Juniors are extraordinarily vital to main mining corporations as a result of they’re the corporations discovering the deposits that can turn out to be the following mines. On this approach, juniors assist the majors to interchange the ore that they’re continually depleting of their working mines. Put one other approach, juniors discover the assets for majors to show into mineable reserves.

Financings/ capex drying up

One supply factors out that senior miners have been allocating a comparatively small portion of their revenues to exploration spending, with most expenditures invested in growing present mines and measures to cut back working prices.

If the seniors aren’t exploring, and when was the final time you heard of a significant mining firm making a greenfields discovery, it falls to the juniors. However junior mining financing has just about dried up; world exploration budgets in 2021 had been half of what they had been in 2012.

Capital expenditures in mining fell from roughly $260 billion in 2012 to $130 billion in 2020 (corresponding to fifteen% and eight% of business revenues, respectively), McKinsey & Firm discovered.

In response to Pure Assets Canada, in 2023 exploration spending by juniors declined to $2 billion, down 19% from $2.5 billion in 2022.

Nevertheless it will get worse, a lot worse.

In response to a latest evaluation by S&P International, gold discoveries all over the world have turn out to be extra scarce and smaller, dampening the outlook for future provide of the steel.

The report by way of Mining.com discovered there have solely been 5 main gold discoveries since 2020 including about 17 million ounces. A significant gold discovery was outlined as containing 2 million ounces in reserves, assets and previous manufacturing.

Nevertheless, S&P’s report famous that whereas the variety of discoveries and quantity of gold proceed to develop every year, many of the belongings had been found many years in the past….

It additionally identified that the common measurement of the latest gold discoveries has shrank, at about 3.5 million ounces in contrast with 5.5 million ounces throughout 2010-2019. Actually, not one of the discoveries remodeled the previous 10 years entered the listing of the 30 largest gold discoveries.

One of many graphs above comprises an vital assertion. It says “The variety of discoveries has been trending decrease regardless of increased budgets, as explorers are likely to deal with extending previous deposits as a substitute of discovering new ones.”

The S&P report says, “Along with analyzing previous discoveries, we have now examined prospects utilizing our knowledge on preliminary useful resource bulletins, which we observe month-to-month… we recognized 176 preliminary useful resource bulletins with a complete of 79Moz of contained gold.”

“Solely 78, or 44% of those bulletins are from greenfield belongings whereas the remainder are from newly found deposits inside present initiatives, demonstrating the business’s choice for exploring identified belongings.”

After which this:

“Whereas not all of those belongings will turn out to be main discoveries, the growing variety of bulletins in recent times brings a lot wanted optimism to an business that has skilled fewer and smaller discoveries. Since 2017 annual gold exploration budgets have greater than doubled, reaching a peak of $7 billion in 2022 after a low of $3.3 billion in 2016. Though budgets fell in 2023 attributable to tighter financing commissions, they continue to be elevated in comparison with earlier years. This development is prone to proceed so long as gold costs stay excessive.

“The upper exploration budgets since 2017 have contributed to extra and preliminary bigger useful resource bulletins. From 2017 to 2023, there was a mean of 42 bulletins with a mean of 24Moz of gold every year in comparison with a mean of 30 bulletins and 13Moz of gold when gold budgets had been declining.”

Let’s decipher what S&P International is de facto saying in its report, as a result of both knowingly or unintentionally, it fails to state the apparent: that there isn’t a cash for the juniors!

The report ballyhoos the truth that, regardless of there being an absence of recent discoveries previously decade, growing gold budgets “brings a tad of optimism for the way forward for gold provide, because the variety of preliminary useful resource bulletins continues to develop in measurement and quantity.”

Optimism for whom? Actually not junior useful resource corporations.

As for being optimistic on future gold provide, S&P analysis analyst Paul Manalo stated the information helps the agency’s long-held view that the business’s deal with older and identified deposits limits the possibilities of discovering enormous gold discoveries in early-stage prospects. No kidding.

“The dearth of high quality discoveries within the latest decade doesn’t bode effectively for the gold provide,” stated Manalo.

“Based mostly on the newest month-to-month Gold Commodity Briefing Service, we anticipate gold provide to peak in 2026 at 110 million ounces, pushed by elevated manufacturing Australia, Canada and the US — nations that additionally account for essentially the most found gold.”

He added that gold provide is predicted to fall to 103 million ounces in 2028, ensuing from a decline in provide from these nations.

Why would provide decline from these nations? In Canada and america, it may take as much as 20 years to construct a mine from discovery to manufacturing. Any new mines that began on the event path from 2008 onwards doubtless received’t add to the gold provide by 2028, as a result of they received’t but be operational. With few mines within the pipeline in these jurisdictions, mine manufacturing should come from present, more and more depleted mines.

As for peak gold, it’s already right here.

In a world of useful resource depletion, it falls to gold exploration corporations to fill the hole with new deposits that may ship the form of manufacturing required to satisfy gold demand, which is at present out-running provide.

The gold market continues to expertise tightness attributable to difficulties increasing present deposits, and a pronounced lack of enormous discoveries in recent times.

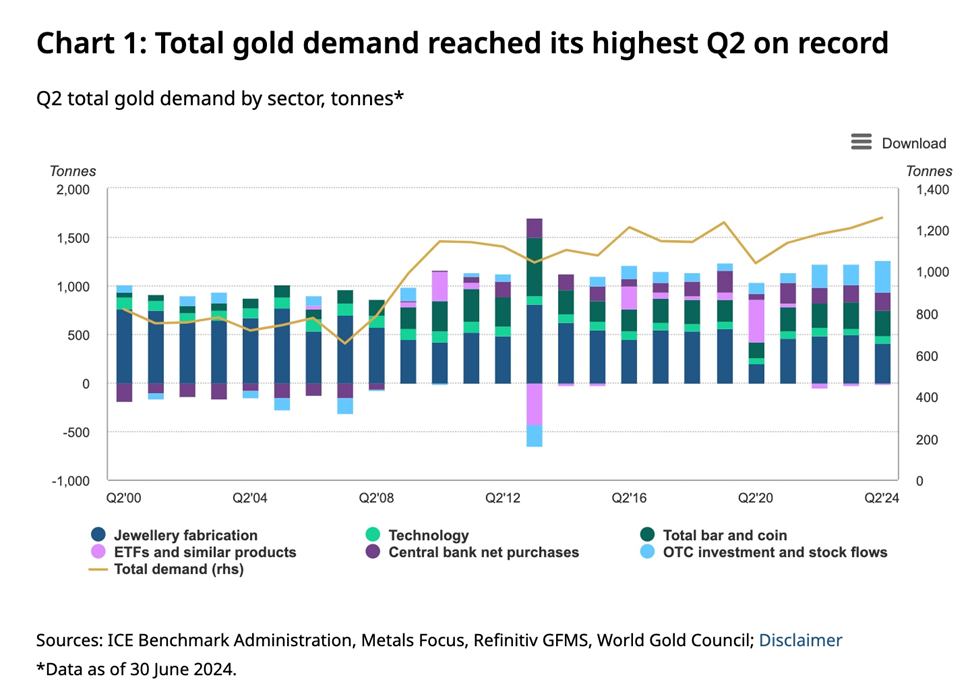

In 2023, 4,448 tonnes of gold demand minus 3,644t of gold mine manufacturing left a deficit of 804t. Solely by recycling 1,237t of gold jewellery may the demand be met. (The World Gold Council: ‘Gold Demand Tendencies Full 12 months 2023’)

That is our definition of peak gold. Will the gold mining business have the ability to produce, or uncover, sufficient gold, in order that it’s in a position to meet demand with out having to recycle jewellery? If the numbers mirror that, peak gold could be debunked. We’ve been monitoring it since 2019, and it hasn’t occurred but.

Within the second quarter of 2024, gold demand reached its highest second quarter on report, however provide nonetheless did not preserve tempo. Mine manufacturing of 929.1 tonnes fell in need of whole gold demand of 1,258.2 tonnes. Solely by recycling 335.4 tonnes may Q2 gold provide meet Q2 demand.

It isn’t solely gold initiatives that juniors are having bother getting financed, resulting in fears {that a} paucity of recent deposits will result in commodity shortages. We see this significantly with crucial minerals.

Kai Hoffman, the CEO of Soar Monetary, advised Kitco Mining in Might that regardless of increased valuable steel and copper costs, the generalist investor is lacking from useful resource shares and “there isn’t a euphoria.”

When it comes to financings, Hoffman stated the market is trending again to gold and silver, regardless of $180 million raised within the uranium area within the first three months. “Nevertheless it’s all later-stage initiatives,” Hoffman stated, affirming the conclusions reached by the S&P report.

An article earlier this 12 months from Investing Information Community tackled the issue of junior financing. The difficulty was a theme each on the Vancouver Useful resource Funding Convention in January, and the annual PDAC occasion in March in Toronto.

INN quoted Pierre Lassonde, co-founder and chair emeritus at Franco-Nevada (TSX:FNV) as saying that retail buyers have stayed away from the useful resource sector in favor of the fast cash and flashy profiles related to large tech corporations.

In response to Lassonde, the tech shares often known as the “Magnificent 7” collectively symbolize US$13.1 trillion in market cap, near the estimated US$15 trillion in gold that has been mined by historical past, and greater than 50 instances the US$250 billion mixed market cap of all gold equities, together with royalty corporations.

“(Of the US$250 billion), half of that’s six corporations, after which the opposite half, US$125 billion, is about 150 to 300 corporations — within the scheme of issues for buyers, they turn out to be irrelevant,” he stated.

Lassonde added that asset and fund managers are steering away from gold attributable to elements equivalent to disasters, capital prices and dangerous execution of mergers. He supplied the instance of Newmont (TSX:NGT), whose share worth reached practically US$90 in April 2022, however as of the tip of February had fallen as little as $30 following its merger with Newcrest. It at present trades for $53.11.

Jacqui Murray, companion with Useful resource Capital Funds, stated there’s been a generational shift amongst personal fairness funds, with youthful managers selecting to not spend money on mining for environmental and moral causes, particularly with the brand new buzzword, ESG.

In a piece entitled ‘Explorers and builders not noted to dry’, INN wrote:

Bringing new mines on-line is a protracted course of. It takes 10 to twenty years to maneuver an asset from discovery to manufacturing, and the overwhelming majority of discoveries don’t even make it to the manufacturing stage.

This makes funding on the exploration stage crucial for the business to make sure long-term viability and progress. Nevertheless, whereas exploration is vitally vital, it’s additionally essentially the most difficult and dangerous level for funding.

“I took a ten 12 months span from ’83 to ’93, and I checked out 3,000 exploration corporations and what occurred to them,” Lassonde stated. “Of these 3,000, solely 5 really delivered mines that opened and made cash. So the ratio is appalling, and it bought worse within the final 20 years as a result of there hasn’t been the form of discovery that we noticed within the ’80s and ’90s.”

These sorts of outcomes don’t instill confidence. For Lassonde, sifting by corporations is a part of his day-to-day life. However for normal buyers, doing due diligence on the huge array of obtainable shares could be daunting.

Lassonde additionally pointed to a different elementary shift inside the business, saying {that a} regular lack of senior corporations in Canada — together with Alcan, Falconbridge, Inco and Noranda — over the previous 20 years has had a appreciable affect on juniors. “These corporations not solely did analysis and improvement, however out of the C$100 million to C$200 million finances that they had for exploration, they shepherded most likely 50 to 100 corporations every on the junior degree, as a result of they understood that fifty % of all discoveries are made by juniors,” he defined.

Regardless of this top-down loss in funding capital and geological experience, the variety of junior corporations continues to be appreciable, and so they’re all competing with one another for what funding is accessible.

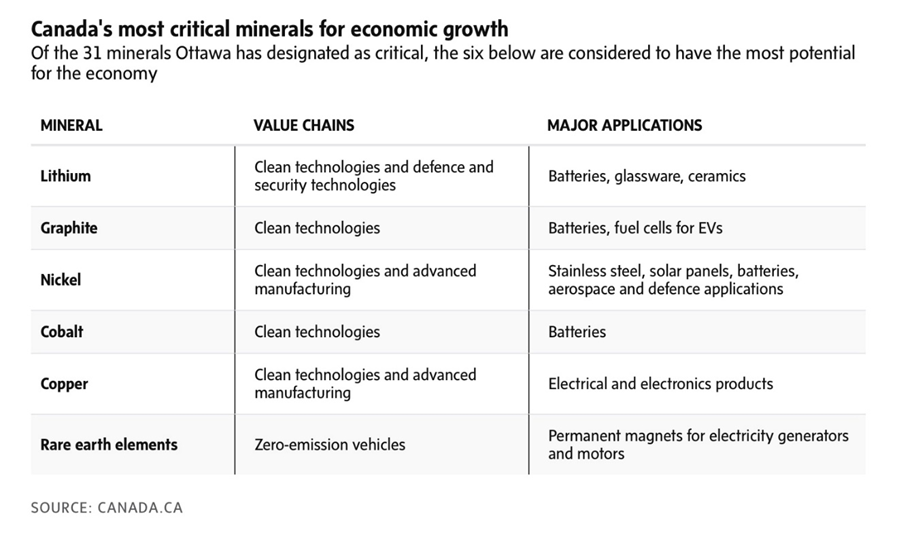

A Globe and Mail article revealed in November 2023 famous the disconnect between the crucial minerals wanted to drive the following part of the worldwide economic system, equivalent to graphite, nickel, copper and lithium, and the truth that many of the junior mining corporations which might be trying to find them are barely treading water, unable to finance the following phases of their exploration.

The business is totally totally different in comparison with 20 years in the past, when Canadian corporations with home initiatives had been the envy of the mining business. Vale’s $19-billion acquisition of Inco in 2006 helped seed a junior mining ecosystem centered in Vancouver and Toronto.

A lot of it has vanished – the bankers, the buyers and the keenness. In 2010, the mining sector made up 25 per cent of the whole worth of the Toronto Inventory Trade and the TSX Enterprise Trade, greater than another business. That 12 months, junior miners on the Enterprise Trade had been in a position to increase $5.3-billion to fund their exploration and improvement initiatives. As of October, that they had raised lower than half of that, and the sector’s composition of the whole TSX has fallen to 13 per cent.

Whereas financings for all sectors are sluggish this 12 months as a result of buyers are recalibrating after the COVID-19 pandemic tech bubble popped, mining has misplaced its lustre within the Canadian market. There are fewer funding banks offering analysis protection of up-and-coming mining corporations, and fewer funding advisers taking note of the sector. When a junior firm tries to boost cash, there simply aren’t as many individuals prepared to hearken to the gross sales pitch.

The wrestle to finance terrifies politicians and diplomats as a result of Canada and america are dropping the worldwide crucial minerals conflict. “Merely put, we don’t have sufficient of those minerals as we speak to satisfy the world’s – and our personal – rising demand,” David Cohen, the U.S. ambassador to Canada, stated in an October speech.

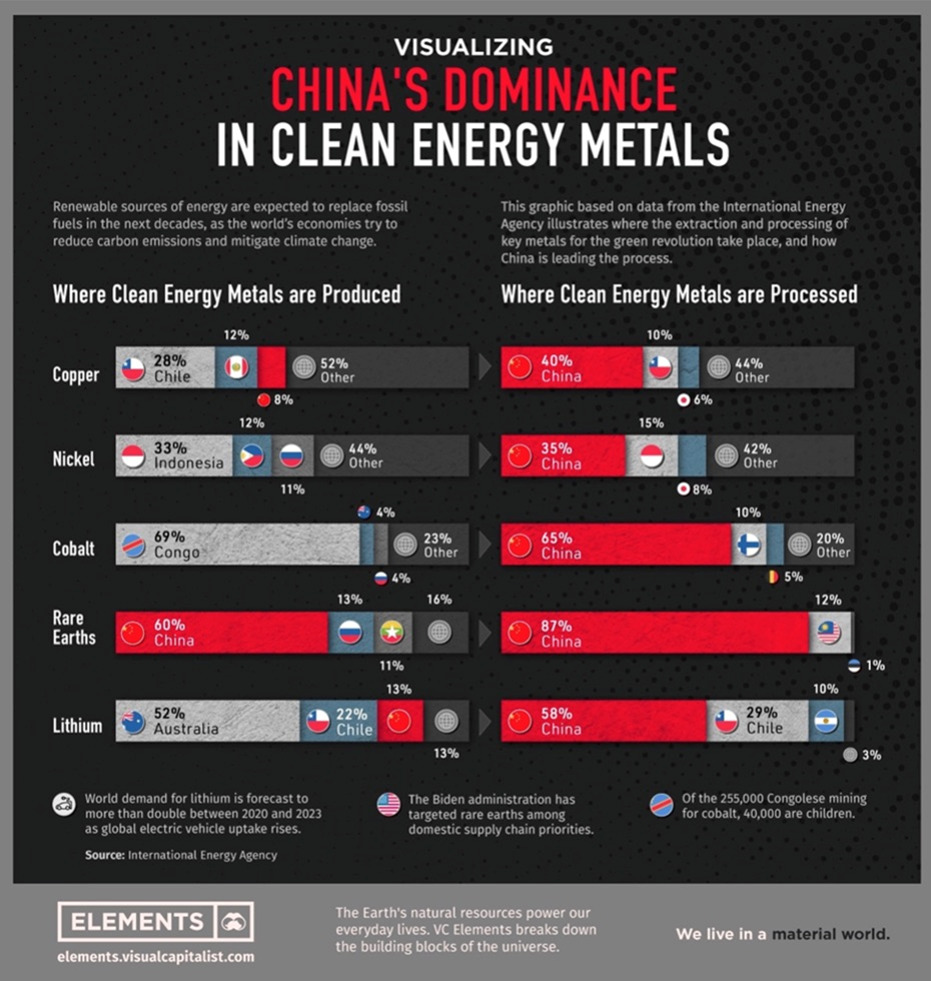

The fear is that China is hoovering up crucial minerals and can use them in opposition to the West in a geopolitical provocation, the identical approach Russia held its pure fuel provide over Europe’s head when it attacked Ukraine. At present, China refines greater than half of all nickel, lithium and cobalt worldwide.

China risk

The motive behind america commerce technique is well-documented — to shed itself of dependence on China whereas loosening the grip its predominant rival has on the worldwide provide chain of crucial minerals.

On the subject of uncooked supplies for the electrical car business, China is undisputedly essentially the most dominant pressure on the planet.

For instance, nearly each steel utilized in EV batteries as we speak doubtless comes from there, both mined or processed. Because of its technological prowess in refining, China has established itself because the across-the-board chief within the battery metals processing enterprise (see under).

In response to the Worldwide Power Company, the nation accounted for roughly 60% of the world’s lithium chemical provide in 2022, in addition to producing three-quarters of all lithium-ion batteries.

It additionally has a decent grip over the world’s provide of cobalt by its mining operations within the Democratic Republic of the Congo. Over the following two years, China’s share of cobalt manufacturing is predicted to succeed in half of world output, up from 44% at current, in line with UK-based cobalt dealer Darton Commodities.

IEA estimates that China’s share of refining is round 50-70% for lithium and cobalt, 35% for nickel, and 95% for manganese, regardless of being instantly concerned in solely a small fraction of the mine manufacturing.

The nation can also be chargeable for practically 90% of uncommon earth parts, that are important uncooked supplies for everlasting magnets utilized in wind generators and EV motors, in addition to 100% of graphite, the anode materials in EV batteries.

A report by Rice College’s Baker Institute for Public Coverage reveals that China now controls roughly 60% of the world’s manufacturing of those minerals that are thought of essential to the worldwide power transition.

For the US, this poses an awesome safety threat, as China may simply resolve to weaponize its market dominance, primarily locking America out of the crucial minerals provide chain.

Of the estimated 120 million tons of uncommon earth deposits worldwide, the majority of these at 44 million tons are present in China. The nation now accounts for 60% of uncommon earth mining, 85% of uncommon earth processing and 90% of high-strength uncommon earth everlasting magnet manufacturing.

China reducing off uncommon earths may show catastrophic for the US, whose high-tech sectors imported 78% of their uncommon earth metals from China between 2017 and 2020, in line with the US Geological Survey.

The Biden administration’s nationwide safety technique, revealed in October 2022, recognized uncommon earth provide chains as a significant concern. A 2021 Protection Division assessment additionally concluded that overreliance on China “creates threat of disruption and of politicized commerce practices” that will hit business sectors significantly laborious.

China beforehand suspended exports of uncommon earths to Japan following tensions in 2010 surrounding the Senkaku Islands, which additionally alarmed these in Washington.

The US has since moved to bolster its home uncommon earth provide chain, with a level of success. USGS knowledge reveals that China’s share of all uncommon earths produced globally dropped to roughly 70% final 12 months from about 90% a decade earlier.

However, China nonetheless has a agency maintain on the processing of uncommon earths. This previous June, Beijing unveiled an inventory of uncommon earth rules geared toward defending provides within the title of nationwide safety, laying out guidelines on the mining, smelting and commerce within the crucial supplies used to make merchandise from magnets in electrical automobiles to client electronics, Reuters reported.

That information was adopted by the imposition of export limits on antimony and associated parts in August. Final 12 months China accounted for practically half of all mined output of the steel, utilized in navy purposes equivalent to ammunition, infrared missiles, nuclear weapons and evening imaginative and prescient goggles, in addition to in batteries and photovoltaic tools.

CNN quoted uncommon earths analysts at China Securities saying that growing demand for arms and ammunition attributable to wars and geopolitical tensions was prone to see tightening management and stockpiling of antimony ore.

Final December, China banned the export of expertise to make uncommon earth magnets. Beijing has additionally tightened exports of some graphite merchandise, and imposed restrictions on exports of gallium and germanium merchandise broadly utilized in semiconductors, CNN acknowledged.

Trade Week gave six explanation why China’s risk to ban crucial minerals exports just isn’t a bluff, listed under with mild enhancing:

- China has beforehand carried out export restrictions and bans. China blocked uncommon earth exports to Japan in 2010 and banned exports of uncommon earth processing expertise in 2023.

- China may benefit from imposing mineral export bans. Export bans on choose minerals would display that China can retaliate in opposition to U.S. efforts to curb expertise exports to China—and presumably deter america from additional restrictions, enabling China to refill on U.S. expertise.

- Chinese language mineral producers may doubtless discover various prospects to america. Some growing areas like Southeast Asia have growing mineral demand from their rising manufacturing sectors that China’s mineral producers may faucet into.

- China’s dominance of the crucial mineral business is much larger than Russia’s affect on the pure fuel business. Thus, the implications of China reducing off crucial mineral exports to america are doubtless broader and extra extreme than Europe dropping Russian pure fuel exports.

- America and its companion nations doubtless can not rapidly produce sufficient minerals to completely change imports from China.

- America would wrestle to incentivize sufficient mineral manufacturing in resource-rich nations exterior China.

To mitigate the dangers of potential Chinese language export bans, Trade Week suggests the US authorities ought to enhance stockpiling, noting the Nationwide Protection Stockpile is barely round 1% of its 1962 worth.

The NDS solely has 836 tons of nickel, lower than 5% of the Division of Protection’s annual nickel utilization, and it at present doesn’t comprise any of the 4 minerals used largely by the DoD: aluminum, copper, lead and fluorspar.

Along with stockpiling, Trade Week suggests the US authorities may supply low-cost financing to US corporations to safe offtake agreements with trusted suppliers, i.e., the “friend-shoring” we beforehand wrote about. The article notes US automakers are already pursuing offtake agreements for lithium, utilized in EV batteries.

The federal government must also enhance funding for mineral exploration. Whereas we at AOTH are leery of presidency funding, preferring to boost funds in the marketplace or by personal placements, a taxpayer-funded increase to mining wouldn’t come incorrect, both. Trade Week states:

Exploration is vital for growing the U.S. mineral provide and lowering reliance on China. Underneath Title III of the Protection Manufacturing Act (DPA), the U.S. Division of Protection is funding some mineral exploration efforts, together with nickel exploration in Minnesota and cobalt exploration in Idaho. Title III additionally permits the division to fund mineral exploration in Canada, Australia and the UK, as these nations are thought of “home sources.”

China’s bans on the export of crucial minerals processing expertise and on exports of sure crucial minerals over the previous few months has been met with powerful speak from politicians in Canada and the US.

Earlier this month, the Globe and Mail reported that Canada has begun the method to impose tariffs on Chinese language batteries and important minerals. In August, the nation hiked tariffs on Chinese language-made automobiles from 6% to 106%, efficient Oct. 1.

The transfer places Canada consistent with america, which introduced plans to extend tariffs on related gadgets within the spring.

Tariffs of 25% will likely be utilized to some metal and aluminum merchandise made in China on Oct. 15, the Globe acknowledged.

In response to CNN, the Biden administration final week finalized tariff hikes on sure Chinese language-made merchandise first introduced in Might.

The tariff charge will go as much as 100% on electrical automobiles, to 50% on photo voltaic cells and to 25% on electrical car batteries, crucial minerals, metal, aluminum, face masks and ship-to-shore cranes starting September 27, in line with the US Commerce Consultant’s Workplace.

Tariff hikes on different merchandise, together with semiconductor chips, are set to take impact over the following two years.

Former President Trump now operating for a second time period, and Vice President Kamala Harris, have each talked about tariffs whereas campaigning. Trump carried out tariffs on about $300 billion of Chinese language-made merchandise whereas in workplace 2016-20.

President Biden has saved these tariffs in place and determined to extend a number of the charges on about $15B of Chinese language imports. If elected, Trump has pledged to considerably enhance the tariffs the US has on imports from everywhere in the world. He’s calling for as much as 20% tariffs on each international import and has known as for an extra tariff as much as 60% on Chinese language imports. He would additionally impose a 100% tariff on nations that cease utilizing the US greenback.

Harris has not given many particulars on her tariff coverage apart from to assault her opponent’s tariff proposals as a “Trump gross sales tax”.

Research have discovered that American shoppers have borne nearly your entire value of Trump’s tariffs on Chinese language merchandise, CNN stated.

China has launched a criticism on the World Commerce Group over Canada’s EV tariffs, and is already determining methods to skirt US tariffs. BYD, China’s largest EV automaker, is reportedly reviewing potential areas for a plant in Mexico that will enable it to convey its cheaper electrical automobiles into america tariff-free, beneath the United States-Mexico-Canada Settlement (previously NAFTA). A minimum of a dozen Chinese language electric-car part suppliers have additionally introduced new factories or added to their present investments in Mexico in recent times, in line with the Wall Road Journal.

Conclusion

If america and Canada are to minimize the grip that China at present has over our crucial mineral provides, we’re enjoying a harmful sport — poking the bear with a big stick with out having a back-up plan as to what occurs if the stick doesn’t forestall the bear from charging and ripping out our throats.

By that I imply we at present mine valuable few of the crucial minerals wanted to construct an electrified economic system, and we lack the smelters for processing them and the technical know-how to take action.

By pissing off China with tariffs, are we not reducing our nostril to spite our face? We don’t wish to see an inflow of low-cost Chinese language-made merchandise dumped on North American markets, however certainly the answer is to mine, course of and manufacture the merchandise that we want at dwelling, quite than stopping them on the border.

The scenario is dire and it begins with mining. The S&P report is deceptive in that it reveals that main mining corporations are exploring for extra gold, however they’re doing it on their very own properties, typically mining across the edges of deposits found many years in the past.

They’re doing nothing to exit and discover new mines, however that has by no means been a significant’s job. It’s the job of juniors to find new mineral deposits however they don’t seem to be being financed; they actually don’t have any cash and are conducting financings at 5-10 cents, thus blowing out their share constructions.

Or doing bought-deal financings to institutional minded buyers who’re solely too prepared to promote their instantly saleable (no 4 month maintain) shares and journey the warrants until train.

If North America doesn’t have the metals it wants. that China has locked up, after which China turns round and says we’re not promoting them to you, what are we going to do? Proper now the business’s resolution is to go poking round their very own brownfield initiatives to seek out extra steel to mine. It’s a far cry from what we’re going to want.

It’s elemental to the mining business that the juniors are effectively financed, deposits have a shortened path to manufacturing, say 5 years like in Scandinavia, versus as much as 28 within the US. Juniors must be out within the bush making discoveries.

As a result of solely with the assistance of juniors can mining clear up its existential downside of getting the assets which might be at present owned by its adversaries. Junior useful resource corporations discover the assets miners then purchase and switch into their mineable reserves.

Actually, I don’t assume it’s a lot of a stretch to say that with out financed juniors, with out a protected and safe provide of metals, with out safety of provide, with out refineries and smelters, and with out the technological information to fabricate magnets and anodes for instance the developed economies of the western world are very a lot in danger if provides of those crucial metals, and related applied sciences, come from our opponents.

Authorized Discover / Disclaimer

Forward of the Herd publication, aheadoftheherd.com, hereafter often known as AOTH.

Please learn your entire Disclaimer rigorously earlier than you employ this web site or learn the publication. If you don’t conform to all of the AOTH/Richard Mills Disclaimer, don’t entry/learn this web site/publication/article, or any of its pages. By studying/utilizing this AOTH/Richard Mills web site/publication/article, and whether or not you really learn this Disclaimer, you’re deemed to have settle fored it.