Whereas the deal finally failed, the truth that BHP was keen to pay $39 billion for Anglo’s copper mines says quite a bit concerning the significance of copper to the electrified financial system, and the businesses that mine it.

As this text will show, it isn’t solely BHP that’s attempting to find copper, which is now essentially the most crucial mineral on Earth because of it being a required uncooked materials in electrical automobiles and renewable vitality, but in more and more brief provide.

Certainly the complete provide chain — from upstream miners to downstream customers, and every part in between, together with majors, mid-tiers, juniors and copper smelters — is screaming for copper, attempting desperately to lock up provide earlier than the world runs out, as demand overtakes obtainable portions as early as subsequent yr.

Copper

Copper is likely one of the most vital metals with greater than 20 million tonnes consumed every year throughout a wide range of industries.

Lately, the worldwide transition in direction of clear vitality has stretched the necessity for the bottom steel even additional.

Merely put, electrification doesn’t occur with out copper, the heartbeat of the worldwide vitality financial system.

Together with the same old functions in building wiring and plumbing, transportation, energy transmission and communications, there may be now added demand for copper in electrical automobiles and renewable vitality methods.

Thousands and thousands of ft of copper wiring can be required for strengthening the world’s energy grids, and lots of of hundreds of tonnes extra are wanted to construct wind and photo voltaic farms. Electrical automobiles use triple the quantity of copper as gasoline-powered vehicles. There’s greater than 180 kg of copper within the common dwelling.

Further copper is being demanded by the electrification of public transportation methods, 5G and AI.

Depletion & manufacturing issues

Manufacturing issues unfold to MSM late final yr, when the federal government of Panama ordered First Quantum Minerals (TSX:FM) to close down its Cobre Panama operation, eradicating practically 350,000 tonnes from world provide.

A strike at one other giant copper mine, Las Bambas in Peru, quickly halted shipments.

Copper specialist Anglo American now says it’s scaling again output by about 200,000 tons, owing to go grade declines and logistical points at its Los Bronces mine. Los Bronces manufacturing is predicted to fall by practically a 3rd from common historic ranges subsequent yr because the miner pauses a processing plant for upkeep, Reuters stated Tuesday.

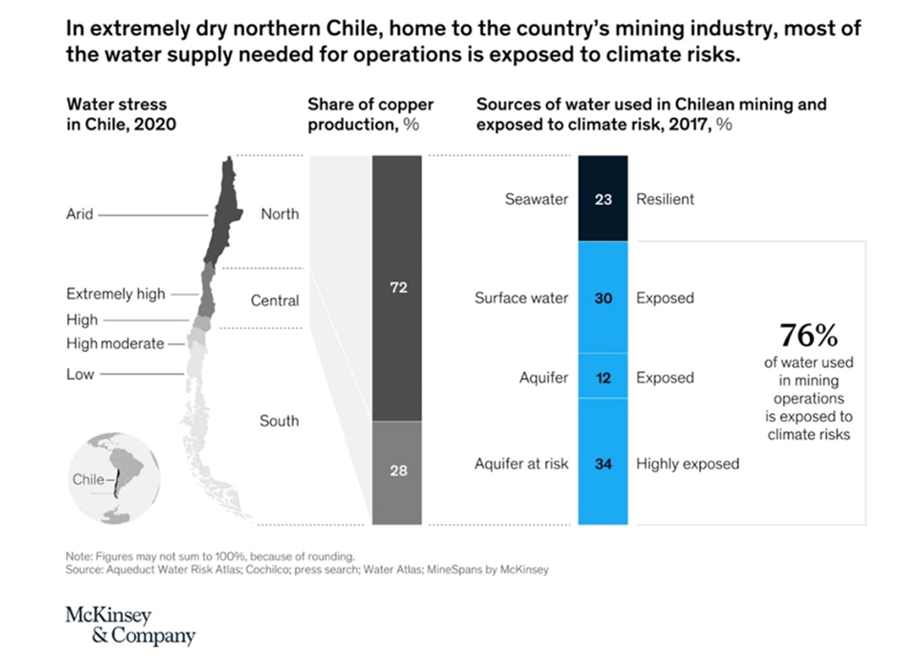

Chile’s copper output has been dented by a long-running drought within the nation’s arid north. State miner Codelco’s 2023 manufacturing was the bottom in 25 years.

All 4 of Codelco’s megaprojects have been delayed by years, confronted price overruns totaling billions, and suffered accidents and operational issues whereas failing to ship the promised increase in manufacturing, based on the corporate’s personal projections.

There are additionally issues about Zambia, Africa’s second largest copper producer, the place drought circumstances have lowered dam ranges, creating an influence disaster that threatens the nation’s deliberate copper growth.

Ivanhoe Mines (TSX:IVN) reported a 6.5% quarterly drop in manufacturing on the world’s latest main copper mine, Kamoa-Kakula within the DRC.

The tightness of the copper focus market has been mirrored in therapy and refining prices plummeting from over $90 per tonne to under $10/t. This drastic discount compelled Chinese language smelters, answerable for round half of world refined copper manufacturing, to think about a ten% manufacturing minimize.

n a earlier article, we dug deep into the availability cuts to get an concept of how a lot copper is really being produced. Our evaluation confirmed suspicions that it’s significantly lower than a number of years in the past.

Greatest copper mines produced 20% much less copper in 2023

Our first step was consulting Visible Capitalist’s 2021 graphic of the world’s 20 largest copper mines by manufacturing capability.

The determine under exhibits Escondida in Chile main the pack, at 1.4 million metric tons capability each year, by means of to quantity 20 First Quantum’s Sentinel mine in Zambia with its 260,000 tpa capability. 5 of the 20 mines “tied” for having the identical quantity of capability.

These 20 mines have the capability to provide practically 9 million tonnes of copper yearly, representing 44% of world manufacturing in 2020.

However how a lot did they really produce in 2023?

AOTH combed by means of quarterly and annual reviews, press releases and information articles to seek out out.

Of the mines we may discover 2023 manufacturing figures for, the overall got here to five,818,792 tonnes. Solely two — now-shuttered Cobre Panama and Grasberg (Freeport McMoRan’s 231,836t +204,960t estimated manufacturing from PT Inalum and PT Indonesia based mostly on 51.24% possession) — produced greater than their 2020 manufacturing capacities. The remainder produced much less.

We needed to discover a strategy to compensate for the lacking information for six mines. We determined to make use of every particular person mine’s 2020 manufacturing capability because the (lacking) 2023 manufacturing determine. For instance, no figures had been discovered for Southern Copper’s Buenavista mine in Mexico, so for 2023 we used its 2020 manufacturing capability of 520,000 tonnes. This generously estimates the quantity of copper that was really produced final yr, since most, if not all of those mines with lacking information doubtless produced lower than their manufacturing capability.

Including 1,592,960 tonnes of estimated 2023 manufacturing (for six mines) to the 5,818,792 tonnes of precise 2023 manufacturing for the remaining 14 mines provides a complete of 7,411,752 tonnes — 19.6% lower than 2020’s whole capability for the world’s high 20 mines of 8,869,000 tonnes.

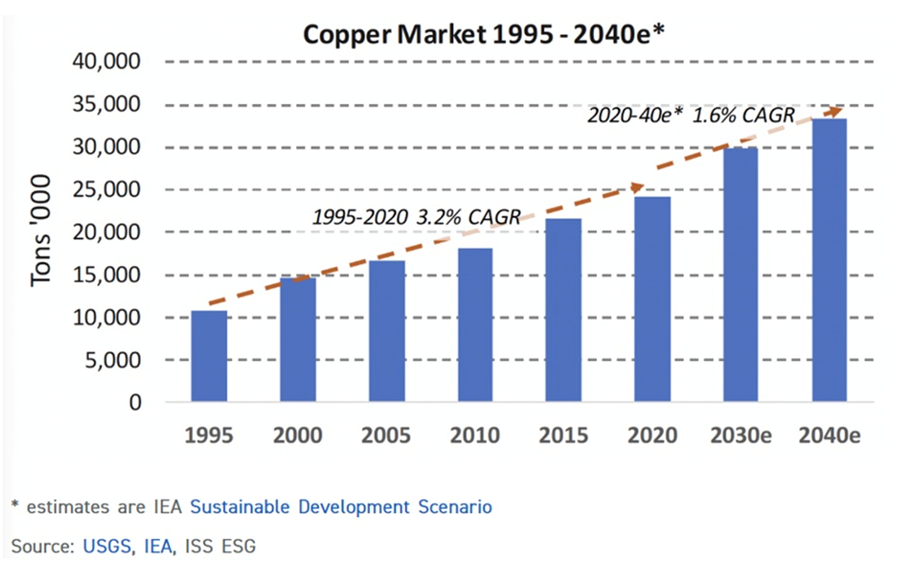

Benchmark Mineral Intelligence (BMI) forecasts world copper consumption to develop 3.5% to twenty-eight million tonnes in 2024, and for demand to extend from 27 million tonnes in 2023 to 38 million tonnes in 2032, averaging 3.9% yearly development.

But the US Geological Survey reviews provide from copper mines in 2023 amounted to solely 22 million tonnes. If the copper provide doesn’t develop this yr, we’re a 6Mt deficit.

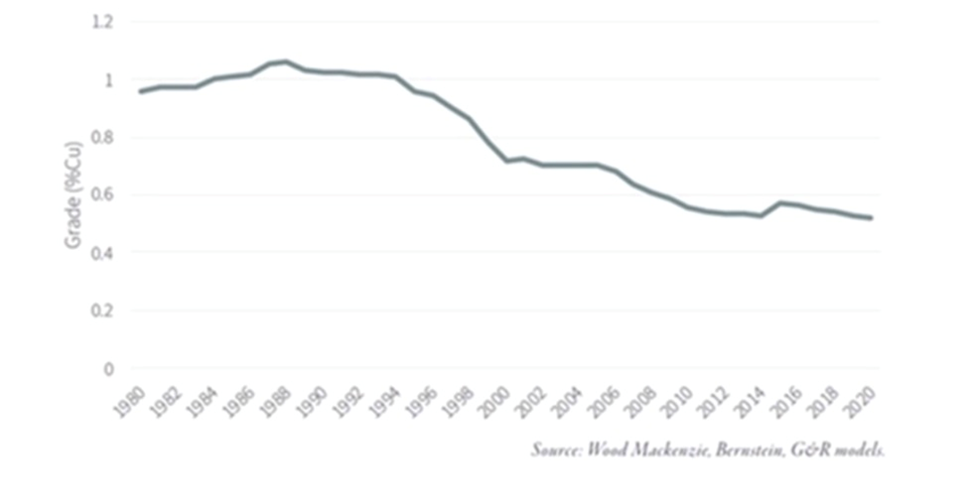

As our calculations present, that 22 million tonnes of manufacturing displays roughly a 20% discount in output from the highest 20 copper mines. If provide interruptions proceed in a number of the high producers, like Chile, Peru, Zambia and the DRC, the deficit may develop even greater, and sure will. Extra labor unrest at Las Bambas in Peru is looming. Chile continues to have water issues and based on the Worldwide Power Company, common copper grades there have declined by 30%.

Wall Avenue commodities funding agency Goehring & Rozencwajg says the business is “approaching the decrease limits of cut-off grades and brownfield expansions are not a viable answer. If that is right, then we’re quickly approaching the purpose the place reserves can’t be grown in any respect.”

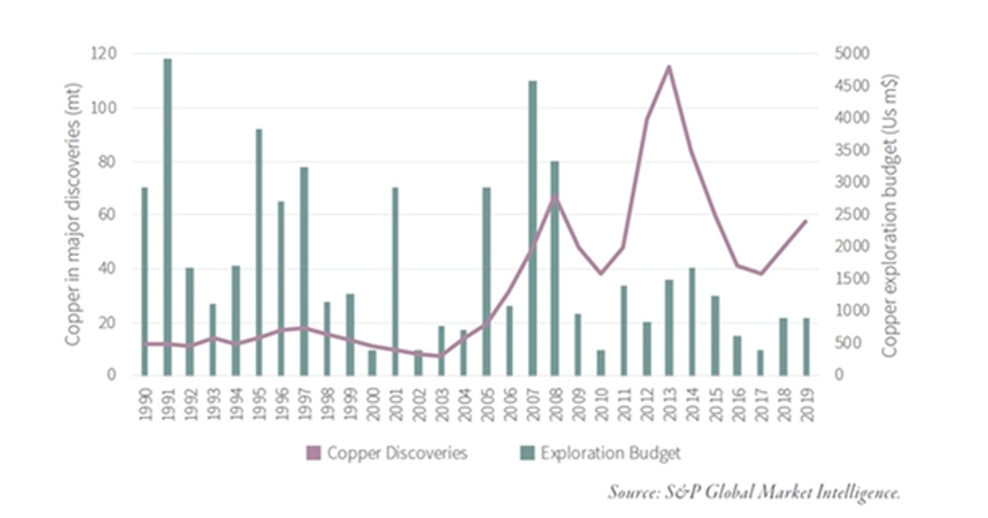

The significance of creating new discoveries in establishing a sustainable copper provide chain is apparent.

Exposing the copper surplus fable — Richard Mills

Greenfield additions to copper reserves have slowed dramatically, with tonnage from new discoveries falling by 80% since 2010.

Bloomberg New Power Finance says copper miners must double the quantity of world copper manufacturing, simply to satisfy the demand for a 30% penetration charge of electrical automobiles — from the present 22Mt a yr to 40Mt.

Copper consumption by inexperienced vitality sectors globally is predicted to leap five-fold from 2020 to 2030, information from consultancy CRU Group exhibits.

Future copper utilization is carefully tied to assembly carbon emissions targets.

To transition from a fossil fuel-based financial system to at least one run on clear energy together with the electrification of the worldwide transportation system, would require a colossal increase within the manufacturing of mined supplies, together with copper.

Larger penetration of photo voltaic, wind and vitality storage all would require copious metals.

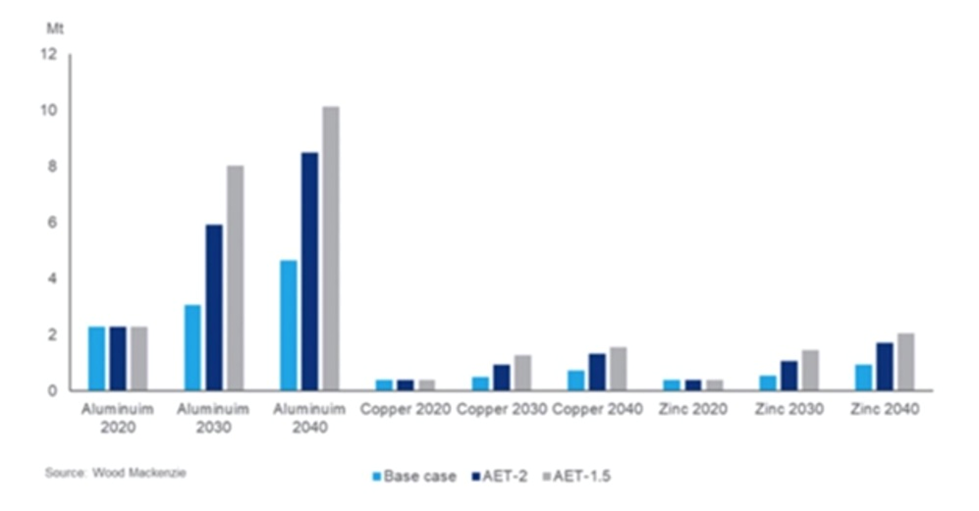

Wooden Mackenzie, a commodities consultancy, predicts that utilization of aluminum, copper and zinc in photovoltaics will double by 2040.

“Copper is utilized in excessive and low voltage transmission cables and thermal photo voltaic collectors,” Kamil Wlazly, Wooden Mackenzie’s senior analysis analyst, wrote within the report.

Below a base case situation, according to a 2.8 to three˚C world warming view, the report expects aluminum demand from photo voltaic to rise from 2.4 million tonnes in 2020 to 4.6Mt in 2040; base case copper demand would go from 0.4Mt in 2020 to nearly 0.7Mt; and world zinc consumption would double from 0.4Mt 0.8Mt within the base case.

There are two methods for the mining business to extend copper reserves: it could both discover giant new deposits to grow to be mines; or copper corporations can decrease their cut-off grades and add new reserves that manner.

A few of the world’s largest copper corporations are doing every part they will to broaden current mines and purchase potential new deposits, as they search to interchange their quickly depleting copper reserves and sources.

We’ve already talked about BHP’s curiosity in copper, evidenced by its $39B bid for Anglo American final yr.

Anglo has indicated that South Africa could be a very good jurisdiction to discover. Copper, nickel, lead, and zinc are among the many base metals the corporate is focusing its world discovery technique in greenfield and brownfield initiatives.

Barrick Gold (TSX:ABX) desires to diversify into the pink steel from the yellow. The corporate already owns the Porgera mine in Papua New Guinea, which borders Indonesia to the east, with China’s Zijin Mining.

One other huge gold miner, Newmont Corp (TSX:NGT), in 2021 struck a cope with GT Gold, to take over the junior and its Tatogga gold-copper discovery within the Golden Triangle of northwestern British Columbia.

Why are main mining corporations so intent on securing new provides of copper? Fairly merely, they’re operating out of ore.

With out new capital investments, Commodities Analysis Unit (CRU) predicts world copper mine manufacturing will drop from the present 22 million tonnes to under 12Mt by 2034, resulting in a provide shortfall of greater than 15Mt. Over 200 copper mines are anticipated to expire of ore earlier than 2035, with not sufficient new mines within the pipeline to take their place.

A few of the largest copper mines are seeing their reserves dwindle; they’re having to dramatically sluggish manufacturing because of main capital-intensive initiatives to maneuver operations from open pit to underground. Examples embrace the world’s two largest copper mines, Escondida in Chile and Grasberg in Indonesia, together with Chuquicamata, the most important open-pit mine on Earth.

These cuts are vital to the worldwide copper market as a result of Chile is the world’s greatest copper-producing nation — supplying 30% of the world’s pink steel. Including insult to damage, copper grades have declined about 25% in Chile during the last decade, bringing much less ore to market.

Greenfield and brownfield reserve additions are anticipated to disappoint by means of the last decade, based on Goehring & Rozencwajg. S&P International Market Intelligence estimates that new discoveries averaged practically 50Mt yearly between 1990 and 2010. Since then, new discoveries have fallen by 80% to solely 8Mt per yr. (I might really be shocked if 8Mt of copper is being discovered yearly. It’s doubtless significantly much less — Rick)

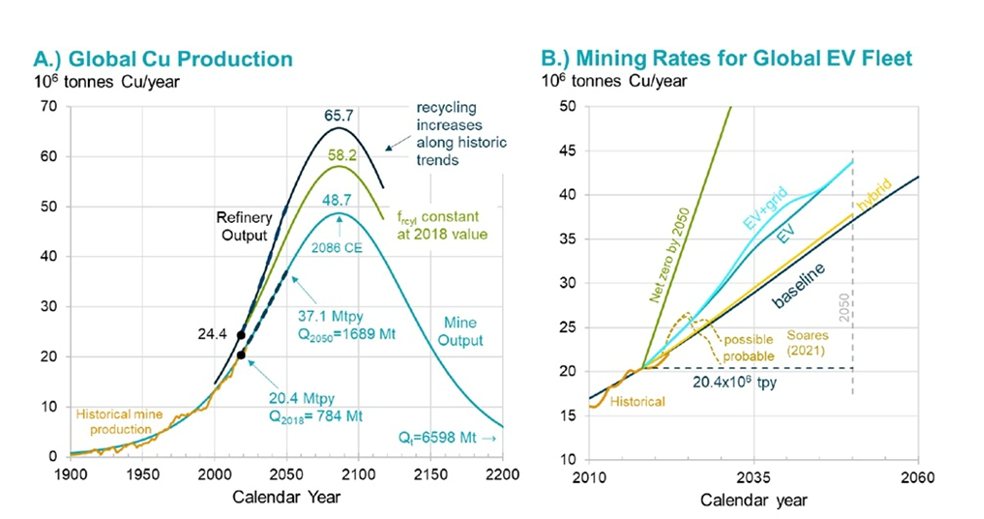

The diploma to which the business has did not convey on new mines is obvious in a new examine by the College of Michigan and Cornell College. The researchers discovered that copper can’t be mined quick sufficient to maintain up with present US coverage tips to make the transition from fossil-fueled energy and transportation to electrical automobiles and renewable energies.

How inconceivable? The researchers discovered between 2018 and 2050, the world might want to mine 115% extra copper than has been mined in all human historical past to 2018. This might meet our present copper wants and assist the growing world with out contemplating the inexperienced vitality transition.

To impress the worldwide car fleet requires bringing into manufacturing 55% extra new mines. Between 35 and 195 giant new copper mines must be constructed over the following 32 years, at a charge of as much as six mines per yr. Spoiler alert – ain’t gonna occur, in different phrases an inconceivable job. In closely regulated environments like the US and Canada, it could take as much as 20 years to construct one mine from scratch.

China

Their reserves dwindling, head grades decrease, an absence of latest discoveries, and manufacturing snafus because of a litany of issues together with indigenous relations, NGO’s, useful resource nationalism, world warming/ energy cuts and shortages of water is it any marvel that international locations (and corporations) needing copper are wanting elsewhere for it?

The posterchild for this pattern is China, which within the Nineteen Nineties and early aughts, went purchasing for the minerals it wanted to feed its financial system that, till 2015, was rising at double digits. Beijing invested billions both by means of the acquisition of mining and vitality firm stakes, or outright mine acquisitions. At first, the buys had been concentrated in Africa, with iron ore and copper the predominant commodities.

The concept was that deep-pocketed, state-funded miners would purchase initiatives for China’s home use.

The acquisition in 1998 of an 85% stake in Zambia’s Chambishi copper mine for about $20 million was certainly one of China’s earliest abroad mining investments.

China introduced a $5 billion mortgage to the DRC for infrastructure improvement in 2007, following up one other $3.8 billion for mining investments in 2008. The Export-Import Financial institution of China pledged an almost $9 billion mortgage to construct and improve the DRC’s highway (4,000 km) and rail system (3,200 km) for transportation routes that join its extractive industries, and to develop and rehabilitate the nation’s mining sector, in return for copper and cobalt concessions. China would acquire rights to extract as much as 10 million tons of copper and 420,000 tons of cobalt (confirmed deposits) over a 15-year interval.

The China Non-Ferrous Metals and Development (CNMC) and Yunnan Copper Trade in 2013 commissioned a $300 million copper smelter in Zambia’s Chambishi. (Institute of Creating Economies Japan Exterior Commerce Group (JETRO))

Extra not too long ago the specified metals are people who feed into the worldwide shift from fossil fuel-powered transportation and vitality era to electrical vehicles and renewables. This has meant a seek for lithium, cobalt, graphite, copper and uncommon earths.

How China is locking up crucial sources within the US’s personal yard

As a part of a plan to scale back debt, Rio Tinto (LSE:RIO) put its Northparks copper-gold mine in Australia on the block. China Molybdeum Co answered the decision, in 2013 paying $820 million for 80% of the asset.

Within the early 2010s, China started transferring into South America. State aluminum firm Chinalco purchased the Toromocho copper mine in Peru from a junior, Peru Copper, and started business manufacturing in 2010. Chinalco nonetheless owns the mine and in 2018 began an growth.

In 2014 a consortium of three Chinese language corporations — CITIC Metallic Co., MMG and Guoxin — acquired the Las Bambas copper mine in Peru from Glencore Xstrata in an all-cash deal price $5.85 billion.

Japanese corporations acquired in on the motion too. A information report from 2013 stated JX Nippon Mining & Metals was on monitor to greater than double copper manufacturing from its mines, the bulk coming from JX’s 75%-owned Caserones copper mine in Chile. (the mine is now 51% owned by Lundin Mining – see under)

In 2020, Mitsubishi Supplies was additionally energetic in Chile, agreeing to amass a 30% curiosity within the Montoverde copper mine and related initiatives from Mantos Copper for $263 million. The opposite 70% is held by Capstone Copper (TSX:CS).

A 3rd Japanese firm, Marubeni, holds a 30% stake within the Centinela and Antucoya copper mines and a 12.48% stake in Los Pelambres copper mine, all of that are in Chile. Marubeni operates the mines with Antofagasta plc (LSE:ANTO).

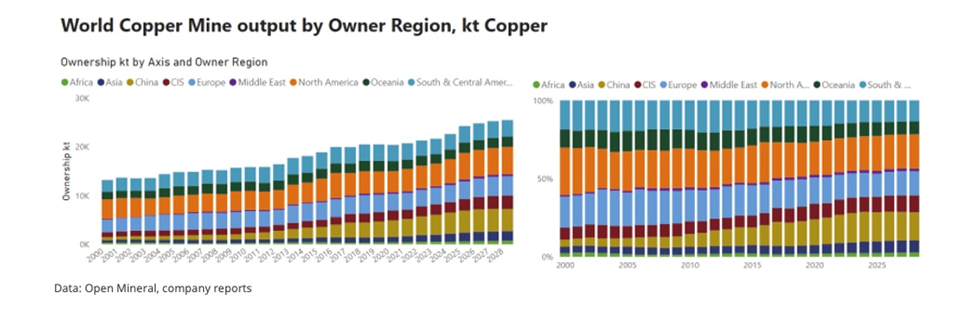

A latest report by Open Mineral studied tendencies in copper mine possession. “Probably the most hanging takeaway, say the report’s authors, “is that Chinese language corporations have dramatically elevated their fairness in world copper mine provide, from 5% initially of the century to 19% by 2023 following a sequence of forward-looking investments throughout the growing districts of the African copper belt and western China, in addition to strikes into extra mature mining areas in South America and Europe.”

“With China’s large copper smelting capability and manufacturing base, these investments signify a daring, long-term technique aimed toward securing copper provide for the nation’s future.”

“Whereas the quantity of mined copper owned by Western majors, mid-tier and junior miners has risen from 8.1Mt in 2000 to only over 10Mt in 2023, the general share of North America, Europe and Oceania has fallen from over 60% of world copper mined initially of the century to ~46% final yr. Firms from these areas have retreated to some extent from Asia ex-China, whereas regardless of key investments their share of African mine output has compressed as a result of a bigger proportion of latest copper belt provide has been developed by Chinese language corporations.”

We don’t must look very onerous to point out that is the case.

In 2018, China’s largest gold firm, Zijin Mining, took over Canada’s Nevsun Sources for $1.4 billion, including the Timok copper-gold venture in Serbia and a 60% stake in Eritrea’s Bisha copper-zinc mine to its asset portfolio.

The identical yr, Zijin paid $1.26 billion for 63% of Serbia’s largest copper mining and smelting firm, RTB Bor.

In Africa, Chinese language state-run conglomerate CITIC bought a 20% stake in Canada’s Ivanhoe Mines (TSX:IVN) for $723 million. The information launch says Ivanhoe will use the proceeds to advance its improvement initiatives in southern Africa, together with Platreef, Kipushis and Kamoa-Kakula within the DRC — the most important copper mine to open not too long ago, in July 2021.

The venture is a three way partnership between Ivanhoe (39.6%), Zijin Mining (39.6%), Crystal River International Restricted (0.8%) and the DRC authorities.

Ivanhoe signed two offtake offers, one with a subsidiary of Zijin Mining; the opposite with Chinese language commodities dealer CITIC Metallic, to promote every 50% of the copper manufacturing from Kakula — the primary of two mines concerned within the three way partnership. In different phrases, 100% of Kamoa-Kakula’s Part 1 manufacturing goes to China.

2023 noticed China’s MMG agreeing to pay $1.9 billion for Cuprous Capital, a non-public firm that owns the Khoemacau copper mine in Botswana.

Additionally final yr, South Africa’s Sibanye Stillwater (NYSE:SBSW) reportedly deliberate to usher in a Chinese language investor to type a partnership if it gained its bid to purchase Zambia’s Mopani Copper Mines. The story says Sibanye was competing with Zijin Mining, and that Sibanye’s CEO needed to diversify into copper from South Africa’s gold and platinum mines, the place output has been decreased because of blackouts and rising crime.

Ultimately it was Worldwide Sources Holding RSC of Abu Dhabi that gained the bid and can make investments $1.1 billion within the beforehand Glencore-owned mine.

The newest Chinese language copper acquisition once more concerned Zijin Mining, which in January of this yr stated it plans to take a 15% stake in Canadian copper firm Solaris Sources (TSX:SLS). In accordance with the Monetary Put up, the $130 million funding could be used to advance Solaris’ Warintza copper venture in Ecuador.

The majors

The largest copper merger to floor among the many main miners was BHP’s tried take-over of rival Anglo American.

The $39 billion acquisition was centered round Anglo’s South American copper belongings, however BHP walked away after Anglo rejected a last-ditch try for extra time, Reuters stated. The primary purpose for the deal’s collapse was the requirement that Anglo unbundle its South African platinum and iron ore companies. Mining.com famous {that a} tie-up would have given BHP about 10% of world copper manufacturing.

The mining large is definitely bold in its pursuit of copper. In April 2023 an Australian courtroom permitted its $6.4 billion takeover of OZ Minerals, which on the time was the corporate’s greatest M&A transaction since its $12.1B buy of Petrohawk Power in 2011.

OZ owned two working copper and gold mines in South Australia, Carrapateena and Distinguished Hill, in addition to the West Musgrave nickel and copper venture in Western Australia.

Late final yr, one other blockbuster copper buy-out plan made headlines. This time it was Glencore’s (LSE:GLEN) $22.5B bid for Canada’s largest diversified miner, Teck Sources (TSX:TECK). After a lot backwards and forwards, Glencore agreed to spend $6.93 billion for Teck’s metallurgical coal division, and merge it with its personal coal belongings — leaving Teck’s copper belongings intact. The proprietor of the Highland Valley copper mine in British Columbia can also be a component proprietor (with Newmont Mining) of Galore Creek, one of many world’s largest undeveloped copper-gold-silver deposits. Teck additionally has operations in Peru, Chile and the US.

The world’s second-largest miner, Rio Tinto (LSE:RIO), is investing in copper mines in Utah and Arizona. In 2017 Rio dedicated a further $302 million to the Decision copper venture. To this point, companions Rio Tinto (55%) and BHP (45%) have spent over $2 billion to develop the stalled venture, which has been within the allowing section since 2013.

The corporate in 2023 stated it intends to take a position about $920 million at its Kennecott copper operations in Utah as a part of a plan to extend its copper provide in North America.

In fact we will’t overlook about Newmont’s $16.8 billion buyout of Australia’s Newcrest Mining, which additionally accomplished in 2023. A cornerstone of the deal was Newmont diversifying from gold into copper, by buying Newcrest’s copper belongings, together with the manufacturing Cadia mine in Australia (17Moz of gold and three.6Mt of copper in reserve) and the Wafi-Golpu improvement venture in Papua New Guinea. One supply stated the tie-up doubled Newmont’s copper reserves.

Newcrest in 2019 bought 70% of the Crimson Chris copper-gold mine in British Columbia, forming a three way partnership with the mine’s proprietor, Imperial Metals (TSX:III). Newcrest’s 70% share transferred to Newmont when the Newmont-Newcrest deal was finalized.

Via our personal analysis, AOTH recognized extra copper investments:

- Chilean miner Antofagasta has secured $2.5 billion to finance a second concentrator at its Centinela copper mine. Lenders embrace the Japan Financial institution for Worldwide Cooperation, Export Improvement Canada and the Export-Import Financial institution of Korea.

- Commodities group Glencore (LSE:GLEN) is learning means by which to amass Anglo American, following BHP’s failed bid. The 2 corporations already co-own the Collahuasi copper mine in Chile, holding 44% apiece.

- China’s Jiangxi Copper purchased 25.9 million First Quantum Minerals’ shares, serving to the beleaguered Canadian miner to boost CAD$1.5 billion in February. First Quantum (TSX:FM) in 2023 had its Cobre Panama mine shut down by the federal government. The Chinese language agency, which holds 18.4% of FM, additionally agreed to purchase $500 million in copper shipments from a First Quantum mine in Zambia.

- Russian agency Norilsk Nickel has been pressured to shut its Arctic copper plant because of Ukraine-related sanctions. Reuters stated Norilsk will as a substitute construct a brand new plant in China by means of a three way partnership, with building slated for completion by mid-2027.

- Lundin Mining (TSX:LUN) in March of final yr acquired a majority curiosity in Chile’s Casserones copper-molybdenum mine. The Toronto-based firm paid $800 million for a 51% share of SCM Minera Lumina Copper Chile, a subsidiary of JX Nippon Mining & Metals, which operates the mine. Lundin will even pay JX $150 million in instalments over six years, and have the proper to amass a further 19% curiosity by paying $350M over 5 years.

Smelters

On the high we stated that each hyperlink within the copper provide chain is wanting steel and frightened about not getting sufficient. This contains copper smelters, which purchase the uncooked ore from mining corporations and refine it into completed merchandise, for a charge.

Whereas this seems to be a brand new pattern, in truth it goes way back to 2010. That yr, Dowa Metals & Mining, a unit of Dowa Holdings, Japan’s fourth-largest copper smelter, deliberate to double the ore procurement charge from its mines to 30% in 5 years, dealing with competitors from China and India.

“Enlargement of China’s smelting capability has brought about an ore scarcity that may persist by means of a minimum of 2014, based on CRU Group. Processing charges slumped 38 % this yr as smelters competed to course of scarce uncooked materials,” Bloomberg reported on the time (Sound acquainted? The identical factor is going on now — Rick)

The information outlet famous that Dowa Holdings, in a enterprise with Sojitz Corp. and Furakawa Co., stated it could spend $183 million to purchase a 25% stake within the Gibraltar copper mine in British Columbia from Taseko Mines (TSX:TKO).

Staying with Japan, in 2020 the nation’s high smelter, JX Nippon Mining & Metals, elevated possession of its then-majority-held Caserones copper mine in Chile (it’s now 51% owned by Lundin). The corporate purchased Mitsui Mining’s 25.8% stake after the price of the troubled venture doubled to $4.2 billion, based on The Northern Miner.

The next yr, Mitsui Mining & Smelting offloaded its 0.97% stake within the Collahuasi copper mine in Chile to its guardian firm, Japanese buying and selling agency Mitsui & Co, Mining Expertise stated. As talked about, Anglo American and Glencore every personal 44% of the open-pit mine. The remaining 12% is held by Japan Collahuasi Sources (JCR).

In 2018, a Reuters story stated “Chinese language copper smelters wish to make extra investments in mines, pushing to shore up provide of focus at a time when competitors for the uncooked materials is heating up, business executives stated. China is the world’s greatest shopper of the steel however its personal copper mine manufacturing has been stagnating amid a broad crackdown on air pollution, exacerbating a heavy reliance on imports.

“Extra direct tie-ups with mines would diversify smelters’ sources of provide, in addition to probably giving them extra sway in annual provide negotiations with giant world miners akin to BHP and Freeport-McMoRan Inc.”

The article went on to say {that a} personal Chinese language smelter, which makes use of 100% copper focus and no scrap, was seeking to cope with copper mines instantly. It quoted the chief vice chairman saying the smelter is potential funding in mines in South America, Europe and a few African international locations with secure political environments.

Getting extra present, Japan’s Mitsubishi Supplies Corp in 2023 stated it goals to greater than triple its copper focus output by means of fairness holdings by 2030, presumably by means of shopping for stakes in early and mid-stage improvement initiatives.

The corporate, which owns stakes in a number of copper mines together with Los Palambres and Mantoverde in Chile, desires to spice up its copper focus manufacturing to 500,000 tonnes a yr from 150,000t now. The plan would price $1.9 billion by the top of the last decade, together with investments in copper mining and smelting.

Juniors

We discovered that a number of majors have been investing in early-stage junior useful resource corporations, who, as I’ve said many occasions earlier than, personal the world’s subsequent mines. Amongst latest transactions:

- Freeport McMoRan (NYSE:FCX), the world’s largest publicly traded copper miner, in 2021 acquired all of the shares of Carpo Sources and its Yandera copper venture in Papua New Guinea. Measured and indicated sources quantity to six.2 billion kilos of copper equal, from sources of virtually 8 billion kilos of CuEq.

- Max Useful resource (TSXV:MAX) minimize an 80/20 earn-in cope with Freeport for its Cesar copper-silver venture in Colombia. Below the settlement, introduced on Might 13, Arizona-based Freeport has an possibility to amass as much as 80% of Cesar by spending CAD$50 million to discover the property.

- In August 2023 Rio Tinto agreed to purchase Pan American Silver’s stake in Agua de la Falda S.A., an organization with exploration tenements in Chile’s Atacama area, and to a three way partnership with Codelco to develop Agua de la Falda’s belongings.

Below the settlement, Rio Tinto will purchase Pan American’s (TSX:PAAS) 57.74% working stake in Agua de la Falda for $45 million and the grant of internet smelter returns royalties. Rio Tinto will even purchase the close by Meridian property for $550,000 and the grant of NSRs.

Codelco, which is the world’s largest copper producer and is owned by the Chilean authorities, holds the remaining 42.26% of Agua de la Falda.

- Pan American was additionally concerned in a cope with Glencore in July 2023, whereby Glencore purchased PAAS’s 56.2% stake within the Mara venture, situated within the Catamarca province of Argentina. The 27-year copper-gold mine has confirmed and possible reserves of 5.4 million tonnes of copper and seven.4 million ounces of gold.

- Final yr, First Quantum Minerals partnered with Rio Tinto to advance one of many world’s largest undeveloped copper sources, the La Granja copper venture in Peru. In accordance with the March 30, 2023 information launch, La Granja has an inferred useful resource of 4.32 billion tonnes at 0.51% copper. Rio Tinto has operated the venture since 2006. First Quantum will purchase a majority stake and can undertake the feasibility examine.

- In December 2023, Rio Tinto signed a cope with Arizona Sonoran Copper (TSX:ASCU) that would make Nuton, a Rio subsidiary, a accomplice and de-risk the Cactus venture.

The collaboration may earn Nuton a 40% stake within the venture on the location of the past-producing Sacaton mine south of Phoenix.

- In February 2024, Midnight Solar Mining (TSXV:MMA) teamed up with privately held KoBold Metals to discover Dumbwa, certainly one of 4 targets on its Solwezi copper venture in Zambia. KoBold will spend $15 million on exploration over the following 4 years and make money funds to Midnight Solar of CAD$500,000, to earn a 75% curiosity within the Dumbwa goal.

In April, Midnight Solar and First Quantum Minerals agreed to collectively outline potential feed sources on the Solwezi venture for First Quantum’s SW/EW oxide copper circuit at its Kansanshi mine.

- Lastly, in April 2024 China-focused Silvercorp Metals (TSX:SVM) acquired Adventus Mining (TSXV:ADZN), the rationale being to extend Silvercorp’s publicity to gold, in addition to metals key to a low-carbon future, together with copper. A information launch states that Silvercorp has the technical capability to develop the El Domo copper-gold venture in Ecuador right into a mine — having constructed eight mines in its present operations, three flotation mills of comparable measurement to El Domo, and three tailings storage amenities.

Conclusion

The worldwide hunt for copper has been on for many years, a minimum of for the reason that mid-‘90s, nevertheless it has been accelerating, as corporations concerned in all elements of the copper provide chain notice the structural provide deficit dealing with the copper market. They perceive the necessity to discover sources —current mines, expansions, brownfield initiatives, greenfield initiatives, and so on. and are making offers to amass the bottom steel, which isn’t solely important to electrification and decarbonization, however business normally.

Together with the same old functions in building wiring and plumbing, transportation, energy transmission and communications, there may be now added demand for copper in electrical automobiles and renewable vitality methods.

EVs use triple the quantity of copper as gasoline-powered vehicles. Further copper is being demanded by the electrification of public transportation methods, 5G and AI.

But the 22 million tonnes of copper mined final yr isn’t going to satisfy the required demand, particularly as governments proceed to set bold, some say inconceivable to satisfy, emissions discount targets.

A latest examine discovered that to affect the worldwide car fleet requires bringing into manufacturing 55% extra new mines. Between 35 and 195 giant new copper mines must be constructed over the following 32 years, at a charge of as much as six mines per yr. In different phrases, mission inconceivable.

Automakers are frightened about operating out of provide and are going on to the mines. In August 2023, Stellantis introduced it could pay $155 million for a 14.2% stake in McEwen Copper (a subsidiary of Canada’s McEwen Mining (MUX.TO) and its Los Azules venture in Arizona.

Some majors are taking the straightforward manner out and shopping for different majors to high up their copper reserves (none of this exercise will increase world copper reserves). Examples embrace BHP’s tried takeover of Anglo American, Newmont’s acquisition of Newcrest, and Glencore’s failed bid to get Teck and its copper asset portfolio.

Others, like Freeport McMoran (NYSE:FCX) are doing the more durable work of buying juniors like Max Useful resource (TSX.V:MAX), the house owners of the deposits which may turn out to be the following copper mines. Because the variety of mid-tier and main miners on the promoting block is decreased, these main miners transferring in direction of the underside on the mining meals chain and incomes into junior held initiatives, will more and more turn out to be the norm. Juniors personal the world’s future mines, they’re those the few left standing majors should purchase, or accomplice with, in an effort to improve their reserves.

Copper smelters are rising uninterested in scratching round for copper and receiving a pittance in therapy prices. They too are going on to the mines to make sure a gentle provide of copper feed. To date it’s principally Japanese corporations, however how lengthy earlier than Chinese language smelters, answerable for round half of world refined copper manufacturing, catch on and do the identical?

China neatly started its world venture to amass crucial metals — not simply copper however iron ore, lithium, cobalt, graphite, uncommon earths — and course of them domestically many years in the past. A run by means of latest copper M&A exhibits China continues to see copper as a high precedence.

“With China’s large copper smelting capability and manufacturing base, these investments signify a daring, long-term technique aimed toward securing copper provide for the nation’s future,” reads a latest report.

Western international locations could be clever to do the identical however I concern it could be too late. Present mines have gotten depleted, head grades are declining, and the copper discovery cabinet is naked. On high of this we’ve useful resource nationalism in a number of the huge copper-producing international locations (Chile, Peru, Panama) ongoing labor disruptions, and local weather change crimping manufacturing.

I’ll say it once more, together with an instance of a sophisticated junior working in a secure jurisdiction, junior mining corporations, like British Columbia’s Kodiak Copper (TSX.V:KDK), personal the world’s potential future mines.

Yearly so-called specialists predict a surplus; as a substitute what occurs? Deficit after provide deficit.

Benchmark Mineral Intelligence (BMI) forecasts world copper consumption to develop 3.5% to twenty-eight million tonnes in 2024, and for demand to extend from 27 million tonnes in 2023 to 38 million tonnes in 2032, averaging 3.9% yearly development.

But the US Geological Survey reviews provide from copper mines in 2023 amounted to solely 22 million tonnes. If the copper provide doesn’t develop this yr, we’re a 6Mt deficit.

Our calculations confirmed the present 22 million tonnes of manufacturing displays roughly a 20% discount in output from the highest 20 copper mines. If provide interruptions proceed in a number of the high producers, like Chile, Peru, Zambia and the DRC, the deficit may develop even greater, and sure will.

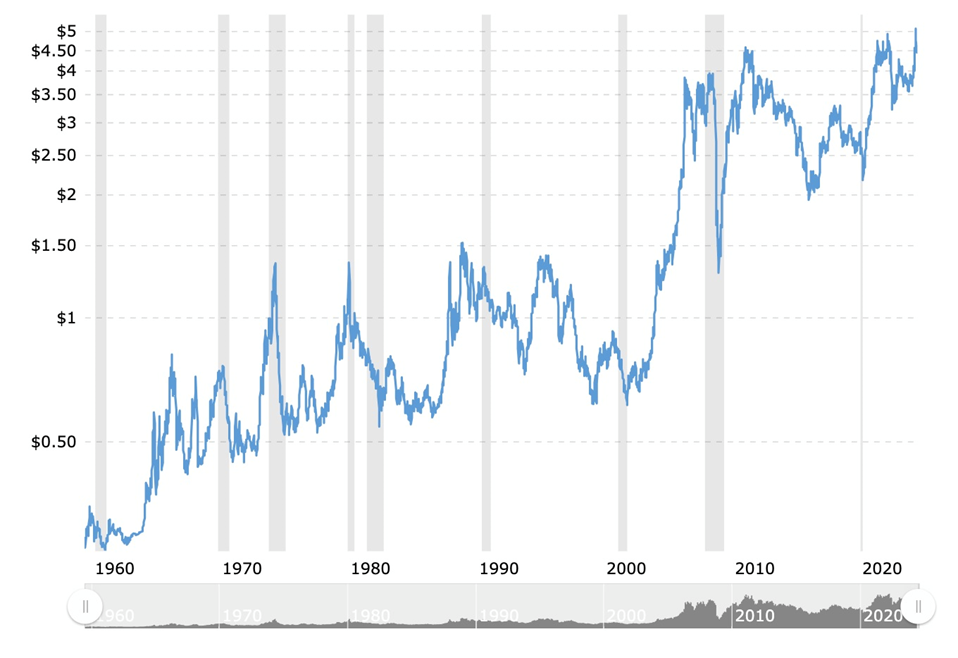

It ought to now be apparent why everyone seems to be scrambling to get their palms on copper. As soon as the workhorse of the worldwide financial system, low cost and plentiful, copper has been elevated to the world’s crucial mineral, with rising costs indicative of over-demand and under-supply.

Authorized Discover / Disclaimer

Forward of the Herd publication, aheadoftheherd.com, hereafter often called AOTH.

Please learn the complete Disclaimer rigorously earlier than you utilize this web site or learn the publication. If you don’t conform to all of the AOTH/Richard Mills Disclaimer, don’t entry/learn this web site/publication/article, or any of its pages. By studying/utilizing this AOTH/Richard Mills web site/publication/article, and whether or not you really learn this Disclaimer, you’re deemed to have accepted it.

Any AOTH/Richard Mills doc isn’t, and shouldn’t be, construed as a suggestion to promote or the solicitation of a suggestion to buy or subscribe for any funding.

AOTH/Richard Mills has based mostly this doc on data obtained from sources he believes to be dependable, however which has not been independently verified.

AOTH/Richard Mills makes no assure, illustration or guarantee and accepts no accountability or legal responsibility as to its accuracy or completeness.

Expressions of opinion are these of AOTH/Richard Mills solely and are topic to alter with out discover.

AOTH/Richard Mills assumes no guarantee, legal responsibility or assure for the present relevance, correctness or completeness of any data supplied inside this Report and won’t be held responsible for the consequence of reliance upon any opinion or assertion contained herein or any omission.

Moreover, AOTH/Richard Mills assumes no legal responsibility for any direct or oblique loss or injury for misplaced revenue, which you’ll incur because of the use and existence of the data supplied inside this AOTH/Richard Mills Report.

You agree that by studying AOTH/Richard Mills articles, you’re performing at your OWN RISK. In no occasion ought to AOTH/Richard Mills responsible for any direct or oblique buying and selling losses attributable to any data contained in AOTH/Richard Mills articles. Info in AOTH/Richard Mills articles isn’t a suggestion to promote or a solicitation of a suggestion to purchase any safety. AOTH/Richard Mills isn’t suggesting the transacting of any monetary devices.

Our publications should not a suggestion to purchase or promote a safety – no data posted on this web site is to be thought of funding recommendation or a suggestion to do something involving finance or cash except for performing your individual due diligence and consulting together with your private registered dealer/monetary advisor.

AOTH/Richard Mills recommends that earlier than investing in any securities, you seek the advice of with an expert monetary planner or advisor, and that it’s best to conduct an entire and impartial investigation earlier than investing in any safety after prudent consideration of all pertinent dangers. Forward of the Herd isn’t a registered dealer, seller, analyst, or advisor. We maintain no funding licenses and will not promote, supply to promote, or supply to purchase any safety.

Richard owns shares of Max Useful resource Corp. (TSX.V:MAX). MAX is a paid advertiser on his web site aheadoftheherd.com

Richard doesn’t personal shares of Kodiak Copper (TSX.V:KDK). KDK is a paid advertiser on his web site aheadoftheherd.com

This text is issued on behalf of MAX & KDK