On the half-year mark, it seems that our prediction was bang-on.

Whereas gold and silver costs had been down on Monday, July 8, the outlook for valuable metals is nice, as for industrial metals together with copper as a consequence of impending Fed rate of interest cuts, at the very least one by 12 months’s finish.

The yellow steel reached $2,393/ounceson Friday following the discharge of US NonFarm Payrolls Knowledge. The weaker labor market and rising unemployment price, which hit 4.1% in June, is fodder for the US Federal Reserve to slash rates of interest, presumably as soon as in September and a second time in December.

“We now have definitive proof of labour market cooling with a considerably alarming rise within the unemployment price in latest months that ought to give policymakers ‘extra confidence’ that client inflation will quickly return to the two.0 per cent goal on a sustainable foundation,” mentioned Scott Anderson, chief US economist at BMO Capital Markets, through The Globe and Mail.

In remarks to Congress, Fed Chair Jerome Powell mentioned the US is “now not an overheated economic system” with a job market that has “cooled significantly” and is again the place it was earlier than the pandemic, suggesting the potential for price cuts is changing into stronger. (Reuters, July 9, 2024)

Powell informed senators that inflation has been enhancing in latest months. The chart under reveals the annual inflation price slowed to three.3% in Might, in comparison with 3.4% in April and three.5% in March.

What’s driving commodities?

Some say that commodities are hedges towards inflation and that folks purchase them when inflation is excessive. Whereas there may be some fact to that, it doesn’t clarify why the greenback is surging concurrently a number of commodities together with gold, silver, copper, zinc, aluminum, molybdenum and crude oil are all rising in worth. As for inflation? It’s truly been falling, because the chart above proves.

I consider the extra doubtless cause has to do with rates of interest. We’ve confirmed in a number of articles that rates of interest management power or weak spot within the greenback.

Why the greenback is rising as treasury yields fall

Usually, the greenback and US bond yields rise and fall collectively, signaling a constructive correlation between the 2. Conversely, the worth of a bond and its yield are negatively correlated. The decrease the worth, the upper its yield. A rising yield favors greenback bulls. Falling bond yields make for a softer greenback. These are generally accepted financial rules.

Demand for {dollars} has been sturdy, mirrored in a US greenback index (DXY) over 105. DXY began 2024 at 102.49, and it’s now at 105.15, a achieve of two.5%. That is partly because of the greenback functioning as a protected haven throughout battle — the conflicts in Gaza and the Ukraine have raged all 12 months and present no signal of ending — together with rates of interest at their highest ranges in 22 years, @ 5.25 to five.50%.

Take into account: if inflation begins heading again up, and the Fed goes again to climbing rates of interest, the next greenback will sink commodity costs. In different phrases, the greenback is a stronger variable than inflation relating to predicting whether or not commodities rise or fall.

Buyers ought to, nonetheless, purchase commodities as safety towards a falling forex. When the greenback is weak we purchase “actual” issues like metals, oil, land, and so on. If you already know the greenback’s going to weaken the perfect place to park your cash is in financial metals like gold and silver. Different commodities additionally do nicely in a low-dollar setting as a result of extra models of a commodity may be purchased with {dollars}, and people with non-dollar currencies can purchase extra {dollars} with their house currencies. They use these {dollars} to purchase commodities priced in US {dollars}.

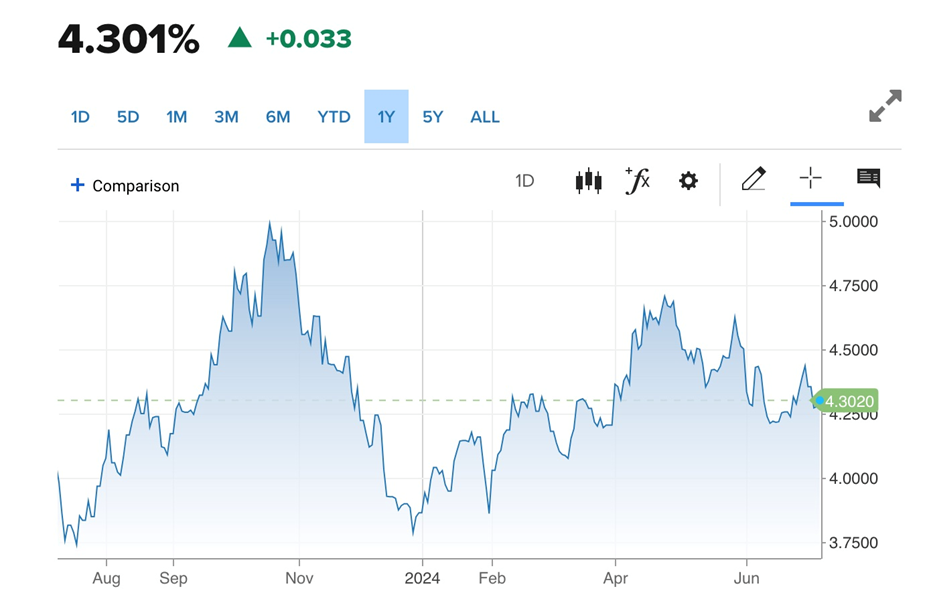

Bond traders are interested in US Treasuries not solely as a result of they’re a protected haven however as a result of they pay a comparatively excessive yield proper now — 4.30% for the 10-year, 4.62% for the 2-year and 4.49% for the 30-year.

The acquisition of extra commodities in a low-dollar setting exacerbates shortages in markets exhibiting low provides. All three metals being mentioned right here — gold, silver and copper — are both undersupplied now or will probably be within the close to future.

The greenback hasn’t dropped but. However these within the know (together with us at AOTH) consider it should. A Goldman Sachs be aware to shoppers Monday mentioned hedge funds purchased commodity-sensitive shares within the week to July 5 on the quickest tempo in 5 months. (BOE Report, July 8, 2024)

If commodity costs are doing nicely now, whereas the greenback is excessive, how a lot increased may they go when rates of interest and the greenback fall?

Gold

The specter of decrease rates of interest is a bullish sign for gold. FX Avenue commented on Monday that gold continues to achieve help from geopolitical and macro components, reminiscent of ongoing conflicts within the Center East and Ukraine.

Egon von Greyerz, chairman of Gold Switzerland, factors out that the political instability inherent in present and future elections this 12 months is one other good cause for proudly owning valuable metals. Particularly provided that out-of-control authorities spending is prone to be the predominant coverage response. Examples are the brand new Labour authorities in Britain, France’s new coalition authorities, and “an insoluble debt disaster” within the US regardless of which presidential candidate wins in November.

In the meantime, de-dollarization by international locations at odds with the US, who worry that the US may freeze their greenback property like Washington did to Russia following the invasion of Ukraine, is growing the enchantment of gold as a foreign-exchange various.

BRICS nations, now wealthier than the G7 and accounting for one-third of the world’s GDP, are reportedly discussing the launch of a BRICS cryptocurrency probably backed by gold.

A latest report from the World Gold Council sees local weather change as one other supply of safe-haven gold demand:

Gold’s carbon profile and decarbonisation potential could reinforce or amplify gold’s position as a protected haven asset, danger hedge and retailer of worth during times of market stress.

“This lends additional credence to our evaluation suggesting that gold’s long-term returns could also be extra sturdy than these of many mainstream asset courses within the context of a variety of local weather eventualities.”

Though a latest evaluation finds gold solely turns into an inflation hedge over lengthy intervals of time; 10 years is just too brief.

In a paper, Prof. Campbell Harvey of Duke College and co-author Claude Erb write that, for traders who add gold of their portfolio immediately, with excessive inflation and gold costs near an all-time excessive, the expectation that gold will hold its actual worth within the subsequent 10 years will not be in line with historical past.

“When gold is at an all-time excessive, the anticipated returns over the following 10 years — in line with historic expertise — could be very low,” Harvey mentioned.

As proof of gold appearing as a longer-term hedge, Campbell and Harvey provide the instance of a Roman centurion who was paid 38.58 ounces of gold two millennia in the past.

“At immediately’s worth of gold, it could be $86,300, which could be very near the wage of a U.S. Military captain with six years of expertise — $85,600,” Harvey mentioned.

Excessive central financial institution demand, which accounts for a few quarter of the gold market, is a further think about favor of gold.

In its annual survey, the World Gold Council mentioned extra central banks plan so as to add to their gold reserves inside a 12 months, regardless of excessive costs. Gold hit a record-high $2,449.89 per ounce on Might 20. The survey mentioned 29% of central banks count on their gold reserves to extend within the subsequent 12 months, the best degree for the reason that WGC started the survey in 2018, and in contrast with 24% in 2023.

Livemint says relentless demand from retail consumers in China and India, — the 2 largest bodily gold customers — together with fund traders, futures merchants and central banks, drove gold to unprecedented heights.

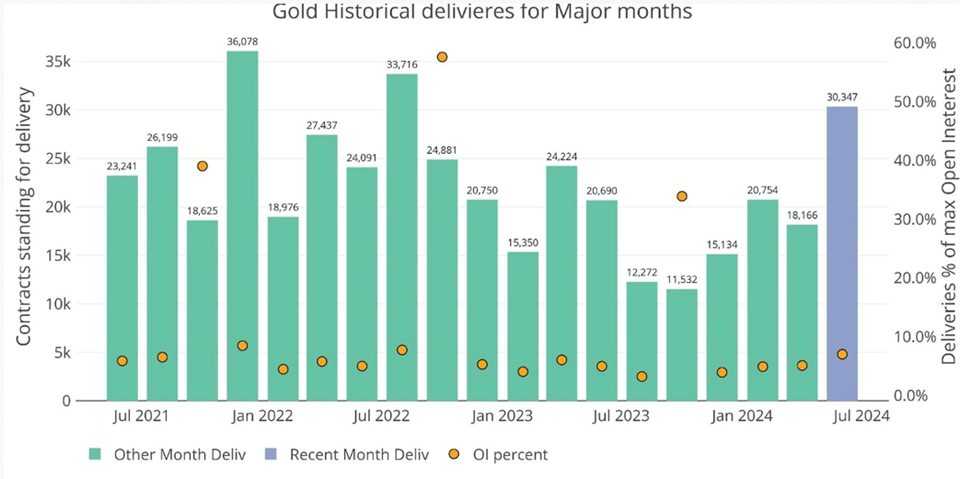

In the meantime the CME Comex, an alternate the place futures are traded for gold, silver, and different commodities, has been seeing huge strikes in silver and gold. This implies extra individuals are taking supply of bodily steel.

In line with Schiff Gold, Might confirmed open curiosity in gold at nicely above pattern — 30,000 contracts stood for supply in June, the biggest quantity since August 2022.

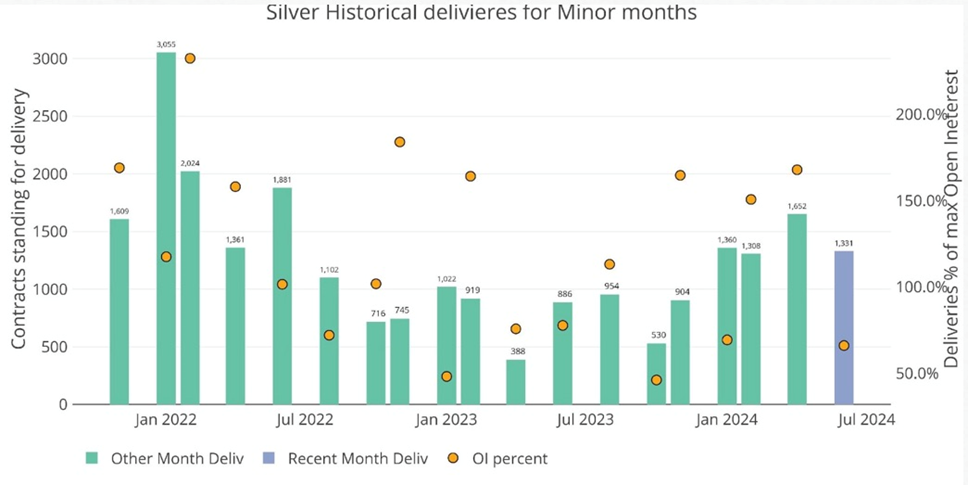

Exercise in silver has additionally picked up after a quiet 2023.

As for gold exchange-traded funds, a serious supply of gold funding demand, outflows have flipped to inflows. Globally, gold ETFs noticed the second consecutive month of inflows in June as a consequence of additions to holdings by Europe- and Asia-listed funds, the World Gold Council (WGC) mentioned on Tuesday, through Reuters. (though collective holdings stay at their lowest since 2020)

Lastly, gold costs are pushing increased as a consequence of a shortfall of mined gold.

In a world of useful resource depletion, it falls to gold exploration corporations to fill the hole with new deposits that may ship the type of manufacturing required to fulfill gold demand, which is at present out-running provide.

The gold market continues to expertise tightness as a consequence of difficulties increasing present deposits, and a pronounced lack of enormous discoveries lately.

In 2023, 4,448 tonnes of gold demand minus 3,644t of gold mine manufacturing left a deficit of 804t. Solely by recycling 1,237t of gold jewellery may the demand be met. (The World Gold Council: ‘Gold Demand Traits Full 12 months 2023’)

That is our definition of peak gold. Will the gold mining business have the ability to produce, or uncover, sufficient gold, in order that it’s capable of meet demand with out having to recycle jewellery? If the numbers mirror that, peak gold can be debunked. We’ve been monitoring it since 2019, and it hasn’t occurred but.

Silver

Like gold, we will examine the supply-demand image for silver to get a way of whether or not we’ve reached peak mine provide.

At AOTH we differentiate between the whole silver provide, which lumps in recycled silver with mined silver, versus mine provide by itself.

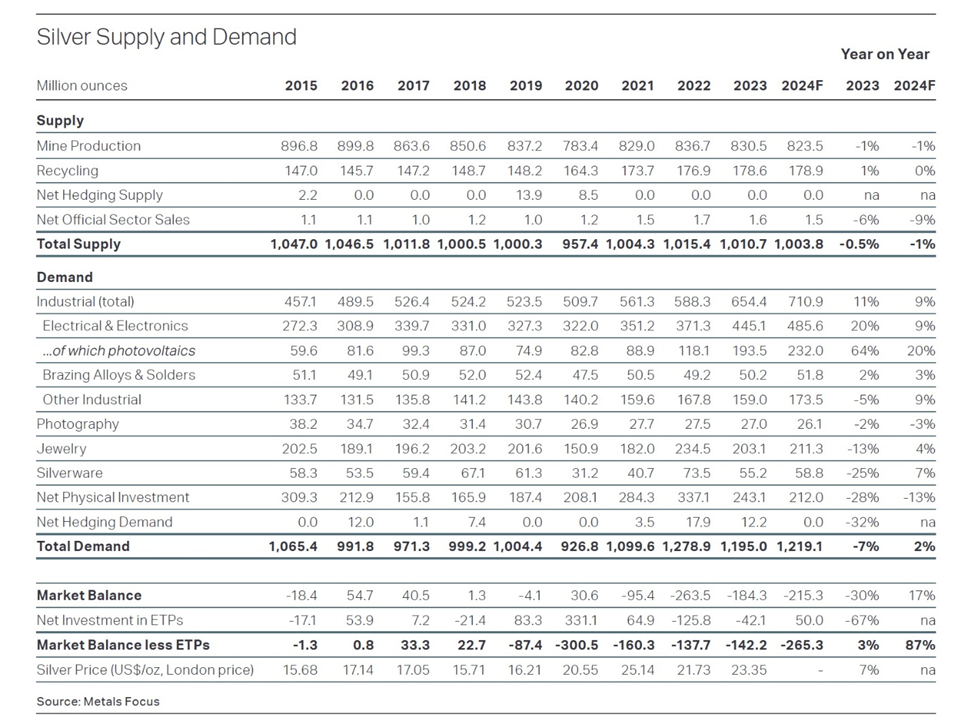

In line with the 2024 Silver Survey, in 2023 world mine manufacturing fell 1% to 830.5 million ounces, or 25,830 tonnes. Weaker output in Mexico owing to a strike at Newmont’s Penasquito mine and decrease ore grades in Argentina had been key drivers of the autumn.

Silver recycling inched up by 1% to a 10-year excessive of 178.6Moz. Mixed, subsequently, now we have complete silver provide reaching 1.010 billion ounces in 2023.

How about demand? In line with the survey, following a report 2022, world silver demand in 2023 fell 7% to 1.195Moz. It was nonetheless 9% increased than the following highest yearly complete. Offtake from the commercial sector achieved a report excessive final 12 months, rising 11% to 654.4Moz, primarily as a consequence of positive aspects within the photo voltaic sector.

(Keep in mind: Whereas a lot of the mined gold remains to be round, both solid as jewellery, or smelted into bullion and saved for funding functions, the identical can’t be mentioned for silver. It’s estimated round 60% of silver is utilized in industrial functions, like photo voltaic panels and electronics, leaving solely 40% for investing. Of the 60% used for industrial functions, virtually 80% leads to landfills.)

2023 demand of 1.195 billion ounces outstripped provide of 1.010Boz, by 185Moz. However keep in mind, recycling is included within the complete provide. After we take recycling out, 178Moz, we get a fair higher deficit of 364.5Moz. (1,195,000,000 minus 830,500,000 = 364,500,000)

That is important, as a result of it’s saying that mined silver provide final 12 months was unable to fulfill complete demand, industrial plus funding, of 1.195 billion ounces. It fell brief by 185Moz, and that was together with recycling.

That is our definition of peak mined silver. Will the silver mining business have the ability to produce, or uncover, sufficient silver that it’s capable of meet demand with out having to recycle? If the numbers mirror that, peak mined silver can be debunked.

At AOTH, we all know that silver costs observe gold costs, and that there’s roughly the identical quantity of investable grade silver above-ground as gold. But silver is at present 1/76th the worth of gold. Which means when silver is extremely demanded, like now — it’s each a financial and an industrial steel — the worth typically slingshots previous gold.

Supply: McAlvany

To this point this 12 months, silver has outperformed gold, gaining 33% towards gold’s 15% rise. The identical factor occurred in 2020, when the pandemic precipitated the “worry commerce” in valuable metals.

Gold is shifting increased primarily as a consequence of central financial institution shopping for, and bodily gold purchases in Asia.

Who’s shopping for all of the silver? India and silver-backed ETFs.

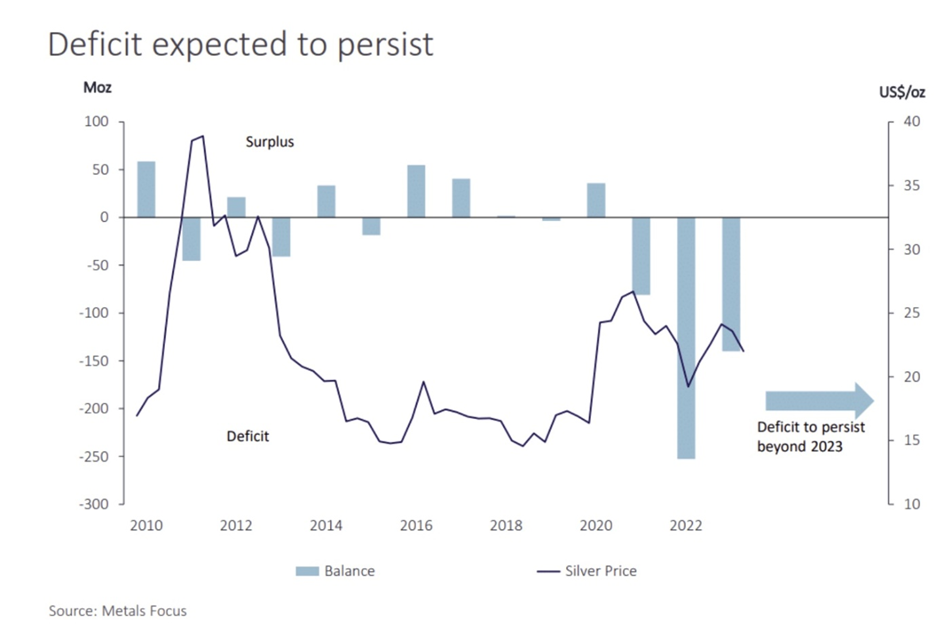

The Silver Institute reported a 184.3 million-ounce deficit in 2023 on the again of sturdy industrial demand.

In an April commentary, SI mentioned industrial demand rose 11% final 12 months to a brand new report of 654.4Moz, smashing the outdated report set in 2022.

In actual fact demand exceeded provide for the third 12 months in a row.

Increased-than-expected photovoltaic (PV) capability additions and quicker adoption of new-generation photo voltaic cells raised electrical & electronics demand by a considerable 20%, to 445.1Moz, the institute mentioned.

The Silver Institute expects demand to develop by 2% this 12 months, led by an anticipated 20% achieve within the PV market. Industrial fabrication ought to submit one other all-time excessive, rising by 9%. Demand for jewellery and silverware fabrication are predicted to rise by 4% and seven%, respectively.

Whole silver provide ought to lower by one other 1%, that means 2024 ought to see one other deficit, amounting to 215.3Moz, the second-largest in additional than 20 years.

Deficits ought to persist past 2024, the Silver Institute mentioned, citing Metals Focus. In line with Metals Focus, this is because of important and increasing industrial demand for silver.

Copper

Copper could have come off the boil lately as a consequence of issues in China however the structural provide deficit is actual and retaining costs elevated.

Benchmark Mineral Intelligence (BMI) forecasts world copper consumption to develop 3.5% to twenty-eight million tonnes in 2024, and for demand to extend from 27 million tonnes in 2023 to 38 million tonnes in 2032, averaging 3.9% yearly development.

But the US Geological Survey reviews provide from copper mines in 2023 amounted to solely 22 million tonnes. If the copper provide doesn’t develop this 12 months, we’re taking a look at a 6Mt deficit.

Mining corporations are seeing their reserves dwindle as they run out of ore. Commodities funding agency Goehring & Rozencwajg says the business is “approaching the decrease limits of cut-off grades and brownfield expansions are now not a viable answer. If that is appropriate, then we’re quickly approaching the purpose the place reserves can’t be grown in any respect.”

With out new capital investments, Commodities Analysis Unit (CRU) predicts world copper mine manufacturing will drop to under 12Mt by 2034, resulting in a provide shortfall of greater than 15Mt. Over 200 copper mines are anticipated to expire of ore earlier than 2035, with not sufficient new mines within the pipeline to take their place.

Final 12 months, the federal government of Panama ordered First Quantum Minerals (TSX:FM) to close down its Cobre Panama operation, eradicating practically 350,000 tonnes from world provide.

A strike at one other giant copper mine, Las Bambas in Peru, briefly halted shipments.

Copper specialist Anglo American says it’s scaling again output by about 200,000 tons, owing to move grade declines and logistical points at its Los Bronces mine. Los Bronces manufacturing is predicted to fall by practically a 3rd from common historic ranges subsequent 12 months because the miner pauses a processing plant for upkeep, Reuters mentioned.

Chile’s copper output has been dented by a long-running drought within the nation’s arid north. State miner Codelco’s 2023 manufacturing was the bottom in 25 years.

All 4 of Codelco’s megaprojects have been delayed by years, confronted value overruns totaling billions, and suffered accidents and operational issues whereas failing to ship the promised enhance in manufacturing, in line with the corporate’s personal projections.

There are additionally considerations about Zambia, Africa’s second largest copper producer, the place drought situations have lowered dam ranges, creating an influence disaster that threatens the nation’s deliberate copper growth.

Ivanhoe Mines (TSX:IVN) reported a 6.5% Q1 drop in manufacturing on the world’s latest main copper mine, Kamoa-Kakula within the DRC.

The tightness of the copper focus market has been mirrored in remedy and refining costs plummeting from over $90 per tonne to under $10/t.

(Miners pay smelters a price to course of copper focus into refined steel, to offset the price of the ore. TC/RCs fall when tight focus provides squeeze smelters’ revenue margins.)

This drastic discount compelled Chinese language smelters, chargeable for round half of worldwide refined copper manufacturing, to think about a 5-10% manufacturing minimize.

That was in March. By July, the state of affairs had flipped 180 levels. Now China is seemingly swimming in copper, a lot in order that it’s exporting refined copper to London Steel Alternate warehouses, that are full to the brim. LME warehouse shares are reportedly above 190,000 tonnes for the primary time since final October.

The Monetary Occasions wrote on June 18 that The largest glut of copper in 4 years has constructed up in Chinese language warehouses, after a worth soar and tepid client demand prompted producers in Asia’s largest economic system to drag again on shopping for the world’s most essential industrial steel. Shares of the steel in Shanghai Futures Alternate warehouses have grown to their highest degree since 2020 at about 330,000 tonnes this month, in line with Bloomberg knowledge. Earlier than then, the final time they hit this degree was in 2015.

The rise in copper inventories displays China’s actual property downturn in addition to sluggish manufacturing and credit score exercise, as Beijing shies away from instantly stimulating family consumption. Within the 4 weeks for the reason that report excessive, copper has fallen 13 per cent to $9,600 per tonne, weighed down by weak Chinese language demand.

But as warehouse shares construct up in China and the UK, the nation is importing giant quantities of crimson steel. Reuters metals columnist Andy Residence wrote on July 10 that China imported 1.61 million tons of refined copper within the first 5 months of the 12 months, a year-on-year enhance of 19.2%.

The comparability is considerably flattered by a low base in early 2023, when imports had been comparatively weak. However imports over the past 12 months have been a strong 3.98 million tons, a degree exceeded solely as soon as on an annual foundation in 2020.

Exports jumped to 73,860 tons in Might, the best month-to-month quantity since Might 2016, as smelters exported right into a worthwhile arbitrage window with the London market…

The core driver of rising imports has been the Democratic Republic of Congo, which final 12 months overtook Chile as China’s high provider of refined copper.

Imports from the Congo grew from 480,000 tons in 2020 to 870,000 in 2023. Volumes thus far this 12 months have jumped by one other 78% to 548,000 tons.

China is the world’s largest copper client so China’s actions available in the market are watched carefully as a result of they have an effect on the worth.

To make sure self-sufficiency, China has expanded its community of copper smelters, that means it should import far more copper ore for processing domestically.

“Like all international locations, China sees a strategic want for copper — notably now with the expansion in inexperienced vitality functions — and China like different international locations desires to make sure self sufficiency,” mentioned Craig Lang, principal analyst at researcher CRU Group.

“China will account for about 45% of worldwide refined copper output this 12 months, in line with CRU,” Bloomberg wrote in 2023.

Let’s summarize what’s happening right here. China is increasing its smelter capability. To do that, it requires extra ore and it’s getting it largely from the DRC, which has overtaken Peru because the second-largest copper-producing nation. Imports are surging concurrently warehouses are filling up.

China has tricked the market earlier than into believing there’s a surplus when actually there’s a deficit. I uncovered this “Copper Con” in March 2015. Right here’s what occurred:

China discovered each analyst they might and invited them to China. The group was proven a number of warehouses stacked with copper to the rooftops. There was a lot copper the bottom was compacting, mentioned one analyst. One other mentioned the stacks had been falling over like dominos. The world purchased the excess story, swallowed it hook line and sinker. Headlines screamed ‘China has sufficient copper!’

In fact it wasn’t true. China wanted copper, and what they’d, all of two million tonnes, was tied up in financing offers. At anybody time there are at the very least 1 million tonnes in transport, or someplace within the provide chain that has already spoken for, i.e.., not obtainable.

Exposing the copper surplus delusion

The world continues to get conned. Yearly so-called “consultants” predict a surplus; as an alternative what occurs? Deficit after provide deficit.

It is sensible that China would attempt to manipulate the market not lengthy after copper hit a report excessive. China desires to pay decrease costs for its copper and has created a man-made surplus by filling up its Shanghai warehouses and exporting refined copper to LME warehouses. The tactic labored. Spot copper is down 14.7% since its Might 20 pinnacle.

On the demand aspect, together with the same old functions in building wiring and plumbing, transportation, energy transmission and communications, there may be now added demand for copper in electrical automobiles and renewable vitality techniques.

Tens of millions of ft of copper wiring will probably be required for strengthening the world’s energy grids, and a whole bunch of hundreds of tonnes extra are wanted to construct wind and photo voltaic farms. Electrical automobiles use triple the quantity of copper as gasoline-powered automobiles. There may be greater than 180 kg of copper within the common house.

Further copper is being demanded by the electrification of public transportation techniques, 5G and AI.

In line with Nikkei Asia, costs are being buoyed by the necessity for extra knowledge facilities to help the event of synthetic intelligence, all of which would require copper.

The newest copper demand driver comes from the Ukraine, the place the battle with Russia is consuming tonnes of bullet cartridge casing manufactured from brass, an alloy of copper and zinc.

The European Protection Company says a NATO 155-mm artillery shell accommodates half a kilogram of copper, with Ukrainian forces firing as much as 7,000 per day.

Citigroup is bullish on copper going ahead, with the financial institution’s analysts predicting that costs may surpass $10,000 a tonne ($4.53/lb) this 12 months as a consequence of coverage help in China. (the motivation worth to construct new mines is $11,000/t)

Mining.com reviews Beijing is predicted to introduce additional stimulus to improve its renewable vitality infrastructure on the Third Plenum assembly in mid-July:

These extra measures, particularly concentrating on home property and grid investments, are anticipated to help copper costs within the close to time period, Citi analysts mentioned in a be aware.

Investing within the pattern

Traditionally, junior useful resource shares provide the perfect leverage to a rising commodity worth due to the large alternative for positive aspects.

Probably the most upside comes from a junior within the exploration stage after they make an preliminary discovery. Nice drill assay outcomes can ship a junior’s share worth skyrocketing. The reverse can be true. Junior explorers working “greenfield” properties (no mining has ever taken place) are the riskiest performs. Strike out on assay outcomes and it might be goodbye to a share worth rise for a very long time – till the corporate finds one other venture.

Subsequent is the post-discovery useful resource definition stage. These corporations have already discovered one thing, the share worth has settled again after the preliminary discovery, and the junior is drilling and sure doing different exploration work, like sampling and surveying, to attempt to show up a maiden useful resource.

The third firm stage is the asset/ growth stage. Right here the advanced-stage junior has already managed to place collectively a useful resource, which might be measured and indicated (extra certainty, much less danger) or inferred (much less certainty, extra danger). They consider the deposit is giant and wealthy sufficient to start out down a growth path. An asset/growth stage firm is, within the opinion of administration, and sure stockholders who’re following the story, prone to grow to be a mine.

When assembling a portfolio of junior useful resource shares, it’s all the time a good suggestion to have a number of shares in every of the three firm phases. A pure exploration play could typically really feel like chasing a rainbow however the potential for making 5, 10, even 20 occasions your cash by buying a penny inventory that goes ballistic on a discovery gap is cause sufficient for us to danger a part of our funding capital.

I all the time goal to have a number of post-discovery useful resource definition stage juniors in my portfolio, too. The chance has been tremendously lowered, the wait time for a discovery non-existent, and the reward may be very good, contemplating the a lot decrease quantity of danger, in comparison with an exploration-stage junior.

At AOTH, we don’t usually put money into main or mid-tier mining corporations as a result of smaller corporations provide far higher upside, however traders could want to embrace a number of producers of their portfolio. You need to select a miner that provides you direct publicity to the commodity you’re all in favour of.

A very good instance is Freeport McMoRan (NYSE:FCX). Headquartered in Phoenix, Arizona, Freeport operates giant, enduring, geographically numerous property with important confirmed and possible reserves, and primarily explores for copper, gold, molybdenum, silver and cobalt.

The corporate is the world’s largest publicly traded copper producer and the fifth largest miner by market cap.

FCX’s portfolio of property contains the Morenci mine in Arizona, Cerro Verde in Peru, El Abra in Chile, and the large Grasberg mine in Indonesia. For extra particulars click on on the Operations tab on Freeport’s web site.

The inventory is up 22% 12 months up to now.

For direct copper publicity I additionally like Hudbay Minerals (TSX:HBM). Hudbay lately acquired Copper Mountain Mining and 75% of its Copper Mountain mine in south-central British Columbia (the rest is owned by Mitsubishi Corp), making it the third-largest copper producer in Canada.

Hudbay can be lively in Manitoba’s Flin Flon Snow Lake Greenstone Belt. The corporate says its Lalor mine (gold, zinc, copper, silver) in Snow Lake is a significant low-cost gold producer that considerably benefited from the refurbishment of the New Britannia mill in 2021. Hudbay has been drill-testing the down-plunge gold and copper extensions of the Lalor deposit, within the first step-out drilling within the deeper zones at Lalor for the reason that preliminary discovery of the gold zones in 2009.

Hudbay owns the manufacturing Constancia copper mine in Peru, and is growing the Copper World Advanced in Arizona and the Mason venture in Nevada.

HBM has soared 73% YTD.

I put money into quite a lot of valuable steel juniors however for direct publicity to silver I like Hecla and Coeur, and for gold I like Agnico Eagle.

Hecla Mining (NYSE:HL) is the oldest silver firm on the New York Inventory Alternate and the most important US silver producer. It has been mining since 1891.

Hecla has 4 producing mines: Greens Creek in Alaska, Fortunate Friday in Idaho, Casa Berardi in Quebec, and Keno Hill within the Yukon.

The corporate can be exploring for silver in three international locations. Its US growth properties are San Juan Silver in Colorado, Silver Valley/Star in Idaho, Republic in Washington State, Rock Creek and Libby in Montana, and 5 tasks in Nevada.

In Canada, Hecla has the Kinskuch property in British Columbia, Heva-Hosco and Opinaca/Wildcat in Quebec, and Rackla within the Yukon.

Its Mexico focus is the San Sebastian silver-gold venture in Durango State.

Hecla is up 16% YTD, having reached a 52-week excessive of $6.23 on Might 20. It retraced to $4.77 on July 1 however is now buying and selling at $5.47.

Coeur Mining (NYSE:CDE) is a US-based valuable metals producer with 4 operations: the Palmarejo gold-silver advanced in Mexico, the Rochester silver-gold mine in Nevada, the Kensington gold mine in Alaska, and the Wharf gold mine in South Dakota. Additionally, the corporate owns the Silvertip polymetallic exploration venture in British Columbia.

Coeur’s inventory has doubled this 12 months, from $3.20 in the beginning of the 12 months to the present $6.40.

Agnico Eagle Mines (TSX:AEM) is a Canadian senior gold mining firm and the third largest gold miner on the earth, producing valuable metals from Canada, Australia, Finland and Mexico.

The corporate owns the 2 largest gold mines in Canada — Canadian Malartic and Detour Lake. Agnico plans to improve Detour Lake, positioned close to the Ontario-Quebec border, right into a million-ounce-per-year producer by digging for higher-grade ore beneath the present open pit, and following a gold system that tracks west.

The remainder of Agnico Eagle’s spectacular manufacturing portfolio includes the Fosterville mine in Australia, the Kittila mine in Finland, the Goldex and LaRonde complexes in Quebec, Macassa in Ontario, the Meadowbank Advanced and Meliadine mine in Nunavut, and the La India and Pinos Altos mines in Mexico.

AEM began the 12 months at $72.05 and now trades at $99.63, for a considerable achieve of 38%.

Two of my favourite copper juniors are Kodiak Copper and Max Useful resource. I additionally like Max for silver, because of the large sedimentary copper-silver property it’s growing in Colombia.

Silver North Sources is the opposite Forward of the Herd silver play. For gold I like EGR Sources and Storm Exploration.

Kodiak Copper’s (TSXV:KDK, OTCQB:KDKCF, Frankfurt:5DD1) MPD property is surrounded by a number of producing and past-producing mines. The producers are Copper Mountain to the south, Highland Valley within the north, and New Afton, near Kamloops, re-opened by New Gold in 2012.

The venture lies throughout the southern portion of the Quesnel Terrane, British Columbia’s principal copper-producing belt.

Historic drilling noticed 384 holes accomplished for the reason that Nineteen Sixties by earlier operators. A lot of the drills examined mineralization from floor, with holes not often testing under 200m depth.

Over the previous 4 years, Kodiak Copper has accomplished 123 drill holes or 74,804 meters.

The corporate tasted success throughout its maiden drill program in 2019 with the invention of the Gate Zone.

Kodiak Copper is present process a ten,000-meter drill program targeted on a number of drill-ready targets within the MPD North and South venture areas. The purpose is to find high-grade mineralization, increasing the near-surface mineralization round identified zones, and making new discoveries.

This 12 months’s discipline program is exclusive for Kodiak Copper in that synthetic intelligence (AI) is getting used to generate and ensure drill targets.

Six goal areas are slated for drilling: two at MPD North (Belcarra and Blue) and 4 at MPD South (1516, South, Adit and Celeste). The concentrating on technique includes the combination of targets developed by Kodiak’s exploration staff and VRIFY AI’s predictive modeling.

VRIFY has acknowledged 9 areas of curiosity, both adjoining to identified copper-porphyry zones (Gamma, Zeta, Epsilon, Lambda, Omega and Sigma), or as new precedence areas (Omicron, Iota and Tau) which benefit follow-up.

Kodiak Copper

TSXV:KDK

Cdn$0.49 2024.07.10

Shared Excellent 63.9m

Market cap Cdn$36.8m

KDK web site

Max Useful resource’s (TSXV:MAX; OTC:MXROF; Frankfurt:M1D2) Cesar copper-silver venture in Colombia is a gigantic, district-scale property on which Max has simply minimize an 80/20 earn in cope with Freeport McMoRan.

The Cesar venture is located alongside the copper-silver-rich Cesar Basin. This area supplies entry to main infrastructure ensuing from oil & fuel and mining operations, together with Cerrejon, the biggest coal mine in South America held by Glencore.

The Cesar venture land bundle now spans greater than 1,150 km of geology potential for sedimentary-hosted copper and silver deposits and contains 20 mining concessions protecting over 188 sq. km.

Max has made important progress at Cesar, its discipline groups have thus far recognized 28 high-priority targets throughout the three districts of the 120-km Cesar copper-silver belt: AM, Conejo and URU.

Underneath the earn-in settlement, introduced on Might 13, 2024, Arizona-based Freeport has an choice to amass as much as 80% of Cesar by spending CAD$50 million to discover the property, and making a sequence of money funds totaling CAD$1.55 million.

To earn an preliminary 51% curiosity, Freeport is required to fund $20 million of exploration expenditures at Cesar over 5 years and make staged money funds to Max totalling $0.8 million. Max stays the operator of Cesar throughout this preliminary stage.

As soon as Freeport earns its preliminary 51% curiosity, Freeport can enhance its curiosity to 80% by funding an additional $30 million in exploration expenditures at Cesar over 5 years and making staged money funds totalling $0.75 million.

Max’s shareholders can stay up for an preliminary $20 million dedication from FCX for what ought to quickly be the beginning of a really aggressive exploration/drill program.

Max Useful resource Corp.

TSXV:MAX; OTC:MXROF; Frankfurt:M1D2

Cdn$0.06 2024.07.10

Shares Excellent 176m

Market cap Cdn$10.5m

MAX web site

Silver North Sources (TSXV:SNAG) gives publicity to one in all Canada’s most prolific silver districts — Keno Hill.

Silver North’s underexplored Haldane venture demonstrates high-grade, high-width potential akin to the veins being mined at Keno Hill.

Between Haldane and its Tim carbonate substitute deposit (CRD), on the BC-Yukon border, Silver North gives sturdy discovery and growth potential towards the bullish backdrop for silver.

The Keno Hill Silver District was Canada’s second largest main silver producer and one of many richest silver-lead-zinc deposits ever mined.

Silver North’s Haldane property is 25 kilometers west of the principle Keno Hill deposits, and south of Victoria Gold’s Eagle mine, which poured its first gold in 2019. The 8,164-hectare land bundle hosts structurally managed silver veins containing galena, sphalerite, and tetrahedrite-tennantite in quartz-siderite gangue.

In 2021 Silver North introduced a new discovery on the West Fault Zone.

The purpose was to seek out Keno-type mineralization and at the very least 300 grams-per-tonne rock over a snug mining width of 4 meters. They achieved that with the West Fault discovery of 311 g/t Ag over 8.7m. This was adopted by 3.14m of 1,315 g/t silver.

In line with Silver North, this new zone has been traced over a 100- by 90-meter space with room to increase alongside strike and at depth.

Silver North Sources can be working with accomplice Coeur Mining to develop the Tim property, positioned on the Yukon aspect of the Yukon-British Columbia border.

The corporate earlier this month introduced that Coeur has began drilling at Tim. Present plans are to drill roughly 2,000 meters, concentrating on silver-lead-zinc Carbonate Substitute Deposit (CRD) mineralization much like that discovered at Coeur’s Silvertip property 19 km south of Tim.

TSXV:SNAG

Cdn$0.14 2024.07.10

Shares Excellent 43.3m

Market cap Cdn$6.81m

SNAG web site

EGR Exploration (TSXV:EGR) is working close to Detour Lake, Ontario, Canada’s second-largest gold operation, inside a area internet hosting a number of multi-million-ounce deposits.

Situated within the northern a part of the Abitibi Greenstone Belt, the Detour-Fenelon Gold Pattern spans over 200 km of potential strike size potential alongside the Sunday Lake and Decrease Detour deformation zones. EGR’s property is positioned 20 km west of the Detour Lake open-pit (therefore the title “Detour West”), and in addition instantly adjoins Agnico Eagle’s holdings alongside the pattern.

To maximise its likelihood of success, EGR since 2020 has elevated its landholding and consolidated your complete 40,255-hectare Detour West venture space, which is now 35 km lengthy by 15 km extensive.

What makes EGR’s floor so intriguing? In line with revered geologist Quinton Hennigh, it’s when deformation belts just like the Sunday Lake Deformation Zone grow to be constricted, or “squeezed”.

A key activity for EGR, because it goes about exploring Detour West, is testing the extension of the SLDZ, attempting to show that Detour West is on pattern with Agnico-Eagle’s Detour Lake mine and its 20.7Moz of reserves.

This summer time’s drill program envisions at the very least 35 reverse-circulation (RC) holes, that may goal the place the gold constructions cross onto Detour West, together with the “squeezed” deformation zone talked about by Hennigh.

The drills will puncture a mean 40 meters of glacial until earlier than coming into the bedrock. “It’s poking a number of shallow holes to seek out the gold dispersal prepare after which testing the bedrock to get a pattern of what rocks we’re entering into,” CEO Daniel Rodriguez mentioned.

If EGR can present sufficient gold-in-till from the fenced RC holes it will probably vector into the supply of the mineralization.

EGR Exploration Ltd.

TSXV:EGR

Cdn$0.05, 2024.07.10

Shares Excellent 40.2m

Market cap Cdn$2.2m

EGR web site

Storm Exploration (TSXV:STRM) got here to my consideration for the exploration settlement it lately signed with the Eabametoong First Nation relating to Miminiska, Keezhik and Attwood, which sit on their conventional territory.

It’s uncommon for a mining firm to prioritize First Nations session over different actions, and I feel this speaks to the progressive mindset of CEO Bruce Counts and his administration staff. Lately, nothing occurs on a mineral exploration property sitting on First Nations land with out the nation’s consent.

Storm’s 4 properties are all are within the neighborhood of historic Ontario gold camps, which mixed have produced over 200 million ounces. The Fort Hope space is a greenstone belt with the potential to host a serious gold camp.

Excessive-grade gold has been confirmed by drilling at a lot of places on the Miminiska property. Historic assays embrace 5.75g/t Au over 20.84m and 13.95 g/t Au over 5.32m, with mineralization hosted in banded iron formation and related shear zones.

The Miminiska venture bears all of the hallmarks of a banded iron formation, which account for round 60% of worldwide iron reserves, The closest analog is Musselwhite, positioned ~115 km to the northwest. The deposit additionally has the same geometry to the Lupin BIF mine, which produced 3.4Moz at 9.1 g/t Au earlier than closure in 2005.

Storm plans to lift cash for a drill program at Miminiska.

Ideally, between 2,000 and a pair of,500 meters can be drilled from six to 10 drill pads. It needs to be famous that the claims at Miminiska are patented claims, that means that no drill permits are required. Regular drilling tips should nonetheless be adopted and Storm wants the help of native first nations, which it already has.

Storm Exploration Inc.

TSXV:STRM

Cdn$0.04 2024.07.10

Shared Excellent 41.6m

Market cap Cdn$2.0m

STRM web site

Richard owns shares of Max Useful resource (TSX.V:MAX).

STRM, KDK, SNAG, EGR and MAXare paid advertisers on his website aheadoftheherd.com

This text is issued on behalf of STRM, KDK, SNAG, EGR and MAX.

Authorized Discover / Disclaimer

Forward of the Herd publication, aheadoftheherd.com, hereafter generally known as AOTH.

Please learn your complete Disclaimer fastidiously earlier than you utilize this web site or learn the publication. If you don’t conform to all of the AOTH/Richard Mills Disclaimer, don’t entry/learn this web site/publication/article, or any of its pages. By studying/utilizing this AOTH/Richard Mills web site/publication/article, and whether or not you truly learn this Disclaimer, you might be deemed to have accepted it.

Any AOTH/Richard Mills doc will not be, and shouldn’t be, construed as a proposal to promote or the solicitation of a proposal to buy or subscribe for any funding.

AOTH/Richard Mills has based mostly this doc on info obtained from sources he believes to be dependable, however which has not been independently verified.

AOTH/Richard Mills makes no assure, illustration or guarantee and accepts no duty or legal responsibility as to its accuracy or completeness.

Expressions of opinion are these of AOTH/Richard Mills solely and are topic to alter with out discover.

AOTH/Richard Mills assumes no guarantee, legal responsibility or assure for the present relevance, correctness or completeness of any info supplied inside this Report and won’t be held responsible for the consequence of reliance upon any opinion or assertion contained herein or any omission.

Moreover, AOTH/Richard Mills assumes no legal responsibility for any direct or oblique loss or injury for misplaced revenue, which you’ll incur because of the use and existence of the data supplied inside this AOTH/Richard Mills Report.

You agree that by studying AOTH/Richard Mills articles, you might be appearing at your OWN RISK. In no occasion ought to AOTH/Richard Mills responsible for any direct or oblique buying and selling losses brought on by any info contained in AOTH/Richard Mills articles. Info in AOTH/Richard Mills articles will not be a proposal to promote or a solicitation of a proposal to purchase any safety. AOTH/Richard Mills will not be suggesting the transacting of any monetary devices.

Our publications are usually not a advice to purchase or promote a safety – no info posted on this website is to be thought of funding recommendation or a advice to do something involving finance or cash apart from performing your individual due diligence and consulting together with your private registered dealer/monetary advisor.

AOTH/Richard Mills recommends that earlier than investing in any securities, you seek the advice of with knowledgeable monetary planner or advisor, and that it is best to conduct an entire and unbiased investigation earlier than investing in any safety after prudent consideration of all pertinent dangers. Forward of the Herd will not be a registered dealer, seller, analyst, or advisor. We maintain no funding licenses and will not promote, provide to promote, or provide to purchase any safety.