On quite a few events, I emphasised that gold is most probably to maneuver within the reverse to actual yields, not nominal ones, however the dialogue retains returning. Let’s dig deeper.

After all, there might be instances when gold strikes within the reverse solution to nominal yields (e.g. the 2-year yields), however the important thing factor is that it’s only the hyperlink between actual yields and gold that’s dependable with out additional consideration.

- Nominal Yield = Actual Yield + Projected Inflation

In different phrases:

- Actual Yield = Nominal Yield – Projected Inflation

Why? Think about that the nominal yield is rising steadily, however the inflation is rallying sharply and is predicted to take action. On this case, the actual yield can be declining.

What would gold be prone to do on this surroundings? It will rally as a result of the inflation-hedge impact can be stronger than the elevated “different value” of holding gold that gives no curiosity (no yield – besides when the steel is leased).

Within the reverse scenario, nominal yields could possibly be declining, but when inflation is falling sooner, then actual yields may really be rising, which means that gold worth can be prone to decline.

There are another components that should be thought of, just like the USD Index, however my level right here is: it’s the actual yield that has a transparent impression on gold. In case of nominal yields, the impression would possibly (or won’t!) be as clear.

Which means it’s crucial to look what’s actually occurring with the bond yields AND how gold used to carry out in related conditions earlier than stating that this or that’s the seemingly implication.

Some authorities would possibly inform you that bond yields and gold have to maneuver in reverse instructions. I’m suggesting that you just query these authorities. The truth is, that’s what I’m going to do under.

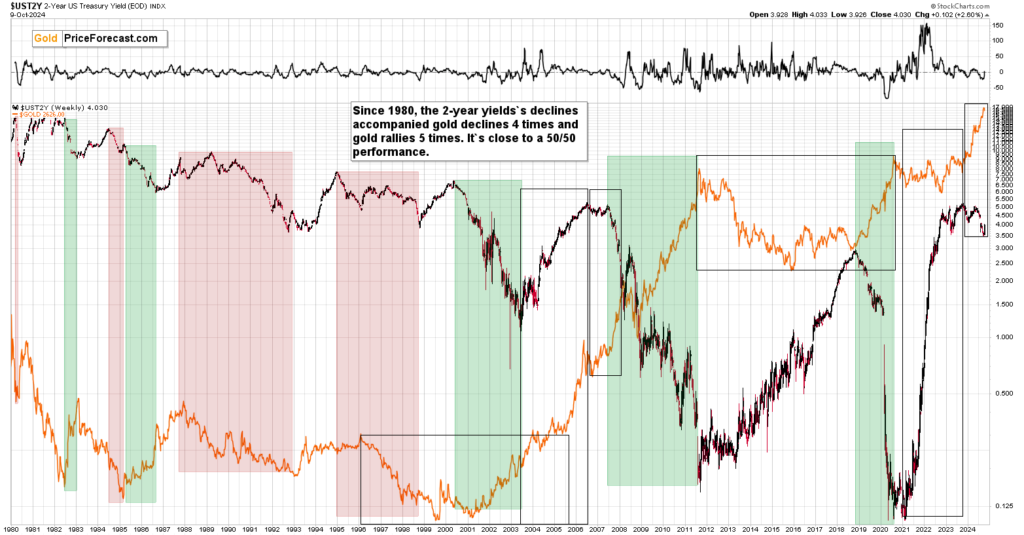

I ready three charts for you that includes the 2-year bond yield which might be prone to shed additional gentle on the hyperlink that to many appears clearer than it ought to.

Let’s begin with the essential “zoom-out” method.

What you would possibly examine gold and the yields is that it strikes within the reverse instructions, and often the interval between 2000 and now’s introduced on the chart. It does certainly cowl three intervals when the yields fell and gold rallied on the identical time.

The flaw on this evaluation is that it assumes that gold hasn’t fashioned a significant high proper now. If it did, then the hyperlink to the interval between 1980 and 2001 turns into extra essential, and again then most intervals when the yields declined had been characterised by declining gold costs.

If we take each intervals into consideration (so, by discarding the belief that gold both topped or that it didn’t high), we get to the conclusion that indications from bond yields’ declines are somewhat unclear.

This would possibly (ought to) elevate a number of eyebrows. Let’s make it extra fascinating by including an additional layer on high of the above evaluation.

I marked two very distinct intervals – ones when gold fashioned multi-year cup-and-handle patterns. That was across the 2000 and across the 2015 bottoms.

Within the second half of the sample, we noticed a rally in each: gold and bond yields (marked with the second rectangle). The rallies began from (roughly) an area low in gold and when bond yields topped, so did gold.

The actually fascinating factor is what occurred within the areas marked with the third triangle. That’s when the value of gold soared whereas bond yields declined.

Within the earlier sample, this continued till we noticed a transfer again up within the yields. That, my buddies, was the 2008 high that preceded profound declines in gold, shares, and – most significantly – mining shares.

What we see now’s that bond yields are after a decline, they usually simply moved again up as gold topped.

Given the above-described analogy, the current high was seemingly a very main high – one which marks the top of a medium-term upswing, and a transparent signal that traders ought to put together (or already be ready) for a wild experience to lower cost ranges – particularly in mining shares.

After all, this isn’t a sign that’s prone to work when it comes to days – it’s prone to have a important impression when it comes to months (and maybe weeks). And it doesn’t invalidate among the long-term alternatives within the valuable metals market.

So, sure, trying on the strikes in 2-year bond yields and the way it impacted gold previously doesn’t need to look so bullish as most individuals painting it. There’s a bearish signal right here as properly – a fairly profound one.

However wait, there’s extra!

Bearish indicators forward

Value strikes and worth patterns are each essential, however all of us learn the phrase that point is extra essential than worth, proper? When the time is correct, the value will reverse – was the continuation of this quote.

With the above in thoughts, let’s flip again to the interval that’s often seen as bullish for gold.

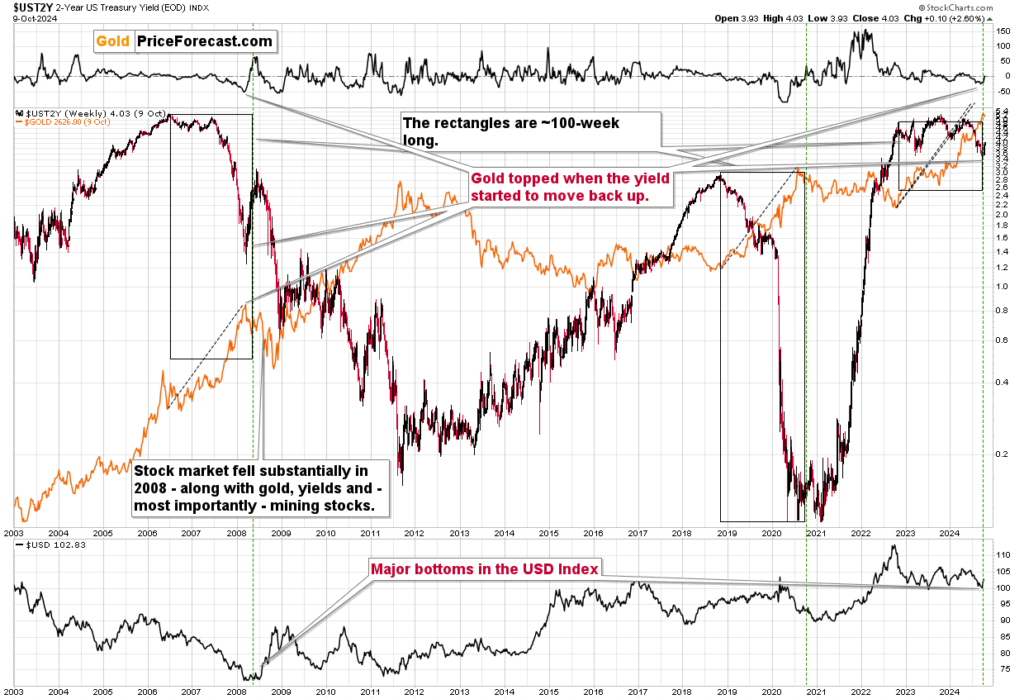

This time let’s contemplate when the rallies actually ended.

The 2008 high was when the rally ended, although yields then traded sideways for a very long time earlier than declining. Whereas they had been buying and selling sideways, gold was shifting increased.

The 2018 high was adopted by a right away decline and gold rallied.

Now, the important thing factor: when did gold high after these rallies?

In each instances, gold topped roughly 100 weeks after the rally in bond yields ended. That’s how huge the black rectangles are.

Guess what – lately, bond yields stopped rallying in 2022 and we’re about 100 weeks after that second. Oops…

Additionally, please be aware that in each most related instances (based mostly on each above charts): in 2008 and now, we noticed a significant backside within the USD Index that fashioned after a big (taking about 2 years) decline. Given final week’s highly effective rally within the USD Index, these conditions appear alike additionally from this angle.

The declines are coming – particularly in junior mining shares. Miners declined profoundly in 2008, and juniors are prone to decline greater than senior miners if the inventory market declines (which is prone to occur). Whereas this might sound unbelievable now (trace: it often appears unbelievable earlier than a very massive transfer takes place), in my view, this decline in junior miners is prone to create many small fortunes for these which might be positioned appropriately.

After all, that’s simply my opinion, however – as you see above – research-backed one.

(By Przemysław Radomski)