extra: Mining trade struggles with valuation hole amid shift to copper