In idea, the financial relationship between Australia and China is a complementary one. Mining is structurally vital to the Australian economic system, at present accounting for nearly 14% of gross home product (GDP), up from 4% in 2004.

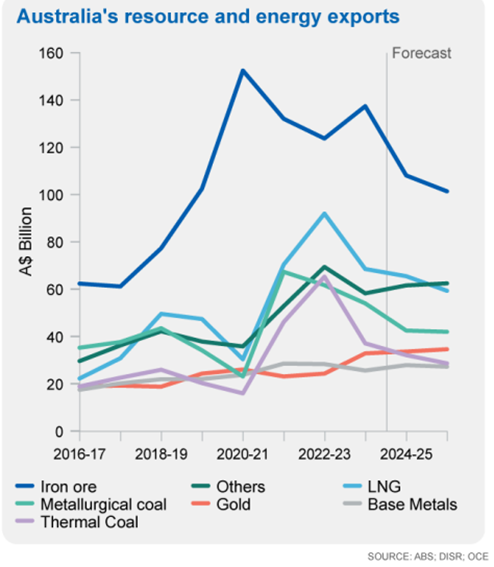

Australia exported A$673.28bn ($456.88bn) price of products and providers in 2023, with iron ore and coal exports taking over the highest two spots, accounting for 20.2% and 15.2% of the whole, respectively.

Whereas mining has expanded, manufacturing has declined, making up simply 6% of GDP, down from 12% in 1992. In distinction, China’s manufacturing ascendancy continues to furnish demand for Australian commodities, proving an important buyer for the mining business.

As many western economies struggled to compete with low cost Chinese language producers over the previous 20 years, the meteoric rise of Beijing was a boon for Australia’s commodity export financial mannequin. In 2023, China was Australia’s largest buying and selling associate, shopping for 32.5% of all Australian exports – however the relationship has not at all times been rosy.

Three years of Chinese language financial coercion

In 2020, political variations between China and Australia started to hamper the financial interrelation. Scott Morrison’s authorities known as for an inquiry into the origins of Covid-19, laying tacit blame on China for the outbreak, and the Turnbull Authorities’s ban of Huawei’s 5G community turned an more and more “thorny difficulty”. In response Beijing accused Australia of aligning with the US in pursuit of a hostile international coverage and meddling in Chinese language inside affairs, and subsequently stopped the import of all Australian items. China’s imports of Australian coal fell to nearly nothing, having imported A$13.7bn (66.29bn yuan) of the stuff in 2019.

The financial coercion was designed to interrupt Australia right into a place of ideological acquiescence with Beijing. The Chinese language Communist Get together (CCP) didn’t like how its quarry was starting to query its politics. Nevertheless, the tactic was not efficient.

Entry probably the most complete Firm Profiles

available on the market, powered by GlobalData. Save hours of analysis. Achieve aggressive edge.

Firm Profile – free

pattern

Your obtain e-mail will arrive shortly

We’re assured concerning the

distinctive

high quality of our Firm Profiles. Nevertheless, we would like you to take advantage of

helpful

resolution for your online business, so we provide a free pattern you could obtain by

submitting the beneath kind

By GlobalData

Beijing underestimated its reliance on Australian iron ore, which was wanted for steel-making, and imports mainly continued on the identical degree.

Whereas China imported much less coal, India and Japan doubled their consumption, proving to be dependable various prospects. The inferior home coal China used as a substitute was additionally unreliable, resulting in coal-fired energy ‘brown-outs’.

As well as, Australia held a powerful geopolitical bargaining place. China wished to hitch a probably profitable free commerce settlement, the Complete and Progressive Settlement for Trans-Pacific Partnership, however as a member, Australia might block China’s accession. Evidently, Canberra held extra world clout than the CCP first assumed.

Return to commerce

The plan for financial coercion failed, and for some commodities, Chinese language imports from Australia are actually as excessive as they’ve ever been. Pushed by the inferiority of its personal coal, China started importing Australian coal once more in January 2023.

In 2024, Chinese language coal imports from Australia might attain a report excessive, based on Andrew Gorringe, researcher on the Institute for Power Economics and Monetary Evaluation (IEEFA). Nevertheless, it is very important notice that solely the thermal coal commerce has rebounded and surpassed historic ranges, whereas the metallurgical coal commerce has declined.

Lithium is one other market through which China and Australia have complementary capabilities. Australia was the world’s largest lithium producer in 2023, accounting for 45% of the worldwide complete, however lacks the flexibility to refine and course of.

China, however, is the world’s chief in lithium refining and processing, with round a 57% monopoly. Between January and June 2023, Australia’s gross sales of lithium to China reached a mixed worth of $11.7bn. As with the iron ore commerce, the Australia-China lithium commerce wants match collectively like a key in a lock.

The commerce solely lives twice?

Though commerce appears pretty much as good as ever, there are causes to counsel this may occasionally not proceed.

The coal and lithium export enterprise mannequin might have an expiry date decided by exterior forces. China is seeking to restrict its demand for coal, with Xi Jinping pledging that coal use will peak by 2026. Concerning thermal coal, Gorringe factors out that Beijing drastically lowered approvals for brand new vegetation within the first half of 2024 (H1 2024), with simply 9.1GW of coal-fired capability given the go-ahead, 83% lower than in H1 2023.

“This may add to the present momentum whereby grid-connected wind and photo voltaic capability exceeded that of coal for the primary time in June 2024,” he says.

On the metallurgical coal entrance, China didn’t approve building of any coal-based metal vegetation in H1 2024. As a substitute, it permitted 7.1 million tonnes (mt) of latest, cleaner scrap-based metal manufacturing capability utilizing electrical arc furnaces, based on Reuters.

Whereas China is seeking to cut back total demand for coal, it additionally needs to supply extra provide domestically. In response to International Power Monitor (GEM), China has greater than 1.2 billion tonnes of coal mine capability within the pipeline, greater than the remainder of the world mixed. Round a 3rd of those mines are underneath building and can quickly be operational. Most are mega-mines with lifespans of not less than 5 a long time.

“In the long run, the declining demand for coal and lowered reliance on imports will place Australia’s already declining market share underneath extra stress,” Gorringe says.

Owing to such pressures, the Australian Authorities says that regardless of the coal commerce with China resuming, Chinese language imports are in structural decline, and that the nation’s home coal provide might match home coal consumption by the 2030s.

Taking cost of Australian lithium provide

At first look, the lithium commerce appears extra stable and structurally entrenched. Australia gives 60% of China’s lithium demand and Chinese language firms corresponding to Ganfeng Lithium have invested long-term capital within the business.

Nevertheless, the US is encouraging Australia to dilute this relationship. China has a stronghold on world lithium provide chains and Washington is eager to place a cease to this. It supplied Australia entry to its $369bn Inflation Discount Act clear vitality incentive if home firms have lower than 25% possession, voting rights or board seats held by “international entities of concern” corresponding to China.

Nevertheless, this isn’t simply Washington barking orders. Canberra recognises it might need to realign in favour of the US. Beneath the Essential Mineral Technique 2023–2030, the Australian Authorities goals to extend collaboration with “like-minded” companions such because the US, the UK, Japan and the EU.

Since 2021, A$1.5bn in financing has been supplied to “strategically vital tasks” that cut back reliance on China. The Australian Authorities has additionally agreed to help provide chains with the US, whereas blocking a number of Chinese language investments.

In apply, this resulted in Treasurer Jim Chalmers blocking two proposed Chinese language investments in Australia’s lithium sector over the previous two years.

Nevertheless, such aggressive decoupling does pose dangers for Australia. Premier of Western Australia Roger Prepare dinner mentioned final December: “It’s extra a matter of accepting the truth that it’s not whether or not they [the Chinese] will come however that they’re already right here. We’ve to know that China is our largest buyer and our largest provider of a number of the weather of a essential minerals and battery provide chain.”

Australia at present doesn’t have any of its personal lithium processing services, which take a very long time to assemble. As an illustration, a brand new native lithium hydroxide plant in Kwinana, Western Australia, took 5 to 6 years to start out operations. The Chinese language firm Tianqi Lithium invested A$700m into the operation in 2016, and different related tasks would require Chinese language capital.

What’s subsequent for China-Australia mining commerce?

Regardless of the thawing of Australia and China’s relationship and the return to affluent commerce, Canberra must be conscious that the present state might not final for so long as it hopes.

Demand for coal might quickly enter structural decline, with China aiming to make use of much less for energy technology and produce what it does use domestically.

The lithium relationship ought to be extra stable as China is closely invested in Australia’s business, however geopolitical manoeuvring on each side might nonetheless destabilise it.

If Australia has learnt something from the three years of financial coercion, it can know to not depend on one commerce associate too closely.