Glencore is within the means of buying 77% of Teck Sources’ coal enterprise in a deal that values the enterprise at $9 billion, or greater than 4 occasions subsequent yr’s estimated EBITDA, in accordance with LSEG information. In Australia, which accounts for roughly half of all coking coal exports, there’s extra exercise. A BHP-Mitsubishi Corp three way partnership, for instance, simply bought two mines for about 3 occasions EBITDA, or $3.2 billion, to Whitehaven Coal, which can flog a minority stake to a steelmaker.

Coking coal has what for now could be a novel pitch. It gives the warmth and carbon vital for blast furnaces to show iron ore into molten iron, used to provide about 70% of the world’s 1.8 billion tons of metal every year. The remaining comes from scrap metallic refashioned in electric-arc furnaces, like ones on the coronary heart of Nippon Metal’s fraught plan to purchase United States Metal. This lower-energy course of, whose furnaces use much less if any coal, is projected to turn out to be as a lot as half the market by 2050. The dirtier technique is ready to continue to grow in India and different elements of Southeast Asia, the place manufacturing might soar 50% over the identical span, in accordance with Wooden Mackenzie analysts.

The open secret, nevertheless, is that coking coal is extra poisonous than what will get shovelled into energy crops. Thermal coal accounts for a few fifth of the world’s greenhouse gasoline emissions, double what steelmaking spews. However coking coal, which is answerable for many of the metallic’s air pollution, does so with only a fifth of the tonnage mined. Its vital methane content material means toxins emitted from pits alone are virtually thrice increased than from thermal coal, Wooden Mackenzie has estimated.

There are additionally no useful options in the identical means that photo voltaic, wind and different renewable sources are supplanting fossil-fuel energy stations. Loads are within the works, nevertheless. Inexperienced hydrogen is one, closely funded by Andrew Forrest’s iron ore miner Fortescue and others. Rival Rio Tinto can also be engaged on utilizing biomass and microwave power. Boston Metallic – backed, amongst others, by BHP, steelmaker ArcelorMittal and German carmaker BMW – goals to commercialize the molten oxide electrolysis course of.

These choices will not be able to compete at a big stage for a decade. This helps clarify the decreased stigma connected to unearthing coking coal in comparison with its electricity-generating thermal cousin.

It’s additionally why the current improve in offers doesn’t appear to be notably contentious. Even BHP boss Mike Henry touted coal mines as considered one of Anglo American’s predominant points of interest after having spent 4 years as CEO pivoting to “future dealing with commodities” equivalent to copper. The essential concept is that Anglo’s mines principally maintain the identical premium-grade exhausting coking coal as BHP’s remaining pits simply down the street. The variability has fewer impurities and normally decrease emissions.

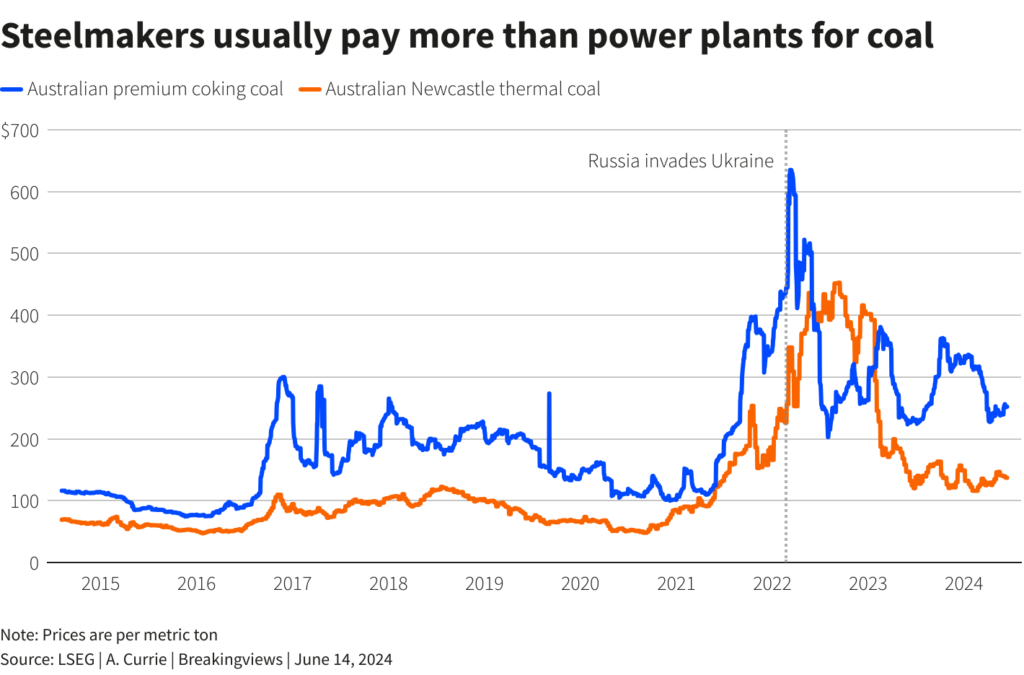

Profitability helps, too. Premium exhausting coking coal sells for round $250 a metric ton, with BHP spending roughly $100 and Anglo $115 to dig it up. Mushy coking coal sells for round a 3rd much less. Thermal coal, in the meantime, fetches lower than $140 a ton, with prices starting from $50 to greater than $100.

Small surprise that thermal coal producers had been the consumers within the two largest coking coal offers. Of the 113 million tons of coal Glencore excavated final yr, lower than a tenth was destined for blast furnaces. Teck’s met coal unit will double that proportion and contribute a 3rd of income, based mostly on final yr’s figures. The concept is that mixed, the enterprise can be value extra in a by-product deliberate by Glencore CEO Gary Nagle.

With BHP-Mitsubishi’s quantity, Whitehaven will greater than double its total manufacturing and catapult the top-line contribution from met coal to about 70% from lower than 10%. The merger additionally ought to increase its EBITDA margin and finally encourage traders to worth the enterprise at extra than simply 3 occasions these anticipated earnings over the following 12 months, per LSEG information. The deal additionally takes the corporate tantalizingly near the edge – 25% of income from thermal coal – that may make it simpler to faucet mainstream banks and insurers.

A few of the offers appear like steals, a minimum of on paper. Glencore’s return on its mooted Teck funding may very well be as excessive as 19%, based mostly on final yr’s exhibiting. And if BHP had been to pay, say, $5 billion to purchase Anglo’s coal mines, or round 4 occasions 2025 EBITDA per Seen Alpha information, after which lower its goal’s prices by a tenth, it’d generate 14% on its capital, Breakingviews calculates.

All else being equal, Glencore would possibly recoup its outlay in simply 5 years, far earlier than even the chirpiest projections for inexperienced hydrogen and different know-how to compete. A putative BHP acquisition of Anglo’s metallurgical belongings would take seven years to repay.

If coal costs drop by a 3rd to their pre-Ukraine conflict band, although, a crude calculation signifies the deal payback timeline would roughly double. That’s assuming prices don’t rise. Many mines in Australia’s chief coking coal area have already got been damage immediately or not directly from flooding worsened by local weather change. Such occasions will improve as extra fossil gas emissions are pumped into the ambiance.

The extra such disasters, the higher impetus there could also be to curb air pollution, placing a much bigger goal on steelmaking. BHP and others anticipating that premium coal can be extra sturdy sound optimistic: Teck has identified that growing exhausting coking coal’s quantity within the furnace to 70% from 50% reduces carbon emissions by lower than 7%.

Furthermore, climate-linked import duties, together with Europe’s carbon border adjustment mechanism, can be totally up and operating earlier than lengthy. Dealmaking is stoking the embers of coking coal, but additionally the chase in opposition to cleaner replacements.

(By Antony Currie; Enhancing by Jeffrey Goldfarb and Aditya Srivastav)