“Globally, there can be few corporations conducting drilling campaigns of this scale, to this depth,” mentioned Michael Fonti, BHP’s major exploration geologist on the web site, stating a diagram of the cone-shaped deposit.

Fonti has spent greater than 20 years on websites very like this one, working most lately on the miner’s close by Olympic Dam, an unlimited, difficult copper and uranium operation. However even for BHP — a $140 billion firm which generated virtually $12 billion in free money move within the final monetary 12 months — giant, greenfield initiatives are scarce, and turning into extra so. Offers, not discoveries, are grabbing the headlines.

Copper’s bull narrative, which helped costs hit an all-time excessive in Could, is nicely understood. Electrification, wealthier populations and an increasing, energy-hungry expertise sector are huge new sources of demand. An electrical car requires roughly thrice the copper that goes into a traditional automobile, and the power transition received’t occur with out sufficient pink metallic for grids, batteries and chips.

This could all be prompting a surge in prospecting and digging, to make sure provide retains up, particularly as giant, established mines age. It isn’t — and that dangers making this much-needed metallic punitively costly.

Miners have been in spending purgatory for over a decade, atoning for the excesses of the final increase. For years, traders demanded beneficiant returns, not manufacturing development and positively not danger. However now that diggers can open the purse strings once more, excessive prices, sluggish permits and different hurdles are pushing the most important metallic producers to purchase — not construct.

Requested at its earnings briefing final month, Henry mentioned the corporate was opportunistic about offers and never pursuing them on the expense of exploration, nor was BHP making a blanket resolution on value. There was no rule of thumb on shopping for or constructing, he mentioned.

Nonetheless, in lower than two years, BHP has purchased copper and gold producer OZ Minerals for $6.4 billion, betting on South Australia’s copper province; tried and failed to purchase peer Anglo American Plc for $49 billion, largely for its South American copper mines; then in July agreed to purchase copper miner Filo Corp. collectively with Lundin Mining Corp, a guess on a venture in growth on the Argentina/Chile border.

“Mining is cyclical, and a key issue driving the pattern of shopping for over constructing is the purpose within the cycle,” mentioned Campbell Cooper, a Melbourne-based advisor at Greenhill & Co., an funding financial institution. “Latest years have additionally seen an acceleration in the price of constructing new mine capability. Arguably that value will not be totally mirrored in fairness valuations, making shopping for extra engaging.”

Constructing from zero, in brief, is each worryingly dangerous and unappealingly expensive.

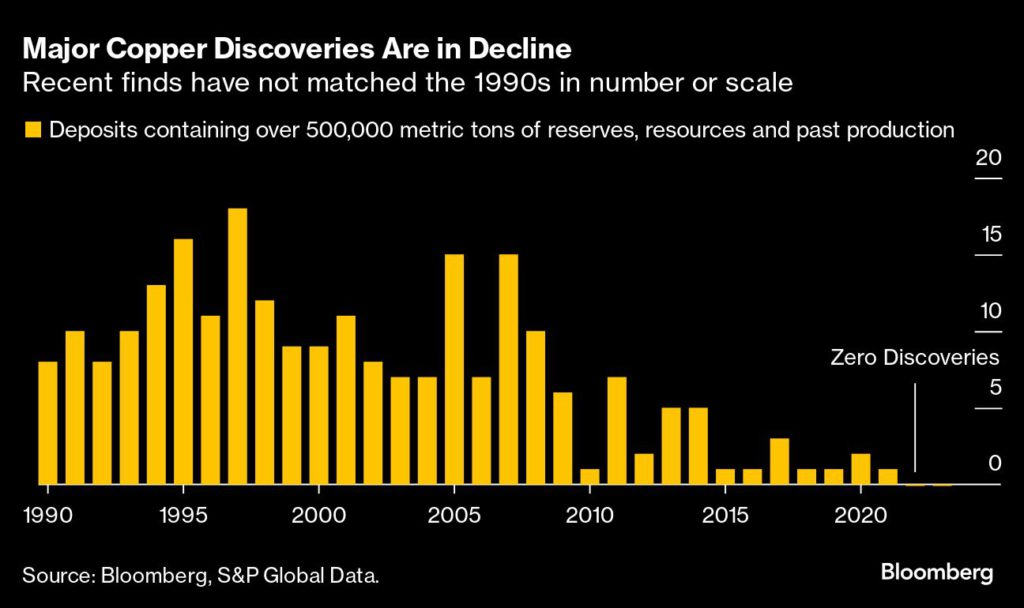

No marvel, then, that solely roughly 1 / 4 of the sector’s sanctioned — or permitted — initiatives between 2019 and 2023 have been of the greenfield selection, in keeping with analysts at Jefferies LLC. That’s down from greater than half within the 2009 to 2013 interval. The scale of latest initiatives can be shrinking.

“There was a raft of copper discoveries within the Fifties, 60s, 70s, and 80s,” mentioned BHP’s Fonti. “Every thing being produced now’s from that period of discoveries.” Escondida, the world’s largest copper mine, dates again to the late Seventies and early Eighties.

In fact, BHP has invested in growth — it permitted almost $5 billion for its potash operation final 12 months — however its exploration funds stays modest, even for copper. Whereas it has almost tripled its annual greenfield spending from the beginning of the last decade to $124 million within the 12 months to June, that compares to $324 million spent on greenfield exploration alone again in its 2012 monetary 12 months.

Friends observe related patterns. Rio Tinto Group, which has not achieved large-scale offers of late, spent $300 million on greenfield exploration in 2023. Anglo American Plc and Freeport-McMoRan Inc have spent much less. Glencore Plc doesn’t element exploration spending, however its focus has been on current deposits in its portfolio.

“Finally the business wants continuous funding in exploration and new discoveries. M&A is necessary to place property into the palms of the optimum homeowners, however won’t materially improve general business provide,” mentioned Sam Brodovcky, head of metals and mining M&A at Customary Chartered Plc. “And for key commodities resembling copper, we have to improve provide not solely to replenish depleting mines but in addition to maintain up with rising demand because the world industrializes and transitions to scrub power.”

Henry says giant gamers like BHP are nicely positioned in terms of including provide. As greenfield dangers improve, the business’s behemoths can unlock extra metallic with the enlargement of current initiatives, because of giant steadiness sheets and technical functionality.

They’re additionally betting on much less dangerous exploration by supporting junior miners — as with BHP’s Xplor program, which gives modest funding with the potential for way more if prospecting is profitable.

What’s much less clear is whether or not this can be sufficient to offer the metallic the world wants.

Juniors, decrease down the mining meals chain, have lengthy taken on a lot of the sector’s exploration danger. However that proportion is now rising simply as funding in smaller outfits falls.

“We’ve acquired to some extent the place we’re fairly reliant on juniors to discover. It’s very troublesome seeing that persevering with in the event that they’re not getting the fairness that they want,” mentioned Sandra Occhipinti, a geologist and researcher at Australia’s nationwide science company, Commonwealth Scientific and Industrial Analysis Organisation.

Richard Schodde, a veteran geologist and skilled on South Australia’s copper belt, places the variety of discoveries made annually at solely a handful. He describes BHP’s fortunate strike at Oak Dam in 2018 “was most likely essentially the most spectacular” of latest years.

Worth is clearly one purpose holding again the splurge that might change that. Copper has loved a bull run on fears of provide disruption and hopes of hovering inexperienced demand. Costs topped US$11,000 a ton earlier this 12 months. However the world financial system is faltering and copper wants to succeed in $12,000 a ton — a near-30% bounce on present costs — to incentivize large-scale investments in new mines, in keeping with Olivia Markham, who co-manages the BlackRock World Mining Fund.

Copper’s enchancment for the reason that value trough of 2020 has not been sufficient. Prices are rising too quick as exploration groups want go deeper, into extra technically difficult deposits or into much less fascinating areas.

Take Oak Dam, the place the underside of the deposit is a few 4 kilometers underground — depths the place warmth from the earth’s core begins to develop into an issue. And even Olympic Dam’s subsequent part of exploration, Olympic Dam Deeps. BHP’s lately acquired Filo asset in South America, in the meantime, sits some 5,000 meters above sea degree, the place the air is so skinny helicopters battle to hover.

“As soon as upon a time you may simply kick rocks. It’s not for the faint-hearted — and just one exploration marketing campaign out of a thousand leads to a discovery,” says Karol Czarnota, a director at Geoscience Australia, a authorities company set as much as encourage mining. Oak Dam was discovered utilizing a few of its knowledge.

One space of fine information is expertise. New devices and higher geological data are permitting even the reassessment of current repositories of knowledge. Core libraries round Australia, for instance, maintain over 100 million meters of rocks from drilling campaigns of previous booms, free for geologists searching for mineralization missed by others.

However even at Oak Dam, a deposit that was virtually missed till new geophysics strategies may unlock it, that cheer is tempered. The sluggish tempo of mine growth means a closing funding resolution won’t come till 2027 on the earliest. Copper manufacturing will nonetheless be years away.

(By Paul-Alain Hunt)