That mentioned, it’s not instantly apparent who’s subsequent on the block. Henry may wait the obligatory six months and have one other pop at Anglo, however he’d nonetheless must work out learn how to separate the UK-listed miner’s juicy copper mines from the opposite bits he doesn’t need. Anglo boss Duncan Wanblad, in the meantime, is unlikely to be an M&A aggressor — his profitable defence towards BHP requires him to spend the following 12 months or so hiving off drawback areas like diamonds. Rio Tinto, the opposite massive international mining beast, was assumed to be ready to pounce on different targets whereas BHP was distracted swallowing Anglo — which it now isn’t.

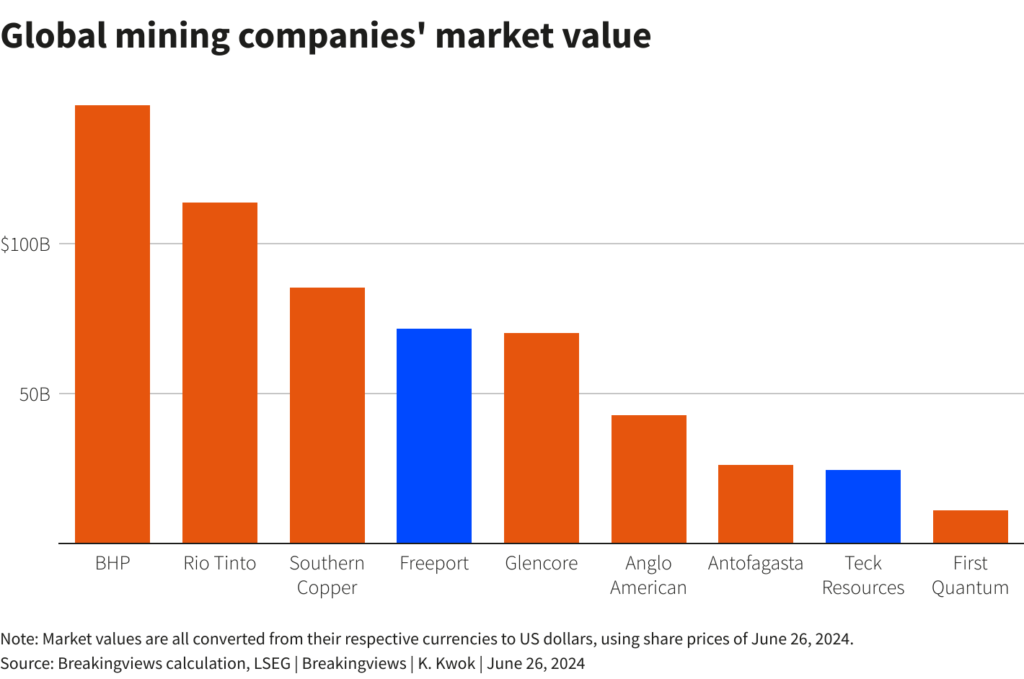

The image doesn’t essentially get any clearer within the subsequent echelon down. Main copper-focused gamers embody $26 billion Antofagasta, whose shares have doubled within the final two years, and $85 billion Southern Copper. These boast annual manufacturing of over 600,000 tonnes and 900,000 tonnes respectively. However Antofagasta is 65% owned by Chile’s Luksic household, which isn’t displaying indicators of promoting, and Southern Copper is 90% held by Grupo México – led by Mexican tycoon Germán Larrea Mota-Velasco. Canada’s $11 billion First Quantum Minerals had over 700,000 tonnes of annual copper output final 12 months, however its Cobre Panamá mine within the Central American state has been embroiled in a spat with the home authorities.

Freeport, which is in distinction largely held by institutional traders, appears a extra promising M&A candidate. CEO Kathleen Quirk, who took the reins this month, wants to seek out methods to make her fairness story extra thrilling: analysts anticipate Freeport’s copper manufacturing to barely improve within the subsequent 5 years at 1.3 million tonnes yearly, in accordance with estimates polled by Seen Alpha. She additionally not too long ago conceded in a Monetary Instances interview that acquisition, whereas not her precedence, was an efficient technique to increase copper output.

Teck is alluring for a starker motive. Boss Jonathan Worth’s copper manufacturing may roughly double to almost 600,000 tonnes by 2028, in accordance with analysts estimates utilizing Seen Alpha knowledge, and Teck’s 60% copper EBITDA margin forecast for 2025 exceeds Freeport’s 45%. Whereas the Keevil household exerts an Antofagasta-style grip on the shareholder register, its particular voting shares will flip to frequent inventory in 5 years. After he completes the sale of Teck’s steelmaking coal enterprise to Swiss rival Glencore, Worth’s group will develop into a vastly enticing goal.

The catch for events is that this attract is considerably already within the costs of the extra centered base steel gamers. Freeport’s shares have gained 360% up to now 5 years, in comparison with 17% for much less copper-exposed Rio, BHP and Anglo. After deducting the earnings generated by coal, Teck is buying and selling at 12.4 instances the remaining EBITDA analysts estimate it to generate in 2024, utilizing Seen Alpha knowledge, with Southern Copper at 14.6 instances and Freeport and Antofagasta at 7 instances. Add a premium on prime of that and Henry and his extra diversified miner friends can be at extreme danger of overpaying: BHP, Rio and Anglo commerce on common at simply 5 instances, so the hazard is that they hand all of the synergy advantages to their targets’ shareholders.

This doesn’t imply Teck and Freeport don’t have any hope of being concerned in massive M&A. That’s as a result of they might use their costly shares to develop into acquirers. There are many choices. Teck’s $25 billion worth provides it almost the identical market capitalization as Antofagasta, whereas Vale’s base steel enterprise was valued at the same value when it bought a one-tenth stake to shareholders together with Saudi Arabia final 12 months. Worth, or his counterparts at Freeport or Southern Copper, may use their fairness to dealer an all-share merger with one in every of this cohort.

Anglo and Glencore may very well be in play too. After spinning off its coal, diamond and platinum companies, Anglo could be smaller, however extra uncovered to base metals. Worth its $3.8 billion of estimated copper EBITDA in 2024 on the identical degree as pure steel gamers like Freeport, and it could be value $27 billion. Wanblad may really feel the necessity to spin out his base metals enterprise pre-emptively if he fails to ship Anglo’s restructuring plan by 2025. In the meantime, Glencore is buying and selling at solely 4.6 instances 2024 EBITDA. If it determined to spin off its large coal companies, the likes of Freeport may fancy what’s left behind — analysts estimate Glencore’s personal copper enterprise will generate $4.8 billion of EBITDA in 2024, implying a possible valuation nearing $35 billion on Freeport’s 7 instances a number of.

It’s not not possible antitrust hurdles lie within the path of any Teck or Freeport M&A splurge. The Canadian authorities, in spite of everything, wasn’t overly welcoming in the direction of Glencore’s bid for everything of Teck in 2023. Quite than have interaction in dangerous M&A, Teck or Freeport might but desire to spend assets on new applied sciences to squeeze extra copper out of their very own current tasks. Nonetheless, it wasn’t in any respect clear BHP would swoop for Anglo as a result of complexity of the political backdrop, and it did so anyway. Copper watchers ought to keep tuned for additional fireworks.

Context information

Freeport-McMoRan chief government Kathleen Quirk mentioned in a Monetary Instances interview revealed on June 17 that lowering the sector from scores of teams right into a small variety of giants may very well be an efficient technique to buoy provides wanted to chop emissions within the a long time forward.

Quirk took cost as chief government of Freeport on June 11. Glencore’s deal to purchase Teck’s coal mines is anticipated to shut within the third quarter.

(The writer, Karen Kwok, is a Reuters Breakingviews columnist. The opinions expressed are their very own.)

(Enhancing by George Hay and Streisand Neto)